💥 Worst Week for Markets in a Year (And Why Everything Sold Off)

$2 TRILLION Vanished in One Day (Stocks, Gold, Crypto, Bonds All Fell)

In the 80s, a magician named Teller (of Penn & Teller) explained how misdirection works. He said the audience looks where the magician wants them to look. Not because they are stupid. Because the human brain is wired to follow motion, color, and surprise. The trick is not in the flash. The trick is in what happens while you are watching the flash.

This week, the flash was AI. Marvell up 32%. Micron crossing $1 trillion. Nvidia unveiling a new PC chip. The crowd watched the flash. Meanwhile, the bond market was pricing in a Fed rate hike. The 30-year Treasury yield hit 5.2%. Mortgage rates jumped. The dollar strengthened. The cost of money went up while everyone was watching the magic trick.

Stocks fell. Bonds fell. Gold fell. Bitcoin fell. All in the same week. That almost never happens.

When everything drops at once, it’s not about any single company. It’s about the plumbing under the whole market. The price of money is going up, and that quietly resets the value of everything else. The most expensive, most crowded bets fall hardest. That’s why AI chips, gold, and bitcoin got hit worst.

Years in finance taught me to watch yields before headlines. The yields were screaming. As John Templeton warned, the four most expensive words in investing are "this time it's different." This week, the market remembered that the hard way.

In 1974, a mathematician named Edward Thorp walked into a casino. He did not look like a high roller. He wore thick glasses and a cheap sport coat. But Thorp had something the house did not expect. He had figured out that blackjack was not a game of luck. It was a game of information. If you tracked the cards already played, you knew the odds of what came next.

Edward Thorp did not stop after the casinos banned him. He took his math to Wall Street. He figured out that stock options were mispriced. He built the first quantitative hedge fund. He beat the market for 20 years. When people asked him his secret, he said one thing. "I do not predict. I prepare."

That is the difference between gambling and investing. Gambling is predicting the next card. Investing is preparing for any card.

Inside today's issue, you'll get the real reason stocks, bonds, gold, and crypto all fell together, why the 10-year yield is now the most important number in your portfolio, the FOMO trap quietly blowing up AI stocks, plus my insider-trade alerts, the week's top movers, and one high-conviction trade.

📬 Here’s what’s inside today’s issue:

Part I — Big Picture (Markets & Economy)

1. The Market Breakdown (And What Matters)

2. 5 Things You Need To Know Right NowPart II — What the Market Is Telling Us

3. Market Psychology, Hidden Signals, and What’s Next

4. Interest Rates Forecast + Real Estate OutlookPart III — Investment Research (Deep Dive & Analysis)

5. Insider Trading Alerts (Smart Money)

6. Stocks Beating the Market Right Now

7. The Smartest Trade I See Right NowPart IV — What You Should Actually Do

8. Practical Advice & What to Do Next

9. One Lesson I Wish I Learned Sooner (Remember This)

10. Ask Andrew Anything (Your Questions Answered)

I hope you’re enjoying this newsletter, it takes a lot of time to research and write so please help support us and:

Hit the LIKE button on this post and share this newsletter to social media or with friends/family:

Become a paid subscriber! (learn about the benefits here) (And get a free 30-day trial with this link):

Part I: Big Picture (Markets & Economy)

1️⃣ The Market Breakdown (And What Matters)

Stocks closed deep in the red. The S&P 500 lost 2.6% (its worst week since last May) and the Nasdaq dropped 4.7% (its worst week in over a year), snapping a 9-week win streak.

Friday alone wiped out more than $2 trillion in U.S. stock value. The big 9 trillion-dollar tech names shed about $1.1 trillion of that by themselves.

Chips led the wreck. Micron fell 13%, Broadcom 8%, Nvidia 6%, and AMD double digits. The chip sector lost over $1.3 trillion, its worst day since March 2020.

Bonds got dumped. The 30-year Treasury yield hit 5.2%, the highest since 2007, and the 10-year climbed to about 4.55%.

Bitcoin cracked $60,000, down roughly 16% on the week and about 50% off its October peak near $126K. ETFs saw a record $4.4B in outflows.

Gold fell as much as 3% to around $4,330. Even the safe havens got sold.

The trigger was a hot May jobs report. The economy added 172,000 jobs versus the 80,000 expected. Good news for workers, bad news for rate cuts.

Traders now price a 40% chance of a Fed rate hike by December, up from just 3% in June.

The SpaceX IPO, expected next week, may be pulling cash out of big tech as funds raise money to buy in.

Inflation and growth are moving in the wrong directions. PCE inflation rose to 3.8%, while first-quarter GDP growth was cut to 1.6%.

Consumers feel far worse than the stock market suggests. Consumer sentiment fell to a record low even as corporate profits and large technology stocks recently reached new highs.

