💥 How to Survive AI Layoffs, a Housing Crisis, Inflation, and a War

AI Is Taking Jobs. Consumer Sentiment Crashed. INFLATION Is Back… And It Gets Worse.

It was a cold April night in 1912 when the Titanic struck the iceberg. The band played on. Passengers marveled at the luxury. Most refused to believe the “unsinkable” ship could fail. They ignored the warning signs until the water was at their feet.

In the months before Pearl Harbor, the stock market rallied. Investors told themselves the war would stay overseas.

In the weeks before the 2008 crash, everyone laughed at the idea of a housing collapse.

Humans confuse calm surfaces with safe waters.

Right now, the surface looks calm. Stocks are up. AI stocks are booming. But underneath, the data tells a different story. Consumer sentiment hit an all-time low. Inflation is speeding up. A war in Iran is disrupting global energy. And Michael Burry just found a $1.7 trillion accounting illusion hiding in your 401k. This issue connects every dot.

Most people think the biggest risk right now is a crash. They’re wrong.

The biggest risk is believing everything is fine.

Because when markets go up during rising inflation, falling confidence, and increasing layoffs… it doesn’t mean the economy is strong.

It means something is out of balance.

And imbalances don’t last.

In this issue, I break down why inflation is likely to get worse before it gets better, expose the $1.7 trillion earnings illusion hiding in your 401(k), explain why the housing crisis just deepened, show you where the smart money is moving, and give you the exact steps to protect and grow your wealth through the chaos.

📬 In today’s newsletter, we’ll look at:

Part I - Markets & Economy:

1. Update, Analysis, and Outlook

2. Important Finance News

3. Chart of the DayPart II - Investing Research:

4. Insider Trades

5. Top Stocks Right Now

6. Today’s Trade

7. Market Sentiment (Fear & Greed Analysis)

8. Macro Technical AnalysisPart III - Tips & Advice:

9. Advice & Recommendations

10. Final Thoughts

11. Your Questions Answered

We hope you’re enjoying this newsletter — it takes a week to research and write so please help support our journalism and:

Hit the LIKE button❤️ on this post and share this newsletter on social media (or with friends & family):

🙏Become a paid subscriber! (learn about the benefits here) (Get a free 30-day trial with this link):

Part I - Markets & Economy

(1) Update, Analysis, and Outlook

📈 Everything You Need to Know (in 1 minute):

Inflation re-accelerated to 3.3% in March — gasoline prices surged a record 21.2% in a single month, the biggest one-month spike since the 1960s. The Iran war is the root cause. That one category accounted for nearly three-quarters of the entire March inflation reading.

The Iran war has removed roughly 500 million barrels from global markets in ~50 days — about $50 billion in lost oil production. That’s equal to all the fuel the world’s international shipping industry burns in 4 months. Peace talks collapsed this weekend, and the U.S. Navy has now begun enforcing a blockade of the Strait of Hormuz.

Consumer sentiment just hit its lowest level in recorded history. The University of Michigan survey has never been this low. 65% of Americans say rising prices are outpacing their income. 39% are now using credit cards to buy groceries.

March home sales fell 3.6% to 3.98 million (annualized) — the worst number since mid-2025. The spring selling season got off to its worst start in recent memory as high costs and war-driven uncertainty froze buyers out.

Airfares jumped 15% year-over-year in March. Delta, United, American, and Southwest all raised checked bag fees by $10. Delta alone faces over $2 billion in added fuel costs just this quarter.

Tech layoffs are accelerating fast. Meta is cutting ~8,000 employees in May (10% of workforce), with more cuts planned later this year. Snap cut 16% this week. Block cut 40%, with CEO Jack Dorsey saying AI is “doing a lot of these jobs better and less expensively than humans.”

Michael Burry found a $1.7 trillion “earnings illusion” hiding in tech stocks. After reviewing over 1,000 annual reports, he says tech earnings are overstated by 42% due to improper accounting for stock-based compensation. Companies flagged include Meta, Palantir, Shopify, CrowdStrike, and Workday.

