💥 Robots, Reverse Aging, and Our Next 250 Years.

The Next 250 Years of Growth. The Robots Are Coming. The End Of Human Aging. AI Now Costs More Than Humans. And Much More!

Welcome back! Money affects every part of your life, so you deserve to understand it. This newsletter is for people who want to build wealth, become smarter, and make better financial decisions.

I spent 20 years in finance learning how money works. My goal is simple, I want to help you build wealth, make better decisions, and avoid costly mistakes.

America turned 250 this year. In 1776, nobody could have pictured cloud computing, AI chips, self-driving cars, humanoid robots, or medicine designed to restore damaged cells. The next 250 years will produce changes that feel just as hard to picture today.

Some future leaders may come from companies that barely exist. Others may grow inside businesses we already know. Alphabet has search, cloud computing, YouTube, Android, Gemini, Waymo, and quantum research. Amazon has cloud computing, logistics, advertising, AI services, and access to hundreds of millions of customers. Nvidia supplies much of the computing power used to train and run advanced AI.

The opportunity is large. The risks are equally real. AI spending has grown faster than proven profits. Chip stocks are expensive compared to their earnings. Robots still struggle with many tasks that humans find simple. And cellular reprogramming has reached human testing, but its safety and value remain unknown.

This issue explains the companies that may shape America’s next growth era, Michael Burry’s bearish AI bets, the true state of humanoid robots, the first human trial of cellular age restoration, and the steps I’m taking with my own money.

📬 Here’s everything in today’s issue:

Part I — The Big Picture (What You Need To Know)

(1) Market Breakdown & What it Means for You

(2) 5 Things You Need To Learn

Part II — What The Market Is Telling Us

(3) Market Psychology, Signals, and What Comes Next

(4) Interest Rates & Real Estate

Part III — Investment Research & Analysis

(5) Insider Trading Alerts

(6) Stocks Beating the Market

(7) The Smartest Trade I See Right Now

Part IV — The Financial Playbook (What To Do Right Now)

(8) Practical Tips & Advice

(9) A Lesson Most People Learn Too Late

(10) You Asked, I Answered

Want more of our insights in your Google Searches and AI answers?

Choose TheFinanceNewsletter.com as a preferred news source. You’ll see our content in more of your results. Add us in one click (and check the box)!

Part I: The Big Picture (Everything You Need To Know)

(1) Market Breakdown & Takeaways

What happened, why it matters, and what’s next.

Economy

The US added just 57,000 jobs in June, well below expectations. The unemployment rate fell to 4.2%, but only because 720,000 people left the workforce.

Labor force participation fell to 61.5%, the lowest reading outside the pandemic since 1976.

Markets

Wall Street analysts expect S&P 500 companies to report 22.5% earnings growth for Q2 (per FactSet), the highest forecast since 2021. Earnings season starts Monday, July 14, when JPMorgan Chase reports.

US stocks are the most expensive they have ever been. The S&P 500’s cyclically adjusted price-to-earnings ratio (its price compared to 10 years of earnings) crossed 40. Bloomberg found that if you strip out AI’s unusual earnings growth, the ratio passes 68, higher than the 2000 peak of 44.2 and the 1929 peak of 32.6.

Market concentration is at a multi-decade extreme. The 10 biggest stocks in the S&P 500 now control about 40% of the entire index, up from a 27% high during the 1999-2000 dot-com peak.

Nvidia lost nearly $1 trillion in market value in under two months and now trades at 18 times its expected earnings for next year, its cheapest level since 2019, even though it still controls 97% of the market for AI data center chips.

Memory chip stocks fell hard. Micron, SK Hynix, and Samsung shares dropped more than 20% from recent peaks as investors bet that growth has peaked, even with strong AI demand.

SK Hynix raised $26.5 billion in its US market debut, the largest US listing ever by a foreign company. The stock opened 14% above its offering price.

Small-cap stocks had their best first half since 1991, and the Russell 2000 now trades at a higher price compared to earnings than the S&P 500.

A 30-year US Treasury bond auction priced at 5.06%, the highest yield since 2007. The government’s long-term borrowing costs keep rising.

Personal Finance

Nearly half (49%) of American adults under 30 now live with a parent, per the Federal Reserve, up 12 percentage points from 2019.

Trump Accounts officially launched July 4. Any child under 18 can get one, contributions cap at $5,000 per year, and babies born 2025-2028 get $1,000 seeded by the federal government.

Obamacare marketplace premiums are set to rise a median of 14% next year, the second straight year of double-digit increases.

Housing

US existing home sales fell 2.4% in June while the median sale price hit a record $440,600. The 30-year mortgage rate rose to 6.49% as the Iran conflict pushed oil and bond yields higher.

Global Markets

Japan’s 10-year and 20-year bond yields hit 30-year highs while the yen trades near 40-year lows. The Bank of Japan is cutting its bond purchases just as Tokyo plans $2.29 trillion in new spending. If Japanese money parked overseas comes home to capture higher yields, it pulls capital out of US markets.

What This All Means for You:

The most expensive stock market in American history is being carried by 10 companies, funded with borrowed money, while the greatest investor alive sits on $397 billion in cash.

I know that’s a lot in one sentence, so let me break it down for you.

The prices come first. When you adjust for AI’s unusual earnings, the S&P 500 is more expensive than it was in 1929 and more expensive than it was in 2000. Think about that for a second. In my 20 years in finance, I watched two full boom-and-bust cycles up close, and the pattern before every bust was the same. Prices stopped reflecting businesses and started reflecting stories. When 10 stocks make up 40% of the entire index, you don’t really own 500 companies when you buy an index fund. Your returns depend mostly on just 10, and the other 490 barely move the needle.

Now look at who’s buying and who’s selling. Charles Schwab’s June data shows regular investors bought every dip, at a 2-to-1 ratio over selling, mostly in the same crowded tech names. At the same moment, Berkshire Hathaway’s cash reserves hit an all-time high of $397 billion. Warren Buffett has spent 60 years buying when others are fearful. Right now, he’s doing the opposite of what regular investors are doing. When the most patient investor in history refuses to spend, he’s telling you that nothing looks cheap to him. Watch what the smartest money does, and ignore what it says.

The bond market is sending the same warning in a different language. A 30-year Treasury just priced at 5.06%, the highest since 2007. Stocks compete with bonds for your dollars. When the government pays you 5% guaranteed, every risky asset has to promise more to earn its place in your portfolio. Expensive stocks and 5% bonds cannot both be right forever.

Then there’s Japan, which I think is the most underpriced risk in the world right now. Japanese bond yields just hit 30-year highs while the yen sits near 40-year lows. For decades, investors borrowed cheap Japanese money and put it into US stocks and bonds. That only works while Japanese rates stay near zero. They aren’t staying near zero anymore. If that money starts flowing home, US stocks and bonds lose one of their biggest sources of buying. Most Americans have never heard of this trade. It touches nearly every asset they own.