💡 Andrew’s Analysis:

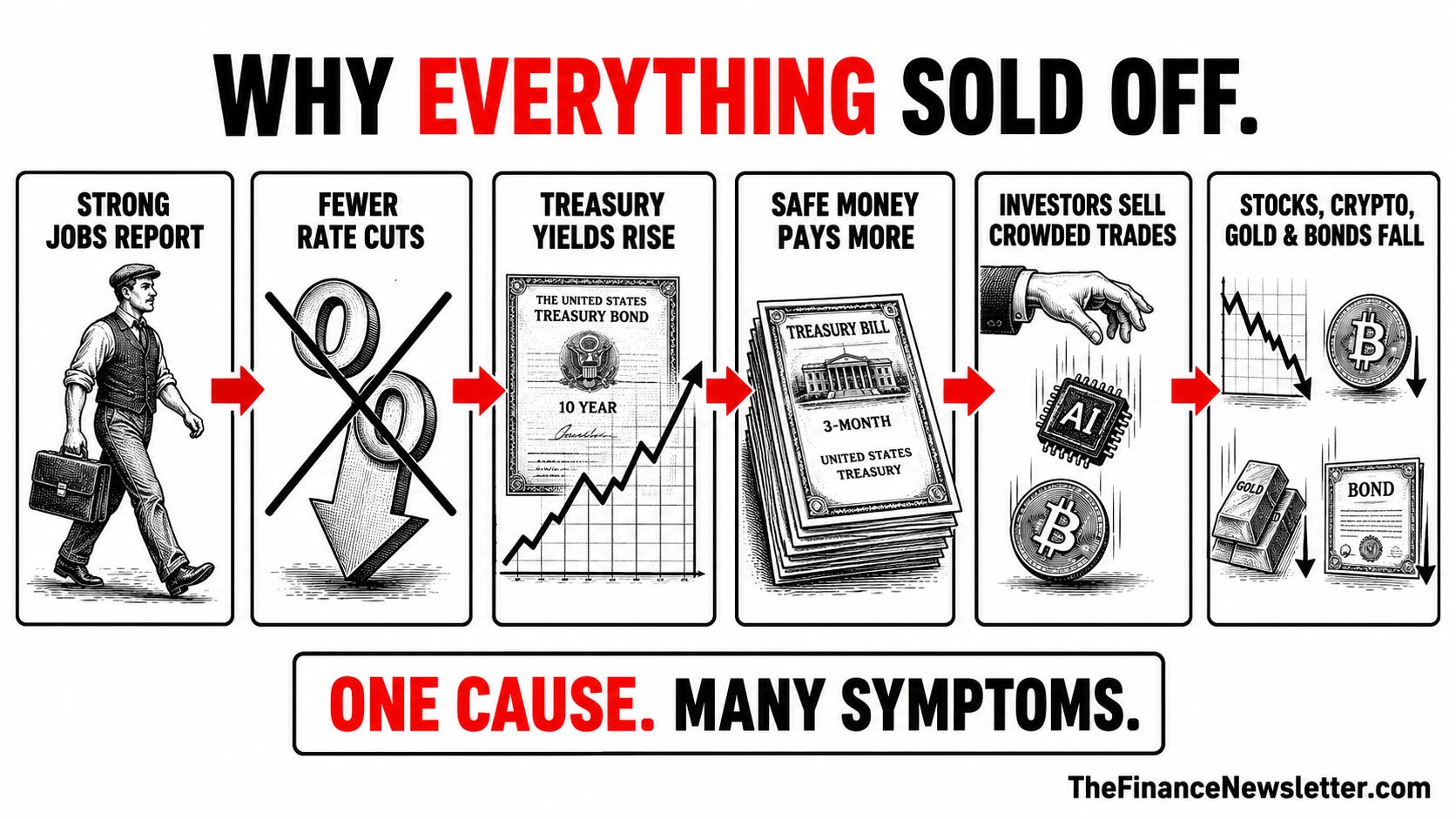

Everything sold off at once. That’s the part you need to sit with. Stocks, bonds, crypto, and gold all fell together in the same week. That almost never happens, and when it does, it’s telling you something simple. This wasn’t about any one company. It was about the price of money going up.

If you read last week’s issue, none of this caught you off guard. The bond market was screaming it. In my two decades around Wall Street, I learned to watch yields before I watch headlines, and the yields were flashing. When the “risk-free” rate rises, everything that’s priced off it has to reprice lower. The most expensive, longest-bet assets fall the hardest. That’s exactly why AI chips, bitcoin, and gold got hit worst. They were priced for a perfect future.

Here’s the chain reaction, start to finish: A strong jobs report told the Fed it can’t cut rates (and might have to raise them). That pushed Treasury yields to multi-year highs. Higher yields make safe bonds more attractive than risky bets, so money rotated out of the crowded winners. Add the Iran war keeping oil and inflation hot, a flood of government borrowing, and a giant SpaceX IPO sucking liquidity out of the market, and you get a “sell everything” Friday. One story. Many symptoms.

Now the debate. One camp says this is the first crack in a bubble. They point out that only 20 stocks hit new highs at the recent top, the same eerie setup we saw at the dot-com peak in 2000.

The other camp says buy the dip, because this is an expectations problem, not a growth problem. Broadcom still grew earnings 88%. It just didn’t beat a sky-high bar. Goldman still sees the S&P at 8,000.

My read? Both can be true at the same time. The near term looks shaky, and I’m staying defensive. But a great business on sale is still a great business. I called the pullback. I’m not calling the end of the bull market. I’m calling for discipline.

My advice:

Don’t confuse a great company with a great price. The chips that fell still have booming demand. The stocks just got ahead of the story.

Watch the 10-year yield. It’s the master switch for stocks, housing, and crypto right now. If it cools, risk assets breathe.

Trim the crowded trades. If more than 80% of your portfolio sits in AI and chips, take some off. Concentration feels great on the way up and awful on the way down.

Keep dry powder. Weeks like this hand you better prices. You can’t buy the dip if you’re fully invested at the top.