AI chip demand keeps accelerating — and supply can’t keep up. TSMC posted profits up 58% year-over-year, raised its full-year forecast, and confirmed AI demand is “extremely robust.” ASML said demand is outpacing supply. Cloud providers are committing $600B+ to data centers this year alone.

Apple named a new CEO. Hardware chief John Ternus takes over September 1. Tim Cook becomes executive chairman after growing Apple from ~$330 billion to $4 trillion — a 12x increase over his tenure.

Psychedelic drug stocks surged 17-42% after Trump signed an executive order fast-tracking FDA review timelines for LSD, psilocybin, and ibogaine treatments. $50 million in federal research funding is attached.

China’s solid-state EV batteries are entering mass production in 2026. Greater Bay Technology just moved these cells off the lab bench and onto the production line — with 2x+ the energy density of current lithium-ion batteries and a potential driving range over 620 miles per charge.

💡 Andrew’s Analysis & Advice:

The most dangerous thing you can do right now is assume things are fine.

Global uncertainty just hit its highest level in recorded history. Not during 9/11. Not during the 2008 financial crash. Not even during COVID. Right now. And yet, the S&P 500 is near all-time highs. Consumer sentiment just hit an all-time low. The gap between what markets are saying and what people are feeling is the most important financial story of 2026.

I’ve been doing this for over 20 years. Through my time at Wall Street banks — through war cycles, credit crises, and irrational exuberance — I’ve learned that the moments that feel the most stable on the surface are often the most fragile underneath. Here’s how to read what’s really happening right now.

One War. Every Problem.