The jobs report ties the domestic picture together. Only 57,000 jobs added in June, and the unemployment rate fell for the wrong reason (720,000 people quit looking for work). A shrinking workforce is why housing is unaffordable for the young, why 49% of adults under 30 live with their parents, and why the Fed is stuck. Inflation is running hot at 4.2% while hiring cools. The Fed can fight one of those problems at a time.

Now put it all together. Record prices, record concentration, record corporate cash waiting in reserve, the highest long-term borrowing costs in 19 years, a weakening job market, and a foreign funding source drying up. Any one of these problems alone is manageable. Together, they describe a market priced for perfection at the exact moment the world is getting less perfect.

Does that mean sell everything? No. I’ve seen expensive markets stay expensive for years, and the people who went all-cash in 1996 missed four more years of gains. Timing the top is a loser’s game. Managing your risk is a winner’s game.

My advice is to do five things this week:

First, rebalance. If tech has grown to over 80% of your portfolio, trim it back to your target. You’re locking in gains without making a prediction.

Second, hold some cash and actually get paid for it. Money market funds and Treasury bills pay around 4-5% right now. Cash finally pays you again.

Third, diversify beyond the top 10. An equal-weight S&P 500 fund (like RSP) or a small-cap value fund gives you America without the concentration risk.

Fourth, keep investing the same amount automatically on schedule (called dollar-cost averaging), no matter what the headlines say. The best returns of my investing life came from shares I bought during scary headlines.

Fifth, circle Tuesday, July 14 on your calendar. The June inflation report and JPMorgan’s earnings land that same day, and together they’ll set the market’s direction for the rest of the summer.

(2) 5 Things You Need To Learn

The biggest ideas & trends to pay attention to, and what comes next.

📬 Today we analyze:

1) 🔮 America Turned 250, These Companies Will Define the Next 250 Years

2) 🤖 AI Now Costs More Than the Employees It Replaced

3) 🚨 Michael Burry Says the End Is Near for AI Stocks

4) 🤖 The Decade of the Robot Has Started

5) 🧬 The First Human Trial to Reverse Aging Just Began

🤔 But first — Will humanoid robots become common by 2035?

🔮 America Turned 250, these Companies Will Define the Next 250 Years

Which companies will still matter 250 years from now? In 1776, nobody could have predicted that a computer chip maker called Nvidia would one day be the most valuable company in the country. That should teach you humility before making any prediction. But some patterns are worth betting on.

AI is the obvious starting point. OpenAI and Anthropic are positioned to dominate the intelligence layer of the economy, and Amazon’s cloud business keeps growing as it rents computing power to nearly every company that needs it. But if I had to pick one public company built for the next century, it’s Alphabet. Beyond search, cloud, and Android, Alphabet’s Gemini models compete at the frontier of AI, it owns roughly 14% of Anthropic and 6% of SpaceX, it leads in quantum computing, and its Waymo self-driving unit is expanding fast. Alphabet is a collection of bets on the future, and several of them are already paying off.

Energy is the quieter story. Data centers are consuming electricity at a pace the grid wasn’t built for, and demand keeps rising. Exxon Mobil and Chevron dominate today, but the long-term prize may belong to fusion startups like Commonwealth Fusion Systems, Helion Energy, and Zap Energy. Whoever cracks cheap, clean, unlimited power owns the next century. Every technology you’re excited about (AI, robots, longevity) runs on electricity first.

My advice is simple. You don’t need to pick the exact winner. In 1776, the smart move wasn’t guessing which merchant would dominate. It was owning a piece of American growth itself. A total market index fund like VTI does that today. Then, if you want upside, add small positions in the themes above (AI, energy, healthcare) and hold them for decades. Time in the market builds wealth. Guessing the future is entertainment.

🤖 AI Now Costs More Than the Employees It Replaced

Uber burned through its entire 2026 AI coding budget in just four months. Read that again. The technology that was supposed to replace expensive human workers is, right now, more expensive than the workers it replaced. Companies are laying people off to fund AI tools that cost more than the people they just let go.

The numbers are hard to believe. By March, 84% of Uber’s engineers were using AI coding tools, and about 70% of the company’s new code comes from AI. Yet Uber’s own president admitted the spending doesn’t clearly connect to useful products. Microsoft, which has invested about $13 billion in OpenAI, told some of its own engineers to stop using an AI coding assistant because the bills got out of hand. Meanwhile, the biggest tech companies (Microsoft, Amazon, Alphabet, Meta, and Oracle) have announced $740 billion in capital spending this year, up 69% from 2025, while more than 115,000 tech workers have been laid off in 2026 alone.

Here’s the part that should worry investors. An MIT study found AI automation is economically worthwhile in only about 23% of jobs. For the other 77%, humans are still cheaper. And the prices companies pay for AI today are fake. OpenAI spends nearly $2 for every $1 it earns running its AI models for customers, and projects $14 billion in losses this year. Anthropic and GitHub both moved customers to usage-based billing this spring, and analysts expect enterprise AI bills to rise another 30-50% when prices reflect real costs. The discounts are ending while the dependence keeps growing.

The market noticed in June. Chipmakers lost roughly $1.3 trillion in value in a single session, the worst day for the semiconductor index since March 2020. Investors were voting against the timeline, since they still believe in the technology but doubt the profits will arrive on schedule. The internet was real, and it still crashed in 2000. What came after the crash was an internet that finally paid for itself. AI is headed for the same sorting.

If you listened a few weeks back when I said the AI trade was getting crowded and the easy money had been made, this week explained why. My advice has three parts. First, look at how much of your portfolio is in AI stocks. If they've grown into a huge share of it, sell some. A good test is to imagine those stocks falling 40%. If that would keep you up at night, you own too much. Second, favor companies that profit from AI usage regardless of which model wins (cloud providers, power producers, and the companies actually saving money with AI, rather than the ones burning money selling it). Third, in your own career, become the person who uses AI to produce measurable results. The layoffs punish people whose output can’t be measured. Right now, the only companies reliably making money from AI are the ones selling it. The companies buying it are still waiting for the payoff.

🚨 Michael Burry Says the End Is Near for AI Stocks

Michael Burry is betting against Nvidia, Tesla, Palantir, Micron, Caterpillar, Applied Materials, and the iShares Semiconductor ETF. Burry is the investor who bet against the housing bubble before 2008 and made a fortune when everyone said he was crazy. Now he’s pointing his warning at the AI boom, and his language has turned dark. In recent posts he wrote that the end is nigh and called the AI story a mass addiction that may die a death by a thousand cuts.