Look where nobody else is. Small caps and microcaps have quietly been beating the giants. The least-crowded corners often hold the best risk and reward.

The lesson is old and it never goes out of style. When money is free, hype runs the market. When money costs something again, fundamentals come back. We just got the reminder.

👉 For daily insights follow me on X /Twitter; Instagram Threads; Facebook; or BlueSky (and turn on notifications)

2️⃣ 5 Things You Need To Know Right Now

📬 Today we look at:

1) Social Security Is Running Out of Money.

2) Surging Bond Yields Threaten the Global Economy.

3) Oil Prices Will Push Interest Rates Higher.

4) FOMO Is Running This Market. That is Dangerous.

5) Winners in the Space Race.

🤔 But first, how much of your portfolio is in tech/AI stocks?

1. Social Security Is Running Out of Money.

The Committee for a Responsible Federal Budget reported that Social Security’s retirement trust fund is on track to run dry by late 2032, which would force an automatic 24% benefit cut. In plain terms, the average retiree’s check would shrink by about $500 a month. Around 63 million people would feel it. In some states it’s worse, with Connecticut facing a $556 cut, New Jersey $554, and New Hampshire $553.

Why is this happening? Math and demographics. When the program started in 1940, more than 150 workers paid in for every retiree. Today it’s fewer than three. People live longer, families have fewer kids, and more money flows out than comes in. The fix isn’t a mystery. Lawmakers could lift the payroll tax cap (right now income above $184,500 isn’t taxed for Social Security), nudge the payroll rate up a hair, or raise the retirement age for higher earners. The problem is politics. About 71% of Americans want more spending here, not less, so nobody wants to be the one to cut.

What this means for you is direct. Don’t build your retirement on a full check arriving. Plan as if you’ll get 75% to 80% of what’s promised, and fill the gap yourself with your own accounts. If you’re a high earner, watch the payroll-cap debate closely, because lifting it is the most likely fix and it would raise your taxes first.

2. Surging Bond Yields Threaten the Global Economy.

The $145 trillion global bond market is flashing red, signaling the era of governments spending freely with no consequences is over. The 30-year U.S. Treasury yield hit 5.18% this week, a post-2007 high. It’s not just us. Japan’s 30-year hit a record 4.15%, and the U.K.’s long bond touched 5.85%, the highest since 2008.

The cause is a pile-up. Supply shocks keep pushing prices up, governments need to borrow huge sums, and the AI buildout is hungry for capital. More borrowing plus more inflation equals higher and more jumpy interest rates. For you that means pricier mortgages and pricier corporate debt, today. And it means that if a recession hits, governments can’t just spend their way out without the bond market punishing them.

The takeaway is a regime change. Rising yields reward savers (lock in those rates while you can) and punish heavy borrowers and pricey growth stocks. The 10-year yield is now the single most important number in your portfolio.

3. Oil Prices Will Push Interest Rates Higher.

The Federal Reserve Bank of Boston reported that the oil spike from the Iran war, about a 33% jump, will push inflation materially higher while barely denting national employment. That’s the twist. The 1970s playbook had two villains, inflation and job losses. This time it’s mostly the first one. Our economy uses far less oil per dollar of output than it did 50 years ago, so a price shock burns your wallet without crushing the labor market.

There are winners and losers by geography. Oil states like Texas come out ahead, while importing regions like Massachusetts lag. The Fed’s own Beige Book pinned energy as the top driver of inflation right now, feeding into shipping, groceries, and fertilizer, even as hiring held steady almost everywhere.

Here’s why it matters for your money. If the shock hits prices but not jobs, the Fed’s worry shifts from “save the economy” to “kill inflation.” That leans hawkish, which means no rate cuts soon. Smart move is to keep some energy exposure as a hedge and expect sticky inflation to stick around through summer.