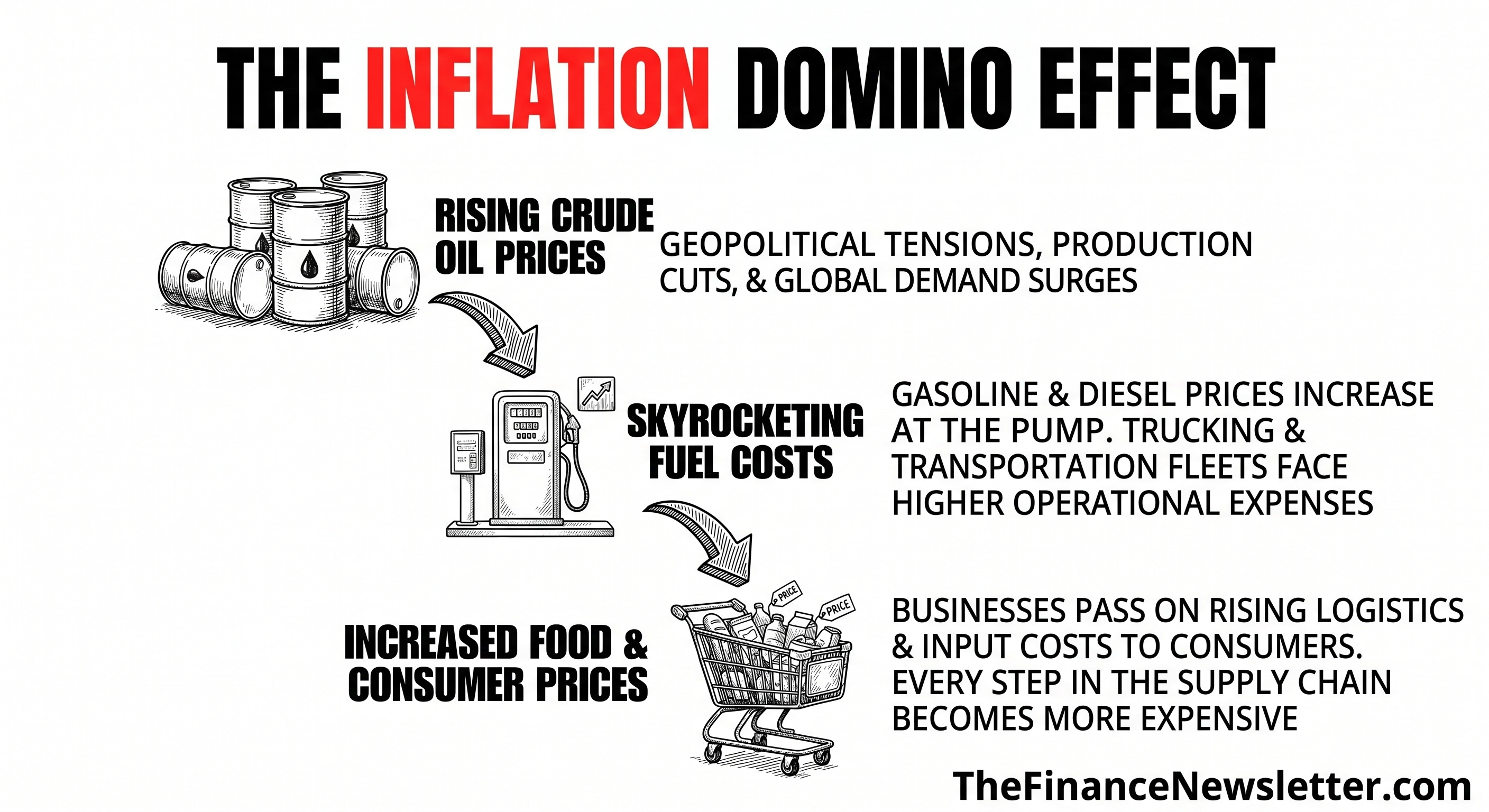

The Iran war, now entering its 8th week, is the engine behind almost every major economic problem on this list. Follow the chain reaction that most people aren’t tracking.

The Strait of Hormuz carries roughly 20% of the world’s oil and LNG supply. Iran’s disruption of that shipping lane removed 500 million barrels from global markets in 50 days. That’s $50 billion in lost oil production. As a result, gasoline prices surged 21.2% in March alone — the biggest single-month spike since the 1960s. That one number drove nearly three-quarters of the entire March inflation reading.

But here’s what most people miss: energy is an input cost for everything. Airlines pay more for jet fuel (Delta’s fuel bill jumps $2 billion this quarter). Construction crews burn diesel, which means PVC pipes cost 50% more and homebuilding stalls. Trucks carrying groceries burn more fuel, which creeps into every price on every shelf. The downstream effects on food, shipping, and agriculture haven’t fully hit yet. What we’ve seen is just the opening act.

Harvard’s Linda Bilmes estimates the total war tab could reach $1 trillion over the next decade. The Pentagon’s current bill is already understated. And the real costs — veteran care, rebuilding, compounding debt — arrive later. These are costs being handed directly to the next generation.

Real Wages Are Losing. Here’s What That Actually Means.

Since January 2021, cumulative consumer prices are up about 26%. Real hourly wages, after adjusting for inflation, grew only about 1.4% over the past year. That gap is the economic reality that 65% of Americans are expressing when they say rising prices are outpacing their income.

When 39% of Americans use credit cards to buy groceries, that tells you something critical. Savings are depleted. Debt is rising. The consumer spending that keeps the economy running is now running on borrowed time — literally. If real wages don’t outpace inflation and grow more quickly, this isn’t just an uncomfortable stretch. It becomes a spending contraction that hits corporate earnings hard down the road.

The AI Boom Is Real. So Is Its Dark Side.

While inflation erodes purchasing power for most Americans, something remarkable is happening on a parallel track. The AI spending boom is not slowing down — it’s accelerating.

TSMC posted profits up 58% year-over-year and raised its full-year forecast. The shift from generative AI (which answers questions) to agentic AI (which takes actions and completes tasks) is pushing chip demand to levels where supply can’t keep up. Cloud providers are collectively spending $600B+ on data centers this year alone. In my two decades in finance, the rule of thumb was always simple: follow the capital. And right now, capital is flooding into AI infrastructure at a pace we’ve never seen.