His argument rests on two statistics. First, AI chip stocks have massively outperformed the cloud giants (Microsoft, Amazon, and Alphabet) who actually pay for the AI buildout. That’s backwards. The suppliers are being valued higher than the customers funding them. Second, compared to its expected earnings for next year, the Philadelphia Semiconductor Index trades near the top of its 15-year range. Burry’s core point is that the AI boom feeds on itself. Chip stocks rise because tech giants announce spending. Equipment makers rise because chip companies build capacity. Investors treat every new spending announcement as proof demand will grow forever. He bet against Micron on July 1 at $1,051.87 after the stock rose nearly 700% in a year, blaming the rally on fear of missing out and the greater fool theory (the belief that someone will always pay more than you did).

The scale of what he’s betting against is enormous. Nvidia hit $5 trillion in value last October. AI spending by the biggest cloud companies (Microsoft, Amazon, Alphabet, and Meta) could reach $725 billion this year. And Bank of America’s bubble risk indicator has the semiconductor sector at 0.91, near-bubble territory. The market has started listening. The semiconductor index fell 6.3% on July 1 and another 5.5% on July 2.

Now for the honest caveat. Burry has been early before, and early feels identical to wrong for a long time. He was warning about housing years before it broke. He has also made bearish calls since 2008 that never paid off. When I worked on Wall Street, the saying was that the market can stay irrational longer than you can stay solvent, and that rule has bankrupted more smart people than dumb ones.

My advice is to treat Burry’s warning as a reason to check your own portfolio, and nothing more. Calculate what percent of your portfolio depends on AI spending continuing (chips, the biggest tech stocks, and the index funds heavy in both). If a 40% drop in those stocks would set back your retirement or force you to change your plans, sell some now while prices are high. Keep 6-12 months of expenses out of stocks entirely. And keep buying your diversified index funds on schedule, because the market rewards discipline over drama. The goal is to survive every crash and stay invested for every recovery.

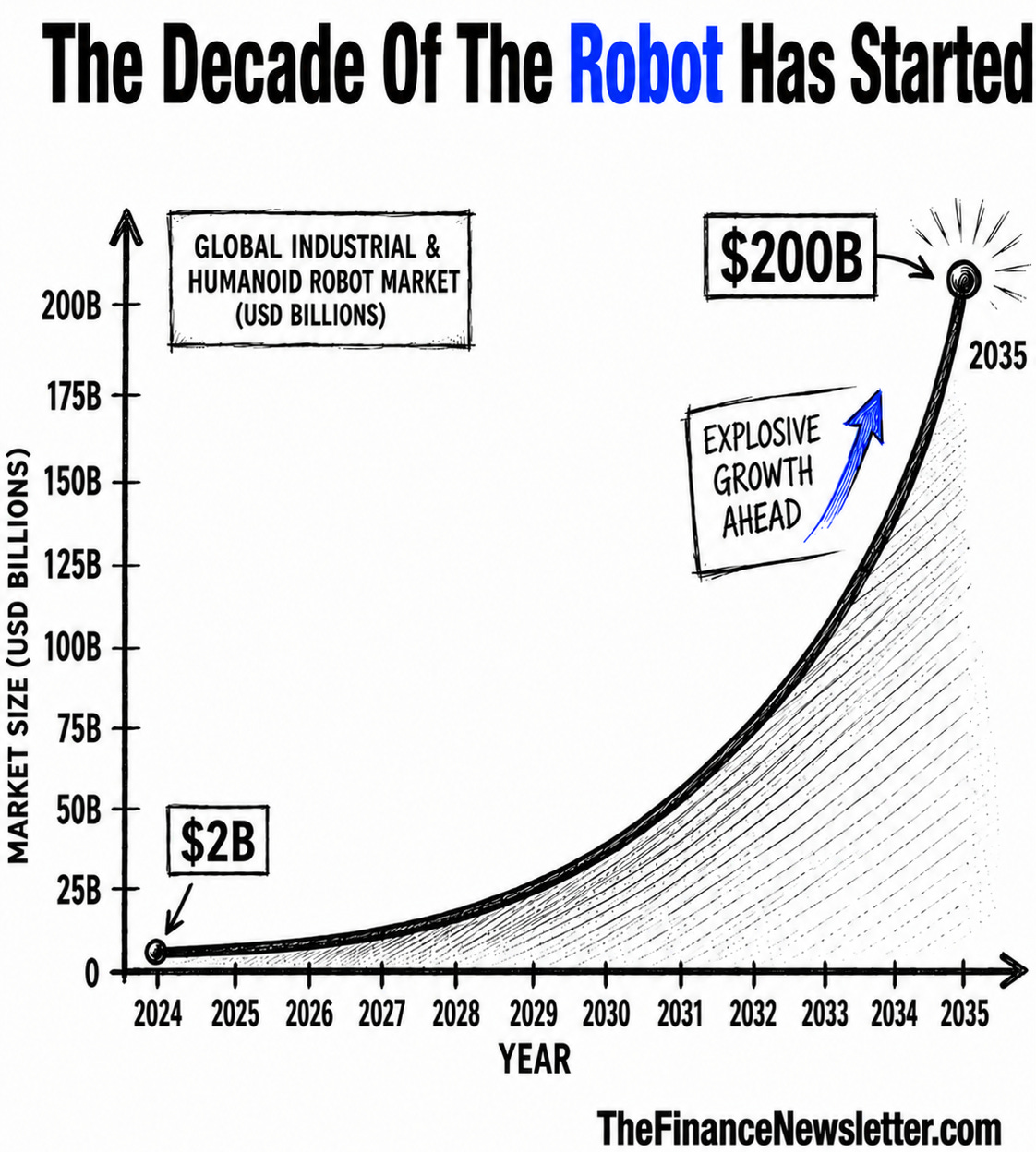

🤖 The Decade of the Robot Has Started

The decade of the robot has started. Barclays projects the humanoid robot market could grow from about $2-3 billion today to $200 billion by 2035. Wedbush’s Dan Ives goes further, calling humanoids the biggest opportunity in physical AI (AI that works in the real world instead of on a screen) and forecasting a market worth trillions over the next decade. Wall Street is starting to bet on a workforce that never asks for a raise, never retires, and works 24 hours a day.

The demand story is demographics. Populations are aging across the developed world, and fewer people want physically demanding jobs. I expect humanoids to scale first in manufacturing, logistics, and construction, with healthcare, elder care, and education following after 2030. Those aren’t science fiction use cases. Those are labor shortages that exist today with no human solution in sight.

Here’s the uncomfortable part for American investors. China is winning. Barclays estimates China accounted for 85% of humanoid robot installations last year and builds machines at roughly half the Western cost, around $50,000 each. China installs about 300,000 industrial robots a year versus about 34,000 in the US, and its robot density has grown 600% since 2016. JD.com is mobilizing up to 500,000 workers to collect movement data for training robots, a data advantage US rivals haven’t matched. Even Nvidia picked Chinese company Unitree’s H2 robot for its first research-grade humanoid platform.