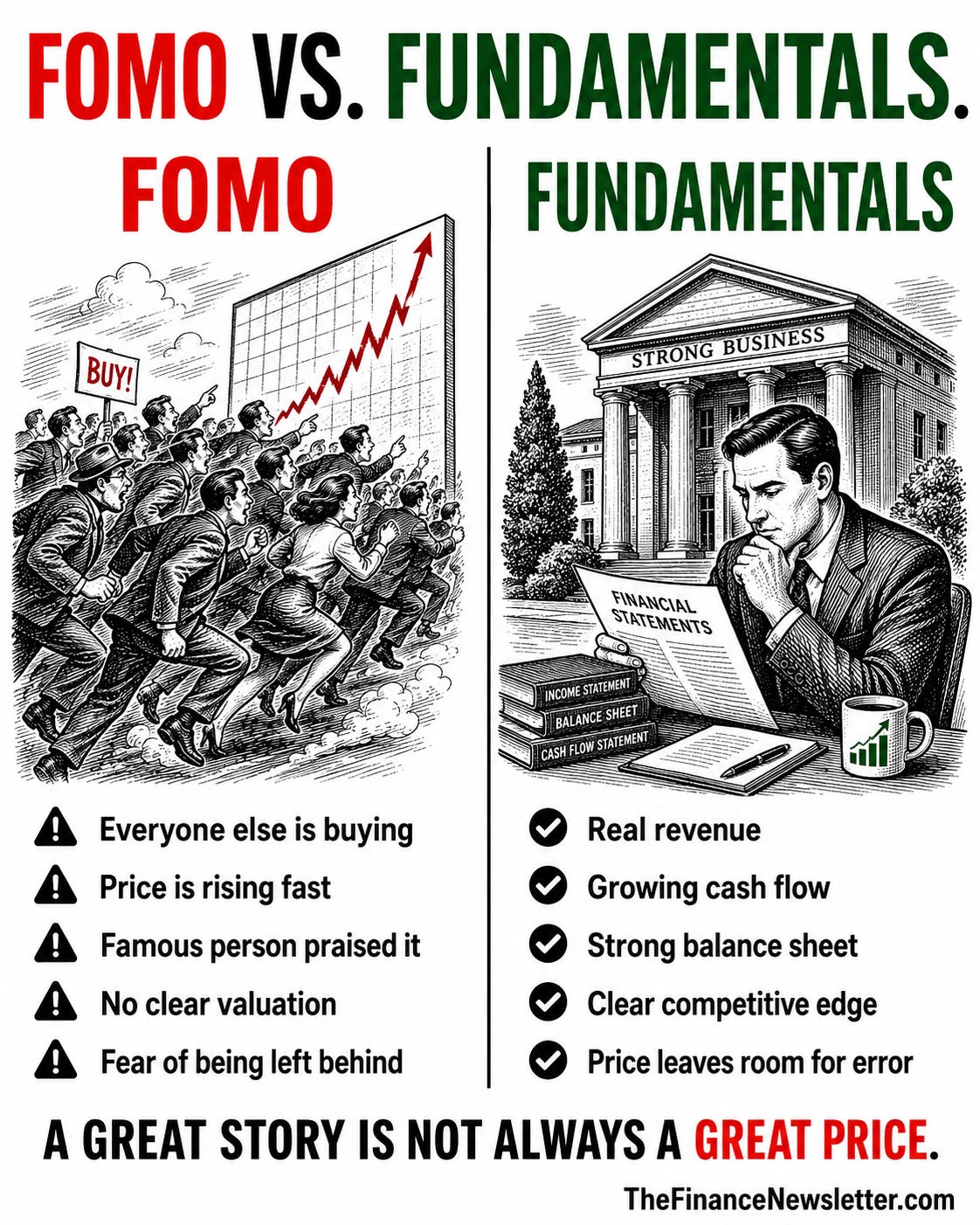

4. FOMO Is Running This Market. That is Dangerous.

The fear of missing out, not fundamentals, is steering big parts of the AI trade right now. The proof is everywhere. Marvell jumped 32% in a day because Nvidia’s CEO called it the next trillion-dollar company. IBM hit a record high on a six-month-old video of a Trump compliment. Virgin Galactic soared 21% because Reddit users confused its ticker with SpaceX’s new one, then crashed 38% the next day. And Micron crossed a $1 trillion value on the bold claim that memory chips “aren’t cyclical anymore.”

The danger sign is the disconnect. Raymond James estimates AI customers will need to spend more than $1 trillion a year to justify the current buildout. History says capital-spending booms this fast and this narrow tend to end in a bust. The legendary investor John Templeton called “this time it’s different” the four most expensive words in investing, and the market is leaning on them hard.

The move here isn’t to bail on AI. It’s to separate the real (datacenter demand is genuine) from the vibes (ticker confusion is not a thesis). Size your positions so a 20% to 30% drawdown doesn’t wreck you, and never chase a parabolic move you can’t explain.

5. Winners in the Space Race.

Space stocks have climbed about 75% this year on SpaceX IPO buzz, outrunning even AI funds. The catch is that none of the pure-play names (Rocket Lab, AST SpaceMobile, Planet Labs, and friends) are profitable, and they trade around 75 times sales. A Blue Origin rocket exploded on the launch pad this week, a blunt reminder that this business is hard and risky.

SpaceX itself is special, with real technology and a profitable Starlink arm. But a rumored $1.5 to $2 trillion price tag has more to do with Elon Musk’s fan base than financial fundamentals. If SpaceX comes back to earth after its debut, it could drag the whole sector down with it.

The safer play is the boring one. Diversified defense and aerospace primes like Lockheed Martin, Airbus, Boeing, and Safran have real space revenue and a defense tailwind as Europe ramps military spending. If you want space exposure, favor the profitable giants over the story stocks, and treat any SpaceX-adjacent pop as a trade, not a forever holding.

💡 Andrew’s Analysis:

The price of money is rising, and it’s separating what’s real from what’s hype. Social Security’s shortfall, the global bond warning, and the oil shock all push the same direction, toward higher rates, harder choices, and less free money. The AI and space frenzy is the mirror image, investors chasing a dream while the cost of capital quietly turns against them.

When money was free, hype thrived and fundamentals got ignored. Now that money costs something again, fundamentals are back in charge. That’s not a coincidence across these stories. It’s the whole point.

So here’s my advice. Own businesses that make real cash, not promises. Demand a margin of safety before you buy anything priced for perfection. Don’t outsource your retirement to a system that’s running 24% short. And keep your story-stock bets small enough that being wrong is an inconvenience, not a catastrophe.