But here’s the uncomfortable flip side. Michael Burry — the investor who shorted the housing market before 2008 — just dropped a bombshell on tech investing. After reviewing over 1,000 annual reports going back a decade, he found a $1.7 trillion “earnings illusion” in Nasdaq 100 stocks. The cause? Tech companies give employees stock as pay — a very real cost — but many haven’t been fully accounting for it in their reported earnings. Of every dollar of GAAP-blessed earnings per share, shareholders actually receive only about 83 cents of real value. Companies flagged include Meta, Palantir, Shopify, CrowdStrike, Datadog, and Workday.

If Burry is even half right, the stocks sitting inside millions of 401(k)s and index funds are worth less than their price tags suggest. This isn’t a reason to panic. It is a reason to think carefully about what you own and why.

Apple’s Leadership Transition Is More Significant Than It Looks

Tim Cook handing the CEO role to hardware chief John Ternus on September 1 isn’t a routine transition. It’s a strategic bet on where the next era of tech gets won.

Cook grew Apple from a $330 billion company to a $4 trillion one — a 12x increase. But the company has stumbled into AI, failed to break into new hardware categories (the car project was quietly abandoned, Vision Pro has found few buyers), and has repeatedly delayed its most ambitious Apple Intelligence features. Ternus — the man responsible for the M-series chips and the physical design of every Apple product — is taking over at a moment when hardware plus AI, not software alone, may define the next competitive moat.

If Apple can position itself as the device layer that runs AI privately and securely — something no competitor is doing at scale — it could define the next decade of consumer technology. That’s the bet. It’s not guaranteed. But it’s worth watching closely.

China Just Changed the Future of Transportation

Greater Bay Technology, backed by China’s GAC Group, just moved all-solid-state EV batteries from the laboratory to mass production — targeting GWh-level output in 2026. These batteries carry 2x+ the energy density of current lithium-ion cells, a potential driving range over 620 miles per charge, faster charging, and dramatically improved safety. They don’t catch fire under stress tests.

When economies of scale kick in over the next 3-5 years, these batteries make internal combustion engines look like dial-up internet in a fiber-optic world. China already produces solid EVs in the $10,000-$15,000 range. Add this battery technology, and you’re looking at a global disruption of the $3 trillion automobile industry that’s moving faster than most investors have priced in. The companies positioned early in rare earth supply, battery materials, and EV infrastructure are going to benefit enormously.

My Advice

The right move isn’t “all in” or “all out.” It’s knowing what risks you’re running and positioning with intention.

First, protect against inflation. Cumulative 26% price increases since 2021 have already eroded significant purchasing power. Cash sitting in a low-yield account is losing real value every day. High-yield savings accounts paying 4-5%, Treasury bills, TIPS, and energy ETFs all provide inflation protection that most people are ignoring.

Second, stay in AI infrastructure selectively. Distinguish between the picks-and-shovels plays — TSMC, ASML, memory chip makers, data center power providers — and the AI-branded companies with more press releases than revenue. The former are benefiting from a real, structural capex cycle. The latter carry much higher valuation risk.

Third, audit your tech concentration. If your index fund or 401(k) is 80-100% in big tech, run Burry’s question on it: are those earnings real, or are they adjusted figures that overstate actual value? A little international exposure, some value stocks, and dividend payers can meaningfully reduce your risk without sacrificing long-term growth.

Fourth, watch housing as a leading indicator. When housing prices crack, consumer confidence typically follows. March’s home sales at their worst level since mid-2025 is a warning sign. A crack in housing would hit bank stocks, consumer spending, and the broader economy faster than most people expect.

Fifth, think in decades on EVs and rare earths. The solid-state battery breakthrough isn’t a 2026 story — it’s a 2028 to 2033 story. The companies building that infrastructure right now — rare earth producers, battery material suppliers, EV charging networks — are early in a decade-long trend with government-backed tailwinds.