The investing problem is that the best pure humanoid companies are still private. So the public-market options are the suppliers. Wedbush’s AI Revolution ETF holds Micron $MU, AMD $AMD, Broadcom $AVGO, and Nvidia $NVDA. For broader exposure, the KOID ETF holds 50 stocks across the humanoid supply chain (chips, sensors, and robot makers) and has returned 66.8% since its June 2025 launch versus 29.1% for the S&P 500.

My advice is to treat this like the internet in 1996. The theme is real, the timeline is long, and most of today’s names won’t be the eventual winners. So use a basket instead of a lottery ticket. A small position (I’d cap it at 5-10% of your portfolio) in a supply-chain ETF like KOID gives you the trend without betting your future on picking the one right robot company. Then be patient for a decade. The people who got rich off the internet weren’t the ones who traded it in 1999. They were the ones who still owned it in 2015.

.

🧬 The First Human Trial to Reverse Aging Just Began

Life Biosciences, a Boston longevity company, announced the first FDA-approved human trial of a drug designed to reverse aging in cells. Scientists injected their ER-100 drug into the eye of a glaucoma patient, attempting to rejuvenate cells in the optic nerve and restore sight. The technology is called cellular reprogramming, and the company hopes to apply it to other organs like the liver, and maybe someday the brain. This is the biggest tangible step the longevity industry has ever taken from promise to proof.

Keep your expectations in check. This trial is in its earliest stage. Cellular reprogramming caused cancerous cells to form in some early mouse research. And the company’s co-founder, Harvard geneticist David Sinclair, has a track record of overhyping longevity treatments before the science supported them. A drug that makes you 21 again is nowhere close.

But follow the money, because the money is serious. Jeff Bezos and Sam Altman are funding longevity startups. Eli Lilly and Merck are putting Big Pharma cash into the space. When billionaires who can buy anything spend their fortunes on one problem, they’re telling you what they think the most valuable product in human history will be. More healthy years. The market for that product is every human being alive.

I follow longevity research closely, and here’s my honest take. The investable breakthroughs will take years, the failures will outnumber the wins, and the first profits will come from ordinary treatments (eye disease, liver disease) long before anything resembling age reversal. Watch Eli Lilly and Merck, since they have the cash to buy whichever startup actually cracks it.

My advice runs in two directions. As an investor, keep longevity exposure small and inside big pharma names that make money today. As a human, act on what’s already proven free of charge. Sleep, strength training, protein, and not smoking are the only age-reversal protocol with 100 years of evidence behind them. The cheapest longevity drug ever invented is the gym and a good night’s sleep.

🧠 Connecting The Dots

Everything we covered this week points to the same pattern. Massive money is chasing the transformation of human work and human life, and the money is arriving faster than the results.

You can see the pattern repeat from every angle. When we asked which companies will own the next 250 years, the answers were all AI, energy, and health. Then we saw that AI currently costs more than the workers it replaced, which means the price of building that future is higher than the value it produces so far. Michael Burry is betting that this gap breaks the boom. Humanoid robots show the next wave of spending starting before the first wave has paid for itself. And the reverse-aging trial shows the same thing happening in medicine, where billions flow into anti-aging research before a single treatment works. In every case, belief is running ahead of proof, and prices are running ahead of profits.

History says two things happen from here, and they sound like they contradict each other. The technology wins, and many investors lose. The railroads transformed America and bankrupted a generation of railroad investors. The internet changed everything and still erased trillions in 2000. Jeremy Grantham, the 87-year-old investor who called both the dot-com and 2008 crashes, made exactly this comparison last week while selling his AI holdings. The lesson from 250 years of American markets is that transformation and bubbles travel together. You can believe in the technology and still refuse to overpay for it.

All of these changes will touch your life too, well beyond your portfolio. AI threatens jobs, robots replace labor, and longevity extends careers. Together they mean your working life will be longer than any generation before you, and the jobs themselves will keep changing. The best response is the same for your money and your skills. Diversify, keep learning, and never depend on a single employer, a single stock, or a single job title.

So here’s what I’d do with this pattern of high prices and unproven profits. Own the transformation through broad index funds so you win no matter which company wins. Cap any single theme (AI, robots, longevity) at a small slice you could lose without changing your life. Keep cash earning 4-5%, because if prices fall hard, that cash lets you buy great companies at a discount, and buying quality at a discount is how investors got rich after 2000 and 2008. And most important of all, invest in yourself. Careers are getting longer, and technology will keep changing what jobs look like. Your skills are the most valuable asset you own.

Bubbles are how the future gets funded. Just make sure you’re not the one holding the bill.

I hope you enjoy reading this newsletter — Please support us and:

Hit the LIKE button on this post

Share this newsletter on social media or with friends & family:

Become a paid subscriber and get smarter with money! (learn about the benefits here) (get a free 30-day trial with this link):

(Your job can pay for this newsletter with its employee development budget — Send this email template to your manager)

Part II: What the Market Is Telling Us

3. Market Psychology, Signals, and What Comes Next

4. Interest Rate Forecast & Real Estate Outlook

(3) Market Psychology, Signals, and What Comes Next

The psychology, signals, and data pointing to where the market goes next.

Fear & Greed Index: Neutral (49, recovering from Extreme Fear)

The Fear & Greed Index sits at 49 this week, a Neutral reading, and the trend matters more than the number. The index measures the emotions driving the stock market on a scale from 0 (extreme fear) to 100 (extreme greed), using seven market indicators. A month ago it read 26, a deeply fearful reading. A week ago it was 32. Today it’s 49. Investors are calming down fast.

The seven indicators are split. Market momentum shows greed, with the S&P 500 trading above its 125-day average. Options traders lean greedy too, buying more call options (bets on rising prices) than put options (bets on falling prices). But stock price strength and breadth both still register fear. More stocks are hitting 52-week lows than this rally would suggest, which means a few big companies are producing most of the gains while the average stock lags. Junk bond demand also signals fear, with investors still demanding extra interest to hold risky debt.

One year ago this index read 76, full greed. The drop from 76 to 26 and the climb back to 49 shows you how big the swings have been this year. The Iran conflict, the June chip selloff, and hot inflation moved investors from confident to scared, and now they’re moving back toward undecided.

My read on a Neutral reading after extreme fear is mildly positive. The best buying windows of my career came when this index sat below 30, and that window just closed. From here, sentiment can move in either direction, so let the July 14 inflation report and earnings season pick the direction instead of your emotions.

AAII Investor Sentiment: Neutral, Leaning Bearish (bears still outnumber bulls)

The AAII Investor Sentiment Survey comes in Neutral leaning Bearish this week, with 37.2% of individual investors bearish (expecting stocks to fall) and 36.3% bullish (expecting stocks to rise). The AAII survey has asked regular investors every week since 1987 whether they think stocks will rise or fall over the next six months, so it’s one of the longest-running measures of how everyday investors feel. Bearish sentiment has now stayed above its historical average of 31% for 22 straight weeks. That’s a long stretch of pessimism.