I hope you’re enjoying this newsletter! It takes a week to research and write so please support our journalism and:

Hit the LIKE button on this post and share this newsletter to social media or with friends/family:

Become a paid subscriber to get smarter with your money! (learn about the benefits here) (Get a free 30-day trial with this link):

(Your job can pay for this newsletter with its employee development budget — Send this email template to your manager)

Part II: What the Market Is Telling Us

3. Market Psychology, Hidden Signals, and What’s Next

4. Interest Rate Forecast + Real Estate Outlook

3️⃣ Market Psychology, Hidden Signals, and What’s Next

Fear & Greed Index — leaning negative

The Fear & Greed Index is a quick read on the market’s mood, scored 0 to 100, where low means fear and high means greed. Right now it sits at 42, in “Fear,” and it’s been sliding fast (down from 54 last week and 67 a year ago). The scary parts are under the hood. J

unk bond demand is in Extreme Fear, and safe-haven demand, stock strength, and breadth are all in Fear. That tells you investors are quietly running for cover even as the headline number looks calm. The one oddball is the put/call ratio, still flashing greed. Net read, fear is taking over, which is a caution sign short term. But remember, deep fear is also where bottoms often form.

AAII Investor Sentiment — negative, with a contrarian twist

The AAII Sentiment Survey asks everyday investors where they think stocks go over the next six months. As of June 3, bullish sits at 36.3%, neutral at 26.7%, and bearish at 37.0%.

Bearishness has now beaten its long-term average for 17 straight weeks. When asked what worries them most, members named the economy and inflation (34.8%) and geopolitics (33.6%). The straight read is negative. But here’s the twist that comes from years of watching this survey. When the crowd gets this gloomy for this long, the market often does the opposite of what they fear. Extreme pessimism is a contrarian green flag.

Technical Analysis — mixed, short-term cracked

The S&P 500 closed at 7,383.74, down about 201 points on the day, and it broke below the floor of its rising trend channel. That signals a slower climb ahead or a move sideways, not a collapse. Support sits near 6,840 and resistance near 7,600. The longer-term trend still reads positive.

The Nasdaq-100 closed at 28,957.60, down about 1,450, and also cracked its channel floor, with support near 24,700 and resistance near 30,600.

Bitcoin is the ugly one. It broke its falling channel to the downside with no clear support below, though it’s oversold and bounced a touch to about $61,700.

My read: mixed for stocks (short-term damage, long-term uptrend intact) and outright negative for bitcoin.

Economic Indicators — mixed

Here’s where the indicators sit versus their typical ranges.

Market volatility (VIX) reads 17.27, calm and neutral.

The 10-year Treasury yield reads 4.45, on the higher side.

The yield spread reads 0.76, positive (not inverted), which is good and signals no recession warning from the curve.

Inflation (CPI) reads 3.78, hot and the clear negative.

Unemployment reads 4.30, low and healthy.

GDP growth reads 2.00, modest and fine.

Consumer sentiment reads 49.80, near record lows and a clear negative.

Put together, it’s a split picture. Jobs and growth are okay and the yield curve isn’t flashing recession, but inflation is hot and people feel terrible. Mixed.

Recession Indicators — neutral to positive

The biggest one, the yield curve, is positive and not inverted. That’s historically the most reliable recession warning, and it isn’t ringing. Jobs are still growing. So the near-term recession risk looks low to moderate. The live threat isn’t a recession right now. It’s sticky inflation forcing the Fed to stay tight.

The bigger picture

Line these up and they tell one clean story. Fear is rising (Fear & Greed at 42, AAII bearish for months) and the charts cracked short term, but the economy itself isn’t broken. Jobs are solid, growth is positive, and the yield curve is normal. So this is a sentiment and rate scare, not a recession.

The knot tying everything together is inflation and rates. Hot CPI, the Iran oil shock, and a strong jobs report all push the Fed to stay tight or even hike. That’s what spooked stocks and crypto, and that’s what the indicators are reacting to.

What could push markets higher from here? A cooler CPI print (next week’s number is the big one), an Iran deal that reopens the Strait of Hormuz and drops oil, or the Fed signaling patience.

What could push them lower? A hot CPI, oil spiking toward $150 if the Strait stays blocked, or more chip-guidance disappointments.

My read: Cautious near term, eyes glued to next week’s inflation data. But extreme fear sitting on top of a healthy economy is usually where bottoms get built. So I’m writing a buy list, not a panic-sell list.

👉For daily insights, follow me on X /Twitter; Instagram Threads; Facebook; or BlueSky (and turn on notifications)

4️⃣ Interest Rate Forecast + Real Estate Outlook

Interest rates

I think mortgage rates hold steady in June, hovering around 6.5% for the 30-year fixed. The reason is simple. Inflation, fueled by the Iran war and higher oil, keeps bond yields elevated, and the Fed is widely expected to hold at its June 16 to 17 meeting (the market is even pricing some odds of a hike). Freddie Mac came in at 6.48% this week, down a tiny 5 basis points, and the 10-year Treasury held below 4.5%. So nothing is breaking loose in either direction yet.

The swing factor is next week’s CPI report. If inflation cools, rates can finally drift lower and affordability improves. If it runs hot, rates stay rangebound or push higher. Until the Strait of Hormuz reopens and oil settles, I wouldn’t bet on a big drop.

My advice: If you’re a buyer, don’t sit on the sidelines waiting for a rate crash that may not come. Buy the home you can afford now and refinance later if rates fall.

If you’re a seller, price to the market from day one (more on why below).

If you’re an investor, lock your rate on deals you like and keep cash ready to refinance if a CPI-driven dip shows up.