Final thought: Uncertainty is at a record high. Markets are near all-time highs. That paradox is both the defining risk and the defining opportunity of this moment. The investors who understand both sides of that equation, and act deliberately, are the ones who build real wealth through chaos.

👉 To get smarter with money follow me on X /Twitter; Instagram Threads; Facebook; or BlueSky (and turn on notifications)

(2) Important Finance News

📬 Today we’ll look at:

1) Inflation Is Back — and the Worst Is Still Ahead

2) The Iran War Is Making America's Housing Crisis Even Worse

3) The Stock Market Is at All-Time Highs. Consumer Sentiment Is at All-Time Lows. Who's Right?

4) AI Adoption Is Real, and So Are the Layoffs

5) The Ticking Time Bomb in Your Retirement Accounts

🤔 But first, Do you trust the current stock market rally?

1. Inflation Is Back — and the Worst Is Still Ahead

The Bureau of Labor Statistics reported this week that the March Consumer Price Index came in at 3.3% year-over-year — the highest reading in nearly two years, and well above the Federal Reserve’s 2% target that hasn’t been met since February 2021.

The single biggest driver was gasoline. Gas prices surged 21.2% in March alone — the largest single-month percentage increase in records dating back to the 1960s. That one category accounted for nearly three-quarters of the entire March inflation reading. And it’s almost entirely a product of the Iran war disrupting the world’s most critical oil shipping lane.

The part that should concern you most is what hasn’t happened yet. When energy costs spike, they take weeks or months to bleed into food prices, trucking costs, manufacturing, and retail. The 3.3% reading may actually be the low point before things get harder. Even before March’s surge, a separate Fed-favored inflation gauge showed a 4.1% annual rate over the three months ending in February. The pipeline of inflation is still filling up.

Cumulatively, prices are up about 26% since January 2021. Real hourly wages, after adjusting for inflation, grew only about 1.4% over the past year. That gap — 26% price growth versus 1.4% real wage growth — explains why 65% of Americans say rising prices are outpacing their income, and why 39% are using credit cards to pay for groceries. When people use credit to buy food, it signals savings are depleted and spending is running on borrowed money.

The Fed’s situation is difficult. It needs high rates to fight inflation — but high rates slow economic growth, crush housing affordability, and squeeze borrowers at exactly the moment they can least afford it. There’s no clean exit from this corner.

My advice: Treat inflation as a permanent feature of your financial planning, not a temporary inconvenience. Assets that have historically outpaced inflation — stocks (selectively), real estate, commodities, and inflation-protected securities — deserve a larger share of your portfolio. If you’re holding cash earning below the inflation rate, you’re losing purchasing power every single day without making a single bad decision.

2. The Iran War Is Making America’s Housing Crisis Even Worse

The Iran conflict is worsening one of America’s most severe housing shortfalls, driving up costs across virtually every building category at a moment when the market was already under extreme pressure.

PVC pipe prices have surged over 50% since the conflict began. Aluminum is spiking after Iranian strikes in Abu Dhabi and Bahrain disrupted Gulf-region supply chains. These materials show up in nearly every residential and commercial project — in plumbing, window frames, HVAC systems, and electrical conduit. When input costs jump like this, developers face three choices: absorb the loss, raise prices, or stop building. Most are choosing the last two.

Projects that were already strained by labor shortages and tight financing are stalling or getting cancelled outright. The only construction segment holding up right now is data centers — where AI demand creates enough urgency and profit margin to absorb higher costs. Every other sector is taking a hit.

Billionaire developer Stephen Ross, the man behind Hudson Yards, called housing affordability “the biggest issue going forward” this week. He acknowledged that Trump’s $200 billion mortgage bond initiative is a step — but said it’s “not enough” to fix a problem this structural. The housing shortage in America — already estimated at 4 to 7 million units before this war began — is getting worse, not better.