But the trend inside the numbers turned this week. Bullishness rose 4.9 points and bearishness fell 5.1 points, the biggest one-week improvement in months. And here’s my favorite detail. When AAII asked members how 2026 returns compare to their January expectations, 70.1% said the market has done better than they expected. So investors are pessimistic about the future while admitting they were too pessimistic about the present. Historically, this survey works best as an opposite signal. Periods of extreme fear have been better times to buy than periods of extreme greed.

Compare these survey answers to what investors are actually doing with their money and you get a strange split. Charles Schwab’s June trading data showed its customers bought stocks at a 2-to-1 ratio over selling, mostly in tech names like Nvidia, Micron, and Microsoft. So investors claim they’re bearish in surveys while buying tech stocks with their actual accounts. Trust what people do with their money over what they say in polls. And their buying shows they still believe.

My advice is to treat 22 weeks of pessimism as a positive setup. Markets rise when doubtful investors slowly put their money back in. If earnings season delivers, there’s a large group of pessimists who could turn into buyers.

Technical Analysis: Bullish (Weak Positive)

Technical analysis of the S&P 500 is Bullish, with one big test directly ahead. The short-term trend is Weak Positive and the long-term trend is Positive. The index closed at 7,543 and sits inside a rising trend channel, which means buyers have been willing to pay higher prices over time. That is the definition of an uptrend.

The number to watch is 7,560. The index is testing that resistance level right now (a price where many investors have sold in the past). A clean break above 7,560 is a positive signal that usually leads to more buying. A rejection there would likely mean a pause or a pullback toward the bottom of the trend channel. Either way, we’ll get the answer soon, and earnings season starting July 14 is the obvious trigger.

Volatility is worth noting too. The index moved 14.6% over the past 66 trading days, which is a lot of movement for a market slowly climbing higher. And traders now expect bigger swings in the Nasdaq-100 (the 100 biggest tech stocks) compared to the broad market than at any time since 2002. The message is that traders expect tech stocks specifically to keep swinging even if the broad market holds up.

My advice depends on where you are.

If you’re a long-term investor, ignore the resistance level and keep your automatic investments running. If you have new cash to invest, I’d split the money. Put half in now and half in after we see how the market handles 7,560 and the July 14 data. You don’t need to predict the outcome. You just need a plan for both outcomes.

Economic Indicators: Mixed (steady growth, hot inflation, miserable consumers)

The economic indicators are Mixed this week, and the tension between them explains the whole market. Start with what’s working. GDP is growing at 2.0%, right in its typical range. Unemployment sits at 4.2%, historically healthy. Expected market swings are calm (the VIX, a measure of expected market swings, sits at a quiet 17.96). The economy is functioning.

Now the problems. Inflation is running at 4.17%, more than double the Fed’s 2% target and rising, largely because the Iran conflict pushed oil prices up. The 10-year Treasury yield sits at 4.44%, keeping borrowing expensive for everyone from homebuyers to corporations. And consumer sentiment reads 44.8, the lowest level in the history of the measure. American consumers are as pessimistic as they have ever been recorded, even with jobs plentiful and the economy growing.

That last combination explains a lot. People have jobs and feel awful, because paychecks grew 3.4% while prices grew 4.2%. When inflation outruns wages, every month makes you a little poorer, and no jobs report fixes that feeling. High inflation also leaves the Fed stuck. New Fed Chair Kevin Warsh ended his June statement with a single clear promise to deliver price stability, which means rate cuts are off the table and rate hikes are now possible. Higher rates pressure stock prices, mortgages, and anyone carrying debt.

My advice is to prepare for inflation to stay high rather than hope inflation goes away. Keep your emergency fund in a money market fund earning 4-5% so inflation doesn’t quietly shrink your savings. Favor companies that can raise prices without losing customers. Pay down any variable-rate debt now, before the Fed decides the next move is up. And ask for the raise. In a 4% inflation world, a flat salary is a pay cut you agreed to.

The Bigger Picture: Neutral (the next move likely comes within two weeks)

My overall grade for this market is Neutral, and I expect the next big move to be decided within two weeks. Sentiment is improving (Fear & Greed at 49, and fewer investors expecting stocks to fall). Price trends are positive (a rising trend, testing resistance at 7,560). But the economics are the problem (4.2% inflation, a Fed talking tough, and stock prices above the 1929 and 2000 valuation peaks).

Here's how everything connects. The market recovered from June’s chip selloff because investors decided the selling went too far, and now the index sits right at that 7,560 resistance level while everyone waits for proof. That proof arrives Tuesday, July 14, when the June inflation report and JPMorgan’s earnings land the same morning. Cooler inflation plus the expected 22.5% earnings growth would likely push the market through 7,560 and turn 22 weeks of bearish sentiment into buying. Hot inflation plus any earnings miss would confirm the pessimists and probably send stocks back toward the bottom of the range, because a market priced for perfection falls hard on anything less.

The honest answer is that nobody knows which way the market goes from here, including me. What I know from 20 years of doing this is that markets caught between rising prices and worsening economic conditions tend to make big, fast moves once the answer arrives, and the investors who survive are the ones who prepared for both outcomes instead of betting on one.

My advice is to spend this weekend on a 30-minute portfolio checkup. Confirm your emergency fund covers 6 months. Confirm no single stock or theme is so large that a 30% drop would make you panic-sell. Confirm your automatic investments are on. Then let July 14 come. Preparation beats prediction every single time.

Want more of our insights in your Google Searches and AI answers?

Choose TheFinanceNewsletter.com as a preferred news source. You’ll see our content more often in your results. Add us in one click (and check the box)!

(4) Interest Rate Forecast & Real Estate Outlook

What’s next for mortgages, housing, and your money.

Interest Rate Prediction: Rates Are Going Up

Mortgage rates are heading higher in the short term, and I don’t say that happily. The Freddie Mac 30-year fixed rate rose to 6.49% this week from 6.43%, and the forces pushing rates up are getting stronger. The ceasefire with Iran is breaking down. Iranian forces fired on three ships in the Strait of Hormuz, the US struck 80 targets in response, and oil rose to $75 a barrel. Expensive oil raises inflation, inflation pushes bond yields up, and mortgage rates follow bond yields. That chain has driven rates all year, and the chain is pulling in the wrong direction again.

The Fed won’t help. May inflation came in at 3.4% on the Personal Consumption Expenditures index (the inflation measure the Fed watches most closely), June CPI is running above 4%, and Fed Chair Kevin Warsh has made price stability his single clear promise. Investors who expected 1-2 rate cuts this year now expect 1-2 rate increases instead. That’s a full percentage point swing in expectations. The soft June jobs report (just 57,000 jobs added) is the only force pulling rates down, and in my view the inflation data matters more right now. Tuesday’s July 14 inflation report is the next big test. My prediction is that mortgage rates hold near 6.5% or rise slightly in the coming weeks, and rates don’t fall meaningfully until the Iran conflict cools or the job market weakens much further.