Real estate

Home prices are falling at a record pace, but this is not a crash. Realtor.com data shows the median list price at $429,500, down 2.4% from a year ago, the steepest yearly drop in their data going back to 2017. Here’s the key detail that proves it’s healthy, not scary. The share of listings with price cuts actually fell (to 17.5%, down 1.6 points), and pending sales rose for a sixth straight month. Translation: sellers are pricing realistically from the start, and buyers are showing up when the number fits their budget.

Inventory is up 2.2% from last year (growth is slowing), and homes are taking about 52 days to sell, roughly normal. There’s a regional split worth watching. New listings are surging in the Northeast and Midwest, while the South and West are stalling and seeing homes sit longer. And rates today are about 37 basis points below where they were a year ago, a quiet tailwind for buyers.

My advice: This is a balancing market, not a 2008 repeat. Buyers finally have some leverage, so negotiate hard and ask sellers for a rate buydown.

Sellers should price right out of the gate and skip the “test the market” game that backfired last year.

Investors should hunt the South and West, where inventory is building and sellers are more motivated.

My forecast: Rates flat near 6.5% through summer, with downside only if inflation cools or the Strait reopens. Home prices keep softening at low single-digit yearly declines, no crash, with the South and West the softest and the Northeast and Midwest the firmest.

I hope you’re enjoying the newsletter! It takes a week to write and research so please help support us and:

Hit the LIKE button on this post and share this newsletter to social media or with friends/family:

Become a paid subscriber and get smarter with money! (learn about the benefits here) (Get a free 30-day trial with this link):

Part III: Investment Research (Deep Dive & Analysis)

5. Insider Trading Alerts (Smart Money)

6. Stocks Beating the Market Right Now

7. The Smartest Trade I See Right Now

5️⃣ Insider Trading Alerts (Smart Money)

Microsoft $MSFT

A congressman with a finance-committee seat just loaded up on the AI giant.

Josh Gottheimer (Democrat, House, New Jersey) made two joint buys, both filed on June 4, 2026, in the $250K to $500K range and the $500K to $1M range (a combined ballpark of $750K to $1.5M).

Gottheimer sits on the House Financial Services Committee, so his trades always get a second look. Microsoft is the AI and cloud heavyweight, with Azure, a huge OpenAI stake, Copilot, and the brand-new Nvidia PC-chip partnership. Buying one of the most liquid megacaps on earth is a low-drama, high-confidence move. The committee seat is what makes any tech buy worth flagging. The outlook is steady, with Azure and AI driving a massive market for years.

Summit Therapeutics $SMMT

Two co-CEOs bought together, and one of them is a billionaire. Robert Duggan (Co-CEO and 10% owner) and Mahkam Zanganeh (Co-CEO and 10% owner) each bought 100,000 shares at $14.60. Each trade was worth $1.46 million, a combined $2.92 million, both filed on June 4, 2026.

Duggan made his fortune by selling Pharmacyclics to AbbVie for about $21 billion, then took the reins at Summit. The company’s whole story rides on ivonescimab, a lung-cancer drug that beat Merck’s blockbuster Keytruda in head-to-head trials in China.

When both people running the company buy on the same day, that’s a loud signal. Why now? They likely see upside in upcoming trial readouts and a path to U.S. approval. The outlook is classic high-risk, high-reward biotech. The cancer-drug market is enormous, but the stock will live or die on trial data.

Aurinia Pharmaceuticals $AUPH

A value-focused almost billionaire just made his biggest bet on the board this week. Kevin Tang (CEO and 10% owner), who runs Tang Capital, bought 814,606 shares at $15.29, a trade worth $12.46 million, filed on June 2, 2026.

Tang is known for buying beaten-down biotechs and squeezing value out of them, sometimes through buybacks or a sale. Aurinia makes Lupkynis, the only FDA-approved pill for lupus nephritis (a serious kidney disease). A buy this size from a famously disciplined investor says he thinks the stock is cheap against its cash and drug sales. Why? He may be betting on growing prescriptions, a buyback, or a takeover. The outlook is a profitable niche drugmaker sitting on cash, which makes it a real M&A candidate.

6️⃣ Stocks Beating the Market Right Now

1) Fluence Energy $FLNC up +43.8% on 6/1

Fluence is up 43.8% after unveiling an AI datacenter collaboration with Siemens and Nvidia. Fluence builds grid-scale battery storage systems. Here’s why that suddenly matters. AI datacenters burn enormous, steady amounts of power, and batteries smooth out that demand and keep the grid stable. This deal drops Fluence right into the center of the AI-power story.

The outlook is strong, the energy-storage market is set to balloon as datacenters and renewables scale together, giving Fluence a multi-year runway. Watch margins and competition, but the runway is real.

2) PagerDuty $PD up +33.6% on 5/29

PagerDuty is up 33.6% after beating on earnings, revenue, and operating income while raising its full-year profit outlook. PagerDuty makes incident-response software, the system that pings IT teams the moment something breaks. As companies run more AI and cloud, uptime becomes mission-critical, and that plays right into PagerDuty’s hands.

The outlook points to a growing market in automated IT operations, sticky enterprise customers, and a clearer path to lasting profits.

3) Okta $OKTA up +30.1% on 5/29

Okta is up 30.1% after both quarterly and full-year revenue guidance topped Wall Street. Okta is the leader in identity and login security, the single sign-on layer that controls who gets access to what. Every new AI app and cloud tool needs secure identity, which is a direct tailwind.