March existing home sales came in at 3.98 million annualized — the worst reading since mid-2025. The spring selling season, which is typically the strongest of the year, got off to its worst start in recent memory. With 30-year mortgage rates still hovering around 7%, first-time buyers are locked out. With construction costs rising and financing tight, builders aren’t filling the gap fast enough.

My advice: If you’re waiting for housing prices to fall sharply, the math isn’t working in your favor. The supply shortage is structural and getting worse — not better. For investors, residential REITs and single-family rental operators continue to benefit as millions of would-be buyers remain permanently sidelined in the rental market. For renters planning to buy eventually, extend your timeline and build savings aggressively in a high-yield account while rates stay elevated.

3. The Stock Market Is at All-Time Highs. Consumer Sentiment Is at All-Time Lows. Who’s Right?

The stock market’s strong performance may be built on shakier ground than most investors realize — a concern that crystallized around bombshell analysis published by Michael Burry, the investor who famously shorted the 2008 housing bubble.

Burry published findings this week showing that Nasdaq 100 tech earnings have been overstated by 42% over the past decade. After reviewing more than 1,000 annual reports from the period ending fiscal 2025, he identified a $1.7 trillion “earnings illusion” tied to improper treatment of stock-based compensation. Companies pay employees partially in stock — a real cost — but many tech firms haven’t been fully counting that cost when reporting their adjusted earnings. “Of every dollar of earnings per share that GAAP blesses, shareholders see only 83.49 cents,” Burry wrote. Companies he flagged include Meta, Palantir, Shopify, Datadog, Workday, CrowdStrike, and Zscaler.

This comes on top of a market that’s already running hot on two forces that may not last. First, AI chip demand has caused Micron’s 2027 earnings estimates to surge from $19 to $101 per share since last October. Second, the Iran war has boosted energy company earnings forecasts by roughly one-third since late February. Both forces could fade — and if they do, valuations that look reasonable today could start looking stretched fast.

The contrast with how ordinary Americans feel is stark. The University of Michigan’s consumer sentiment index just fell to its lowest reading in the survey’s history — a survey that dates back over 70 years. A CBS News poll found 63% of Americans say the economy is “bad” — even with unemployment at 4.3%. Markets and consumers are telling completely opposite stories about the state of the economy. One of them will be proven right.

My advice: Don’t over-concentrate in any single sector. If your portfolio is 80% or more in big tech, rebalancing toward value stocks, dividend payers, and international markets reduces risk without sacrificing long-term growth potential. More importantly, understand what you actually own. The S&P 500 today is heavily weighted toward a handful of AI and tech names. Know what’s inside your index fund

.

4. AI Adoption Is Real, and So Are the Layoffs

Artificial intelligence has become the leading stated reason for corporate layoffs in 2026 — a dramatic escalation from where things stood just a year ago.

AI accounted for 25% of all tracked U.S. layoffs in March — up from just 5% throughout all of 2025 — according to outplacement firm Challenger, Gray & Christmas. Snap is cutting 16% of its full-time workforce, with CEO Evan Spiegel citing AI-enabled streamlining. Meta is cutting roughly 8,000 employees in May, with more cuts later in the year, as the company’s Metaverse bet unwinds into an AI pivot. Block cut 40% of its workforce, with CEO Jack Dorsey saying AI is doing many jobs “better and less expensively than humans.” Salesforce, Oracle, Atlassian, and Pinterest made similar announcements with similar language.

At the same time — and this nuance matters — AI is genuinely delivering real results. A Morgan Stanley report published this week found that one-quarter of all S&P 500 companies reported at least one quantifiable AI impact in Q1, up from 13% a year ago. Bank of America says AI saves them the equivalent of 2,000 software engineers. Hasbro cut concept-to-prototype time by 80%. Altria reduced marketing content creation time by 50%.

Both things are true simultaneously. AI is replacing real tasks. And some companies are using “AI” as convenient cover for restructuring they planned anyway. Whether the reason is genuine or strategic may not matter to someone who just lost their job.

For workers, the message from engineering professor Ahmad Banafa is blunt: “It’s not gonna stop. This is just the beginning.” The window to build AI skills is open right now — but it won’t stay that way.