For the full year, I still expect rates to average around 6.3%, which means the second half of the year should eventually bring mild relief from today’s levels. But I’d plan around a range of 6% to 6.5%, and I’d stop waiting for 5%.

Real Estate: Buyers Have More Negotiating Power Than They Realize

Buyers now have more negotiating power than they’ve had in years, and most people haven’t noticed. Existing home sales fell 2.4% in June even as the median sale price hit a record $440,600. Asking prices give you the clearer picture. They’re down 2.3% from a year ago, sellers are pricing realistically from day one, and there are more than 1.1 million homes for sale, the most since 2023. This week, homes sold faster than a year ago for the first time since April 2024, a sign that realistic prices are finally meeting real demand. And with inflation running 3.4% while home prices rise just 1.2%, houses are getting cheaper compared to everything else once you account for inflation.

Two more shifts matter. First, the 21st Century ROAD to Housing Act becomes law tonight, the biggest federal push to build more homes in decades. The law encourages cities to loosen zoning rules, speeds up environmental reviews, and (the part I find most interesting) removes the old rule requiring manufactured homes to be built on a permanent chassis, which opens the door to building real homes in factories at scale. More supply is the only permanent cure for unaffordable housing, and this law starts that process. Second, foreclosures have returned to 2019 levels. They’re still nowhere near 2008, but foreclosed homes now make up 1.3% of all listings, and the median foreclosed home sells at a 27.2% discount to its estimated value.

My advice:

If you’re a buyer, stop waiting for low rates and start using your negotiating power. Negotiate the price, and ask the seller to pay to lower your interest rate (called a rate buydown). You can refinance a rate later, but you can never refinance a purchase price.

If you’re a seller, price honestly from day one. Homes priced right are selling faster than last year, while overpriced listings sit unsold and lose attention.

If you’re an investor, foreclosures are the opportunity nobody’s discussing. Bank-owned homes (foreclosed homes the bank lists for sale after a failed auction) sell at a 27% median discount, concentrated in affordable metros like Pittsburgh, Baltimore, Dayton, and St. Louis. They’re sold as-is, with fewer photos and longer selling times, and that’s exactly why the discount exists. The discount is your payment for taking on the repairs and the risk.

👉For daily insights, follow me on X /Twitter; Instagram Threads; Facebook; or BlueSky (and turn on notifications)

Part III: Investment Research & Analysis

5. Insider Trading Alerts (Follow the Smart Money)

6. Stocks Beating the Market

7. The Smartest Trade I See Right Now

(5) Insider Trading Alerts (Follow the Smart Money)

The latest insider trades worth paying attention to.

Coherent Corp $COHR

I’m watching this one, and my rating is 8/10. Senator Sheldon Whitehouse, a Democrat from Rhode Island, bought between $15,000 and $50,000 of Coherent Corp $COHR stock, with the trade filed on July 8, 2026. Whitehouse sits on the Senate Finance and Budget Committees, which means he sees federal spending priorities and tax policy before the public does, including anything touching the AI and semiconductor buildout.

Coherent makes lasers and optical networking components, and here’s why that matters. AI data centers need to move enormous amounts of data between chips at light speed, and Coherent’s optical parts are one of the main products that do the job. Every dollar the biggest tech companies (Microsoft, Amazon, Alphabet, Meta, and Oracle) spend on data centers (a projected $750 billion this year) creates demand for Coherent’s parts. The stock has been one of the overlooked winners of the AI boom, and Coherent just signed a supply agreement with AXT to expand production capacity through 2028.

The timing is what catches my eye. A senator with budget oversight bought an AI supplier during the same month that memory chip stocks like Micron and SK Hynix fell more than 20% and famous investor Michael Burry declared the AI boom over. Either the senator is late to a crowded trade, or he expects the data center spending to continue regardless of what stock prices do. Politicians’ trades have historically beaten the market often enough that Congress keeps debating whether to ban them, and I pay attention when a member buys while a sector is falling instead of after prices have already risen.

My take is that Coherent supplies a real, revenue-producing piece of the AI buildout, but at $407 after a huge rise in price, most of the gain has already happened. Coherent stays on my watchlist. I’d get more interested if the price falls back toward its average over the past 200 days.

Energy Fuels $UUUU

I'm watching this one closely, and my rating is 7.5/10. Energy Fuels CEO Ross Bhappu bought 74,000 shares of his own company at $13.08, a total of $967,921, reported on July 7, 2026. That purchase brought his stake to 256,583 shares. A CEO putting nearly a million dollars of his own cash into his own stock is one of the strongest signals in investing. Executives sell for a hundred reasons, but they only buy for one. They think the price is going up.

Energy Fuels is America’s leading uranium producer and also mines rare earth elements, two materials the US is desperate to stop importing. The demand case is simple. AI data centers are forcing utilities to sign nuclear power deals, the federal government treats domestic uranium as a national security priority, and rare earths sit at the center of the US-China technology fight. Energy Fuels is one of the only American companies positioned in both.

The long-term picture is what makes this company interesting. Nuclear power is the only proven energy source that can feed data center demand around the clock without carbon, and Microsoft, Amazon, Alphabet, and Meta have all signed nuclear power agreements in the past two years. If even half the announced AI infrastructure gets built, uranium demand rises for a decade. The risks are that uranium prices swing hard, mining requires constant spending on equipment and operations, and the company’s earnings rise and fall with the price of what the company digs up.

My plan is to research Energy Fuels further this month. A near-million-dollar CEO buy in a strategic American energy company, during an AI power shortage, fits several of my buying criteria. The swings in uranium prices keep the stock at watchlist rather than buy.

(6) Stocks Beating the Market

Stocks gaining the most momentum and what’s driving them.

1) Penguin Solutions $PENG up +25% on Wednesday 7/8

I’m watching this one, and my rating is 7/10. Penguin Solutions was up +25% on Wednesday after earning Nvidia AI Factory Specialized Partner status. Penguin designs and builds the computing hardware (servers, cooling, and memory systems) that companies need to run AI, and the Nvidia partnership puts Penguin on the short list for businesses building their own AI systems.

The Nvidia partnership is the whole reason for the jump, and it’s a good one. Nvidia controls 97% of the market for the powerful chips that run AI in data centers, so becoming one of its specialized partners is like getting an exclusive contractor license for the biggest construction boom in tech. Companies that can’t build AI systems themselves (which is most of them) will hire partners like Penguin to do the work.

Looking ahead, Penguin’s growth depends on AI spending spreading beyond the biggest tech companies to ordinary businesses, and that wave is still early. The risk is that Penguin is a smaller player competing with Dell and Super Micro for the same customers, and a 25% one-day jump means the stock already reflects a lot of this good news. I’d research the company now and wait for the excitement to cool before buying.