The outlook is bright, identity is a must-have, the market is large, and the rise of AI agents creates a whole new wave of “identities” that need securing.

4) NetApp $NTAP up +22.4% on 5/29

NetApp is up 22.4% on a fiscal fourth-quarter earnings and revenue beat. NetApp sells data storage and management for the hybrid cloud. Simple logic here. AI runs on data, and that data has to live somewhere fast and reliable.

The outlook leans on rising AI-data storage demand, a steady enterprise customer base, and a dividend-plus-buyback program that supports the stock.

5) Hewlett Packard Enterprise $HPE up +19.5% on 6/2

HPE is up 19.5% after posting its biggest earnings beat since 2018, with 40% revenue growth. HPE sells servers, networking gear, and AI infrastructure. It’s riding the same AI-server boom that’s been lifting Dell.

The outlook centers on a growing AI-server backlog and the GreenLake cloud subscription business, with one thing to watch, margins, as lower-margin hardware makes up more of the mix.

6) Navitas Semiconductor $NVTS up +19.3% on 6/3

Navitas is up 19.3% after Nvidia showcased its latest power-chip technology at the Computex conference. Navitas makes next-generation power chips (gallium nitride and silicon carbide) that run cooler and waste less energy. With AI datacenters desperate to cut their power bills, efficient power chips are gold.

The outlook is a large efficiency-driven market tied to both AI and EVs, boosted by the Nvidia halo, though as a small cap it’ll stay volatile.

7) Coherent $COHR up +17.6% on 6/2

Coherent is up 17.6% after Nvidia’s CEO highlighted the growing need for optical networking in AI datacenters. Coherent makes the optical components and lasers that move data between AI chips at the speed of light.

The outlook is solid, optical networking is one of AI’s key bottlenecks, demand visibility is strong, and the main risks are execution and competition.

8) STMicroelectronics $STM up +15.2% on 6/2

STMicro is up 15.2% after raising its 2026 datacenter revenue target to about $1 billion. STMicro is a European chipmaker covering power chips, sensors, and microcontrollers for cars, industry, and now datacenters.

The outlook leans on datacenter and auto-chip growth and a broad set of end markets, balanced by the usual chip-industry cycles.

9) Redwire $RDW up +15.1% on 6/4

Redwire is up 15.1% after securing another space contract, this time with regenerative-agriculture startup Astrobiome Space. Redwire builds space infrastructure like solar arrays, components, and in-space manufacturing gear. It’s riding the SpaceX-IPO space wave.

The outlook taps a fast-growing space economy, but the business is contract-driven and the stock trades like a story name, so keep position sizes sensible.

👉 For daily insights, follow me on X /Twitter; Instagram Threads; Facebook; or BlueSky, and turn on notifications!

7️⃣ The Smartest Trade I See Right Now

Hinge Health $HNGE

Big bullish bets are stacking up here. Hinge Health rose $3.24 to $66.23, and call activity is running hot, with 8,653 calls traded, 9 times the average volume and 5 times the put volume. Most of it is parked in the June 18 expiration at the 75.00 strike, and traders are mostly paying the offer, which points to buy-side, bullish intent. The put/call ratio of 0.19 backs that up (way more calls than puts).

Hinge Health runs a digital physical-therapy platform, virtual care for back, joint, and muscle pain delivered through an app and motion sensors, sold mostly to employers who want cheaper care.

The stock has rallied more than 25% since a strong earnings beat on May 5, and this options flow is betting the run continues.

My take, cautiously bullish. The momentum and the flow are real, and the digital-health market is large and growing as employers hunt for lower-cost care. But the 75 strike is a big jump from $66 with limited time, so this is an aggressive bet. I like the direction. I’d respect the risk. The longer-term outlook depends on Hinge proving it can turn that big addressable market into steady profits.

I hope you’re enjoying this newsletter, it takes a week to research and write so please support us and:

Hit the LIKE button on this post and share this newsletter to your social media or with friends/family:

Become a paid subscriber and get smarter with money! (learn about the benefits here) (Get a free 30-day trial with this link):

Part IV: What You Should Actually Do Now

8. Practical Advice & What to Do Next

9. One Lesson I Wish I Learned Sooner (Remember This)

10. Ask Andrew Anything (Your Questions Answered)

8️⃣ Practical Advice & What to Do Next

Don't confuse a great company with a great price. The chips that fell still have booming demand. The stocks just ran ahead of the story. A wonderful business at a terrible price is still a bad investment.

Buy real cash flow. Ignore the hype. Buy companies that make actual money today. Demand a margin of safety before you buy anything priced for perfection.

Trim the crowded trades. If most of your portfolio sits in AI and chips, take some off the table. Concentration feels amazing on the way up and brutal on the way down. Spreading out isn't weakness. It's survival.

Watch the 10-year Treasury yield. It's the master switch. Stocks, housing, and crypto all dance to it right now. If yields cool, risk assets breathe. If they keep rising, everything pricey stays under pressure. Make it the first chart you check each morning.

Keep dry powder. You can't buy the dip if you're fully invested at the top. Hold some cash so a scary week becomes a shopping list, not a gut punch.

Don't build your retirement on a full Social Security check. Plan as if you'll get 75% to 80% of what's promised, and fill the gap with your own accounts. Hope is not a retirement plan.

If you're buying a home, buy what you can afford now. Don't wait for a rate crash that may not come. Buy smart, then refinance later if rates fall. Marry the house, date the rate.