My advice: If your role involves writing, coding, analysis, customer service, or any language-based, repetitive process — build AI fluency now, not later. The workers who learn to work with AI will have far more leverage than those competing against it. Get certifications. Use AI tools daily. For investors, companies successfully deploying AI to reduce headcount have a direct path to expanding profit margins — watch for operating leverage improvements across finance, tech, and communications sectors in the next few earnings seasons.

5. The Ticking Time Bomb in Your Retirement Accounts

Multiple economists and investment managers are warning about a brewing risk at the intersection of private credit markets and the life insurance industry — a risk that could directly affect millions of Americans through their retirement savings.

Private credit — lending done by private funds rather than traditional banks — has grown into a nearly $1.8 trillion market. Life insurance companies became some of its biggest participants, pouring roughly $849 billion into private credit funds by 2024, according to Federal Reserve researchers. That’s more than double what it was in 2014. They did this to earn enough return to fund the annuity payments — steady retirement income — promised to their policyholders.

That setup worked when markets were calm. Now, stress is building. More investors are trying to exit private credit funds than are entering. Redemption requests at business development companies are rising. And because private credit is, by design, opaque — you can’t assess these holdings the way you can with a public stock or bond — it’s genuinely hard to know how bad the exposure is.

Andrew Milgram of Marblegate Asset Management warns of a potential “doom loop.” If enough retirees surrender their annuities out of fear, insurance companies must sell private credit assets into a weak market, pushing prices lower, creating more fear, triggering more surrenders — the same amplification mechanism that deepened the 2008 mortgage crisis. Economist Eileen Appelbaum put it plainly: “The lack of transparency surrounding private credit funds makes it impossible to evaluate just how vulnerable they are.”

The industry pushes back, noting that insurers primarily hold investment-grade private credit, not speculative loans. JPMorgan’s Aaron Mulvihill called the current selling “driven by fear, rather than fundamentals.” Both assessments can be true at once.

My advice: If you have an annuity or plan to buy one, ask your advisor specifically what assets are backing it and whether the insurer has meaningful private credit exposure. Any investment product labeled “private” or “alternative” carries less transparency and more liquidity risk than public market equivalents. Know what you own. If you’re nearing retirement and reliant on annuity income, this is exactly the kind of question a qualified financial advisor should help you answer before a stress event forces the issue.

💡 Andrew’s Analysis & Advice:

The Iran war drives energy costs up, which re-accelerates inflation, which erodes purchasing power, which pushes consumers toward credit — and stressed borrowers increase default risk in private credit markets. That same war drives up construction costs, deepening the housing shortage. The market sits near all-time highs on earnings that may be partially inflated, driven by forces (AI chip demand and war-driven energy profits) that could prove temporary. And companies are using AI to cut costs and workers at exactly the moment when consumer income is under its most pressure in years.

Five separate stories. One economic reality. The widening gap between what Wall Street is reporting and what Main Street is experiencing is the defining financial story of 2026.

My advice:

Move idle cash to a high-yield savings account or short-term Treasuries earning 4-5%.

Check whether your index fund is more than 50% concentrated in tech stocks.

Ask your financial advisor about your annuity’s underlying asset exposure.

Start building AI skills now — certifications, tools, daily practice.

Prepare for summer travel costs to run 15%+ higher than last year and budget accordingly.

👉 For daily insights, follow me on X/ Twitter; Instagram Threads; or BlueSky (and turn on notifications)

(3) Chart of the Day and Deep Dive

The Chart That Shows Chaos Is Here to Stay

💡 Andrew’s Analysis & Advice:

Stop and really look at this chart.

The World Uncertainty Index — a GDP-weighted measure tracking global economic and geopolitical uncertainty across more than 140 countries — just hit 105,000. Not 40,000, where it was during 9/11 and the Iraq War. Not 60,000, where COVID briefly pushed it. One hundred and five thousand. We are in territory this index has never seen before.