2) Cerebras Systems $CBRS up +9% on Thursday 7/9

I’m watching this one, and my rating is 7.5/10. Cerebras was up +9% on Thursday after announcing a major AI infrastructure expansion across Europe. Cerebras builds AI chips the size of an entire dinner plate (most chips are the size of a postage stamp), a design that makes its systems extremely fast at running AI models. Cerebras is one of the few companies with genuinely different technology than Nvidia rather than a cheaper copy.

The European expansion matters because governments and companies there want AI capacity that doesn’t run through the big American cloud companies (Amazon, Microsoft, and Google), and Cerebras is positioning itself as that alternative supplier. Countries building their own AI systems is becoming one of the biggest spending categories in the industry.

The opportunity is a company taking real market share in running AI models, the fastest-growing part of AI computing. The risk is that Cerebras is competing with Nvidia, the most valuable company on earth, for the same customers. High risk, high potential, worth deep research. Cerebras stays near the top of my watchlist.

3) Cloudflare $NET up +9% on Tuesday 7/7

I’m buying this one, and my rating is 8.5/10. Cloudflare was up +9% on Tuesday after the investment bank Scotiabank upgraded the stock, citing growing confidence in its AI infrastructure business. Cloudflare runs a network that sits between the internet and millions of websites, making them faster and protecting them from attacks. Its servers already sit within milliseconds of most humans on earth, and that network is becoming valuable in a new way. Cloudflare’s network is an ideal place to run AI close to users.

Two things make Cloudflare a rare business. First, the company keeps growing year after year, adding revenue near 30% a year for a decade while constantly launching new products on the same network. Second, Cloudflare has built a new business collecting fees from AI. Websites can now charge AI companies for using their content through Cloudflare, and developers can run AI models directly on Cloudflare’s network. Both markets barely existed two years ago.

Long term, I think Cloudflare becomes one of the essential utilities of the internet, serving every website, app, and AI agent that needs speed and security. The stock is never cheap, and that’s the honest risk. If growth slows even a little, the stock will fall hard. I’m buying anyway, in pieces over time, because a business this durable is worth paying a high price for and holding for a decade.

4) SanDisk $SNDK up +8% on Thursday 7/9

I’m watching this one, and my rating is 7/10. SanDisk was up +8% on Thursday after signing a multi-year agreement to supply memory chips to Meta Platforms. AI data centers need staggering amounts of storage, and a locked-in deal with one of the biggest AI spenders on earth gives SanDisk exactly the predictable revenue that memory companies usually lack.

The problem is the timing. Memory chip stocks like Micron and SK Hynix just fell more than 20% from their peaks as investors bet the boom has peaked, and Michael Burry is betting against Micron, SanDisk’s closest peer. The long-term Meta contract is evidence that the demand is real. The 20% drop across the sector is evidence that prices already assumed that demand.

Memory chips are a boom-and-bust business, and I’ve watched those cycles cost investors money for 20 years. The Meta deal earns SanDisk a watchlist spot, and the falling prices across the sector mean patience will likely get me a better price.

5) MasTec $MTZ up +7% on Wednesday 7/8

I’m watching this one, and my rating is 8/10. MasTec was up +7% on Wednesday after acquiring the electrical contractor Superior Group in a $1.65 billion cash-and-stock deal. MasTec builds the physical infrastructure of modern life (power lines, pipelines, and communications networks), and the Superior deal deepens its electrical construction capacity right as America runs short on exactly that kind of capacity.

MasTec is my favorite kind of AI investment because the company wins even if the AI software companies don’t. Data centers need grid connections, transmission lines, and electricians, and there’s a national shortage of all three. Whoever builds the power infrastructure gets paid no matter which AI company wins.

The growth should last decades, since the US electric grid needs a once-in-a-century rebuild for AI, electric vehicles, and new factories. Construction companies carry project risk, and their profits swing from project to project, which is what keeps MasTec from being a buy today. The stock sits high on my watchlist, and I’d buy if the price falls.

6) AMD $AMD up +7% on Monday 7/6

I’m watching this one, and my rating is 7.5/10. AMD was up +7% on Monday after the investment bank Goldman Sachs raised its price target on stronger AI demand expectations. AMD is the clearest number-two to Nvidia in AI chips, and every big customer (Microsoft, Meta, and OpenAI) wants a backup supplier so Nvidia can’t set prices forever. That backup-supplier role alone guarantees AMD a growing slice of a giant market.

The long-term setup is attractive. Nvidia holds 97% of the market for AI data center chips, and AMD doesn’t need to beat Nvidia to succeed. Moving from 3% market share to 10% of a market this size would transform AMD’s earnings.

The problem is the stock’s price. AMD trades at roughly 73 times its expected earnings for next year, versus 18 times for Nvidia, meaning investors pay four times as much for the challenger as for the champion. After this rise, and with the whole chip sector falling, I want a lower price before buying. AMD stays on the watchlist, with a plan to buy a real drop.

👉 For daily insights, follow me on X /Twitter; Instagram Threads; Facebook; or BlueSky, and turn on notifications!

(7) The Smartest Trade I See Right Now

Unusual options activity shows where big money is placing its bets.

Kenvue $KVUE: Big Money Is Betting This Stock Climbs Past $20

I’m bullish on this trade, and my rating for the stock is 7/10. Unusual options activity showed up in Kenvue $KVUE today, with the stock up $0.43 to $19.61. Someone is making a large, fast bet that this quiet consumer stock keeps climbing, and the details are worth understanding even if you never trade an option in your life.

First, the plain-English definitions. An option is a contract that gives you the right to buy or sell a stock at a set price before a set date. A call option is a bet the stock goes up (it gives you the right to buy at a fixed price, so it gains value when the stock rises above that price). A put option is a bet the stock goes down. Buying a call means paying a small amount today for the chance at a big gain if the stock rises. The strike price is the fixed price written into the contract. When traders buy far more calls than puts, they expect the stock to rise.

Now the numbers. Kenvue traded 12,034 call options today, which is 7 times its average volume and 10 times its put volume. Almost all of it was concentrated in one contract, the July 17, 2026 call with a $20 strike price, where more than 10,400 contracts traded at prices between $0.06 and $0.20 per contract. Open interest (the count of contracts that existed before today) was only 410, which means today’s activity is almost entirely new bets rather than old trades closing out. The largest single orders were on the buy side. Somebody wants the stock above $20 within a week, and they’re betting big.

Here’s what Kenvue actually is. Kenvue owns Tylenol, Band-Aid, Listerine, Neutrogena, and Aveeno. It’s the consumer health business that Johnson & Johnson spun off into its own company, which means it sells products people buy in every economy, recession or boom. The stock is up more than 17% over the past month and trades above its average price from both the past 50 days and the past 200 days, meaning the short-term and long-term price trends both point up. Someone buying a wave of $20 calls expiring in seven days is betting that this climb continues right now, possibly ahead of news.