👉 For daily insights, follow me on X /Twitter; Instagram Threads; Facebook; or BlueSky (and turn on notifications)

9️⃣ One Lesson I Wish I Learned Sooner (Remember This)

My grandfather was a farmer. He told me a story I have never forgotten. In the 50s, a drought killed his crop for three straight years. The fourth year, the rains came back. The fifth year, they came harder. By the sixth year, his neighbors were planting right up to the riverbank. They said the drought was the new normal, so the floods would not come back. The seventh year, the river rose 20 feet and wiped out every farm on the floodplain.

My grandfather survived because he remembered both. He kept a buffer. He planted less than he could. He stored grain in the good years. When the flood came, he had enough to rebuild while his neighbors went bankrupt.

The flood is here. The 30-year Treasury is at 5.2%. Mortgage rates are near 6.65%. The Nasdaq just had its worst week in a year. Bitcoin is down 50% from its peak. The question is not whether you saw it coming. The question is whether you built your buffer.

A buffer is not cash sitting in a checking account earning nothing. It is a 5.2% Treasury bond. It is a small-cap fund that has been beating the Nasdaq while nobody was watching. It is a real estate deal locked in at a fixed rate. It is the discipline to sell a winner when it gets too big a slice of your pie.

The water will recede. It always does. And when it does, the people with buffers will buy the land that the leveraged lost. That is how wealth is built. Not by predicting floods. By surviving them.

In my 20 years in finance, I have learned that markets work the same way. After years of easy money, people forget that hard money exists. They plant right up to the riverbank. They leverage up. They chase yield. They confuse a trend with a law of nature. Then the flood comes.

This week was a flood. The 30-year Treasury hit 5.2%. Mortgage rates touched 6.65%. The S&P 500 lost its nine-week winning streak in a single Friday. The Nasdaq had its worst day in over a year. Bitcoin fell below $60,000. Gold dropped 3%. It was not a stock story. It was not a crypto story. It was a money story. The cost of capital went up, and every asset priced for free money got wet.

If you read last week’s issue, you saw this coming. I warned that the bond market was the canary, and the canary was gasping for air. Now the mine is filling with smoke. The question is not whether you smell it. The question is whether you kept your buffer.

🔟 Ask Andrew Anything (Your Questions Answered)

Q: Why did the stock market crash so fast this week

A hot jobs report spooked the bond market. Investors realize the Federal Reserve cannot cut interest rates anytime soon. When borrowing money stays expensive, investors sell risky assets like tech stocks and crypto

Q: How do I know when to buy the dip?

When the Fear & Greed Index hits extreme fear (below 25), when the VIX spikes above 30, and when the stocks you want to own are down 30% from their highs. Right now, the Fear & Greed Index is at 42. Not there yet. Build your list. Set your prices. Be patient. The best buys come when everyone else is terrified.

Q: Are we in an AI bubble?

Parts of it, yes. The demand for AI is real. The prices people are paying often aren’t. When a stock jumps 32% on one CEO’s sentence, that’s FOMO, not analysis. The fix isn’t to bail on AI. It’s to separate real winners from hype and keep your positions small enough to survive a 30% drop.

Q: Is the AI boom over?

No. AI spending, data center construction, and demand for computing power remain large.

The investment phase is changing. Investors now want proof that spending can create revenue, margins, and cash flow.

AI growth can continue while many AI stocks fall.

Q: Is Social Security really going broke?

Not exactly, but the trust fund is on track to run dry around 2032, which would force an automatic 24% cut, about $500 a month for the average retiree. It’s fixable if Congress acts. Don’t count on a full check. Plan for less and save the difference yourself.

Q: Should I buy a house now or wait?

Buy if you can afford the payment at 6.5% and the house fits your life. Do not try to time the rate bottom. Rates could fall to 5.5% next year. They could rise to 7.5% if inflation surges. The house is a home first and an investment second. Lock the rate, buy the home, refinance later if rates drop. The asymmetric risk favors action.

👋Last Words:

Thank you for reading and joining 113,000 subscribers who trust this newsletter to get smarter with money! My goal is simple: Make it easy for you to connect the dots on the economy, markets, and investing.

I hope you’re enjoying this newsletter. Please help support us and:

Hit the LIKE button on this post and share it on social media with friends/family:

Become a paid subscriber and get smarter with your money (learn about the benefits here) (get a free 30-day trial with this link):

(fyi, your job can pay for this newsletter with its employee development budget. To make it easy, we’ve created this email template to send to your manager.)

And please let us know what you think of this newsletter:

Missed an issue? Read past issues here at TheFinanceNewsletter.com

☺️ My goal is to help you become richer and smarter with money — Join 3+ million and follow me across social media for daily insights:

Instagram Threads: @Fluent.In.Finance

Twitter/ X: @FluentInFinance

Facebook Page: Facebook.com/FluentInFinance

Linkedin: Linkedin.com/in/Lokenauth

Youtube: Youtube.com/FluentInFinance

Instagram: @Fluent.In.Finance

TikTok: @FluentInFinance

Facebook Group: Facebook.com/Groups/FinanceTalk

Reddit Community: r/FluentInFinance

➕Please add this newsletter to your contacts to ensure that none of our emails ever go to spam!

This content is for educational purposes only. Such information should not be construed as legal, tax, investment, financial, or other advice. See for Disclaimer, Terms and Conditions.