And yet, the stock market is near all-time highs. That’s the paradox you need to understand.

What this chart is actually measuring: Sourced from Ahir, Bloom, and Furceri and distributed through the Federal Reserve’s FRED database, this index tracks how often the word “uncertainty” and related terms appear in quarterly economic reports from the International Monetary Fund — across every major economy, weighted by their share of global GDP. When the number rises, it means the most senior economic decision-makers in the world are explicitly saying they don’t know what comes next. At 105,000, they’re saying it at a volume never recorded in the index’s 30-year history.

Reading the timeline: 9/11 and the Iraq War pushed the index to roughly 40,000 in the early 2000s. The 2008 Global Financial Crisis kept it elevated but never beyond that level. COVID spiked it to around 60,000. The current reading is nearly double the COVID peak and more than double any previous reading in history. Something genuinely different is happening.

What’s driving the spike: Three forces are compounding at the same time. The Iran war has disrupted global energy markets at a scale the International Energy Agency called “the greatest global energy security threat in history.” AI is accelerating economic disruption faster than governments and policymakers can track or respond to. And geopolitical fragmentation — countries building separate trade networks, technology ecosystems, and financial systems — is eliminating the predictable rules-based global order that gave investors a stable framework for decades.

The historical pattern: When uncertainty spikes sharply, three things tend to follow. Businesses delay capital investment — they wait to see what happens before committing to hiring or expansion. Consumers pull back on big purchases like homes, cars, and travel — exactly what March’s housing data confirmed. And markets eventually price in the uncertainty through volatility, typically after a period of denial that can last months.

Based on the Fear & Greed Index sitting at 68 (Greed) and markets near all-time highs, we appear to be in that denial phase right now. The surface looks calm. Underneath, individual investor sentiment surveys show nine straight weeks of more bears than bulls. Short interest across the Russell 3000 is at a 15-year high. The market’s surface and its internals are telling very different stories.

The long-term lesson this chart teaches: Every previous spike in the uncertainty index — 9/11, 2008, COVID — eventually resolved. Markets set new highs after each one. The investors who held through those periods, or added to positions during them, captured the best long-term returns. Uncertainty is the price of entry for the best buying opportunities. The chart doesn’t predict a crash. It predicts volatility — and volatility, managed with discipline, is how wealth gets built.

My advice:

Hold some defensive assets. Gold, short-term Treasuries, and money market funds act as shock absorbers in high-uncertainty environments. Even a 10-15% allocation reduces portfolio volatility meaningfully when conditions get rough.

Diversify globally. No single country is immune to consequences at this scale of uncertainty. International developed markets and select emerging markets offer both relative value and exposure that’s uncorrelated with U.S.-specific risks.

Don’t try to time the market. The paradox of peak uncertainty is that markets move in counterintuitive ways. The single best action for most long-term investors is maintaining a diversified portfolio while avoiding panic-driven decisions triggered by headlines.

Think in decades, not quarters. The chart has been running for 30 years. Every spike resolved. The people who positioned for that resolution — patiently, deliberately — won. The people who let fear drive their decisions during the spike often missed the recovery entirely. That’s the timeless lesson hiding inside the most alarming chart in finance right now.

I hope you’re enjoying this newsletter — it takes a week to research and write, so please help support our journalism and:

Hit the LIKE button on this post and share this newsletter on social media or with friends & family:

Become a paid subscriber and get smarter with your money! (learn about the benefits here) (Get a free 30-day trial with this link):

(Your job can pay for this newsletter with its employee development budget — Send this email template to your manager)

Part II - Investing Research

4. Insider Trades

5. Top Stocks Right Now

6. Today’s Trade

7. Market Sentiment (Fear & Greed Analysis)

8. Macro Technical Analysis & Predictions

(4) Insider Trades (from Billionaires, Politicians, and CEOs):

When people with deep knowledge, such as politicians who set policy, executives who run the company, or legendary investors, put their own money on the line, pay attention.