Why am I bullish on this setup? Three reasons line up. The price trend is up and gaining strength. The flow of money in the market favors it, because investors are moving out of expensive AI stocks and into steady businesses that sell things people buy in any economy, and Kenvue is exactly that kind of business. And the options activity shows conviction, since new buying at 7 times normal volume suggests some investors expect more gains soon. It also fits a bigger idea from this issue. The Wall Street Journal named Johnson & Johnson the company best built for the next 250 years, and Kenvue is the consumer piece of that same legacy, with brands that have survived every crash since your grandparents were kids.

Now the honest risk, because there always is one. These specific calls expire July 17, seven days out, with a $20 strike price. Kenvue has to rise about 2% in one week for the contracts to pay off, and if it doesn’t, they expire worthless and the buyers lose 100% of what they paid. That’s the nature of options that expire soon. They’re cheap because they usually expire worthless. The traders buying them are risking small amounts (6 to 20 cents per share) for a shot at multiplying their money fast. It’s a lottery ticket, and a lottery ticket is never a safe bet, even a smart-looking one.

My advice depends on which kind of investor you are. If you’re a long-term investor, ignore the options and consider the stock itself. Kenvue at $19.61 is a collection of durable brands with demand that holds up in recessions, and my rating is 7/10, a watchlist name I’d research seriously if the price falls back toward $18. If you’re tempted by the options trade itself, only do it with money you can afford to lose completely, keep it under 1% of your portfolio, and decide your exit price before you enter. The stock is a patient investment. The options are a one-week bet.

Part IV: The Financial Playbook (What To Do Now)

8. Practical Tips & Advice

9. The Lesson Most People Learn Too Late

10. You Asked, I Answered

(8) Practical Tips & Advice

Tips to help you make smarter decisions with money, investing, and life.

Keep investing automatically, no matter what the headlines say. Investing the same amount on a schedule (called dollar-cost averaging) removes your emotions from the decision, and the best returns of my investing life came from shares I bought during scary headlines. Set it and leave it.

Favor businesses that win in several futures. Alphabet $GOOGL has search, cloud computing, YouTube, Android, Gemini, Waymo, quantum research, and investments in Anthropic and SpaceX. Several paths to growth means you don’t need one forecast to be right.

Buy the suppliers with real revenue. AI needs chips, memory, optical parts, electricity, cooling, construction, and data centers. Focus on companies with paying customers, low debt, steady profits, and growth beyond one contract.

Separate technology quality from investment quality. A useful product can belong to a weak business. And a strong company can become a poor investment when its stock price assumes years of perfect growth.

Look at energy and uranium. AI data centers need massive amounts of power, and nuclear power is the only proven source that can feed them around the clock. Companies like Energy Fuels $UUUU sit directly in that demand.

In your career, become the person who uses AI to produce measurable results. The layoffs are hitting people whose output cannot be measured. If you can show that AI makes you faster, cheaper, or better, you become harder to replace. The real threat is refusing to learn the tool.

Ask for the raise. Inflation is 4.2% and average wages grew 3.4%. A flat salary in a 4% inflation world is a pay cut you agreed to.

(9) The Lesson Most People Learn Too Late

Financial lessons most people learn too late in life.

Financial lessons most people learn too late in life.

The next 250 years will create companies and industries that we cannot fully imagine today. AI may change knowledge work. Humanoid robots may change physical work. New energy systems may support both. Cellular reprogramming may change how doctors treat the diseases of aging.

Be optimistic about the opportunity. Just don't overpay for the opportunity.

History rewards people who own productive assets for long periods. History also punishes people who assume every promising technology will create a successful company or a profitable investment. The railroads transformed America and still bankrupted a generation of investors who overpaid. The internet changed the world and still erased trillions in 2000. The winners were the businesses that survived long enough to turn useful products into repeat customers and lasting profits, and the investors who paid fair prices for them.

My advice is to own broad American growth through a fund such as VTI or VOO. Add smaller positions in themes you understand. Keep enough cash and short-term Treasury bills to handle emergencies and take advantage of future declines. And invest in your skills with the same discipline, because AI and robots will keep changing jobs, and the people who learn these tools and solve important problems will stay valuable in any economy.

Believe in the future. Just never pay any price for the future.

(10) You Asked, I Answered

What subscribers are asking, and what you need to know too.

Q: Does Berkshire Hathaway’s $397 billion cash balance mean a crash is coming?

No. Berkshire’s cash shows that Buffett has found few large investments that meet his price and quality standards. Treat the cash pile as a lesson in patience and price discipline rather than a prediction. Buffett held record cash before some crashes and before some rallies too.

Q: What is the safest way to invest in humanoid robots?

Use a small position in a diversified robotics fund such as KOID, BOTZ, or ROBO, then review what the fund actually owns. Many robotics funds also hold industrial automation, chips, software, and medical equipment, so know what you’re buying before you buy.

Q: Which public companies could benefit from humanoid robots?

Nvidia $NVDA, AMD $AMD, Broadcom $AVGO, Qualcomm $QCOM, Rockwell Automation $ROK, and Teradyne $TER supply parts, computing, or automation systems. Each company has different risks, and only part of each business is tied to humanoid robots.

Q: What are Trump Accounts and should my kid have one?

Trump Accounts launched July 4. Any child under 18 can get one, contributions cap at $5,000 per year, the money goes into a long-term index fund automatically, and babies born 2025-2028 get $1,000 from the federal government. Free government money invested for decades is worth taking. Opening an account costs nothing.

👋Final Words:

Thanks for reading and joining 113,000 subscribers who trust our newsletter to get smarter with money. I spent 20 years in finance so you don’t have to. My goal is simple: to help you build wealth, make better decisions, and protect your future by breaking everything down in plain English.

Please support us and:

Hit the LIKE button on this post

Share this newsletter on social media or with friends & family:

Become a paid subscriber and get smarter with your money (learn about the benefits here) (get a free 30-day trial with this link):

Want more of our insights in your Google Searches and AI answers?

Choose TheFinanceNewsletter.com as a preferred news source. You’ll see our content more often in your results.

And please let us know how we did on today’s newsletter:

Missed an issue? Read past issues here at TheFinanceNewsletter.com

☺️ My goal is to help you become richer and smarter with money — Join 3+ million and follow me across social media for daily insights:

Instagram Threads: @Fluent.In.Finance

Twitter/ X: @FluentInFinance

Facebook Page: Facebook.com/FluentInFinance

Linkedin: Linkedin.com/in/Lokenauth

Youtube: Youtube.com/FluentInFinance

Instagram: @Fluent.In.Finance

TikTok: @FluentInFinance

Reddit Community: r/FluentInFinance

➕Please add this newsletter to your contacts to ensure that none of our emails ever go to spam!

This content is for educational purposes only. Such information should not be construed as legal, tax, investment, financial, or other advice. See for Disclaimer, Terms and Conditions.