💥 What Hantavirus, The Bond Crisis, And 3.8% Inflation Tells Us (And What's Next)

EXPLAINED: Stock Market Is Up But Americans Feel Worse Than EVER. Consumer Sentiment Hit 74-Year Low. And The Bond Crisis Nobody Is Talking About.

Warren Buffett once said something that took me years to fully appreciate. He said the stock market is a voting machine in the short run but a weighing machine in the long run. Right now, the votes are overwhelmingly bullish. But when you put the economy on the scale, what you find is a lot heavier and a lot darker than the headlines suggest.

Here’s the contradiction you need to sit with this week. The S&P 500 just hit an all-time high. Consumer sentiment just hit an all-time low. At the same time. In the same country. For the same people.

The University of Michigan’s Consumer Sentiment Index, a survey that’s been running for 74 years, just posted its worst reading in recorded history. Worse than the 2008 financial crisis. Worse than COVID. Worse than the double-digit inflation of the 1970s. And yet your brokerage account has never looked better, as long as you own the right five tech stocks.

I’ve spent over 20 years working in banking and finance, and I’ve never seen a gap this wide between how Americans feel and what the market says. This week, I’m going to show you exactly why that gap exists, how long it can last, and what you should do before it closes.

Because it will close. It always does.

Here’s what’s happening beneath the surface. Gas just crossed $4.50 a gallon nationwide, a 50% jump since the Iran war started. Real wages just went negative for the first time in three years. Consumer debt, both credit cards and auto loans, just hit all-time highs. The spring housing market just posted its worst performance in years. And Jamie Dimon, the most powerful banker on the planet, just warned publicly that a bond crisis is coming.

And yet the market is at record highs.

This week’s newsletter is about understanding both worlds at once. The world your portfolio sees and the world your paycheck feels. Once you understand both, you’ll know exactly where to put your money and, just as importantly, where to pull it out.

This week, we break down why stocks are hitting records while consumers are cracking, why the bond market may be the real danger, and how energy shocks, AI, and solar could shape the next decade of investing.

📬 In today’s newsletter, we look at:

Part I - Market & Economy Update:

1. Analysis & Outlook

2. Important Finance NewsPart II - Investing Research:

3. Insider Trading

4. Top Stocks Right Now

5. Today’s Trade

6. Market Sentiment (Fear & Greed Analysis)

7. Macro Technical AnalysisPart III - Tips & Advice:

8. Advice, Lessons & Recommendations

9. Final Thoughts

10. Your Top Questions Answered

Hope you’re enjoying this newsletter — it takes a week to research and write so please help support our journalism and:

Hit the LIKE button❤️ on this post and share this newsletter on social media (or with friends & family):

🙏Become a paid subscriber! (learn about the benefits here) (Get a free 30-day trial with this link):

Part I - Markets & Economy Update

(1) Analysis & Outlook

📈 Everything You Need to Know (in 1 minute):

Inflation hit 3.8% in April, the highest in three years, beating the Wall Street forecast of 3.7%. Gas prices are up 50% since the Iran war started, and they drove most of the jump.

Real wages fell 0.2% year-over-year, the first drop since 2023. Workers got a 3.6% pay raise on paper, but inflation wiped it out completely. Paychecks are shrinking in real terms.

Consumer debt hit record territory. Auto loan and credit card delinquencies are at all-time highs. Total auto debt crossed $1.68T and credit card debt hit $1.33T.

Consumer sentiment hit a record low at 48.2 on the University of Michigan index, yet the S&P 500 is at all-time highs. The gap between Main Street and Wall Street has never been wider.

The spring housing market stalled. Sales rose just 0.2% in April versus an expected 3% jump. The national median home price hit a record $417,700 while mortgage rates climbed back above 6%.

Bond yields are climbing fast. The 10-year Treasury yield reached 4.45%, markets are pricing in zero rate cuts until late 2027, and there’s a 42% chance of a rate hike by early 2027.

Copper prices hit a record $6.41 per pound, up 40% year-over-year, driven by the AI data center building boom.

Tech and AI stocks are carrying the market. The S&P 500 hit record highs, but only because a handful of big tech names are carrying the weight. Equal-weighted returns are running at about half the headline number.

Semiconductors are on a historic run. Intel is up 239% year-to-date and Sandisk is up 558% year-to-date. The PHLX Semiconductor Index is up 55%+ from its March lows.

The Iran war is accelerating clean energy adoption. Over $3B flowed into renewable energy ETFs in April alone, the biggest monthly inflow since early 2021.

💡 Andrew’s Analysis & Advice:

Most people think a rising stock market means a healthy economy. Right now, that idea isn’t true.

Here’s what’s actually happening. We have two very different Americas sitting side by side. In one America, tech stocks are breaking records, AI spending is exploding, and chip companies are putting up some of the best single-year returns in stock market history. In the other America, gas is $4.50 a gallon and climbing, real wages just went negative for the first time in three years, and consumers are drowning in record debt.

This is the K-shaped economy at its most extreme. And if you’re not watching both sides of that “K,” you’re missing the full picture.

The Iran war is the thread connecting all of it.

When the Strait of Hormuz closed, it didn’t just spike oil prices. It set off a chain reaction. Higher oil meant higher gas. Higher gas meant higher inflation. Higher inflation meant the Fed couldn’t cut rates. No rate cuts meant higher mortgage rates. Higher mortgage rates froze the housing market. A frozen housing market hurt consumer confidence. And crushed confidence threatens to slow spending, the engine of roughly 70% of the US economy.

During my 20 years working in banking and finance, I watched how fast one shock could ripple through an entire economy. This is one of those moments. The energy shock has become an inflation shock, which has become a consumer shock, which now threatens to become a growth shock. The chain isn’t done yet.

Here’s the number to watch above everything else. The 10-year Treasury yield is now at 4.45%. That stat isn’t just a bond market number. It drives mortgage rates, auto loans, credit card rates, and the cost of borrowing for every business in America. The last time yields pushed to this level, it triggered the tariff pause. Markets are fragile at these levels. And the bond market tends to know before the stock market does. When bonds are stressed, stocks eventually follow.

But here’s what makes this moment so unusual. The stock market isn’t listening, at least not yet. The S&P 500 is at record highs. The Nasdaq is up nearly 17% over the past month. Why? Because AI is doing something extraordinary.

The AI supercycle is real, and it’s not hype. Chip stocks like Intel (up 239% this year) and Sandisk (up 558% this year) aren’t just riding narrative. They’re riding real revenue and real profit growth. This is not the dot-com bubble, where companies had no earnings. Micron is on pace for $77 billion in operating profit this year. Samsung just reported an 8x jump in quarterly operating profits. These are real numbers tied to real demand.

But here’s the risk that most people aren’t talking about. When one sector carries an entire index, the whole market becomes dependent on that sector continuing to deliver. Two things could derail this rally quickly. First, any sign that Big Tech is slowing its data center spending. Second, any escalation in the Iran conflict that pushes oil toward $110 or $120 per barrel and drives bond yields to dangerous new levels.

Here’s the bigger-picture connection most people are missing. Copper prices just hit a record high at $6.41 per pound, up 40% from a year ago. That’s not random. You can’t build a data center without copper wiring. The AI buildout is so massive it’s driving real commodity demand at scale, which adds to inflation pressure, which keeps the Fed from cutting, which keeps mortgage rates high, which keeps the housing market frozen. Everything is connected.

Now think about this differently. The very same war that’s crushing American consumers is also speeding up the clean energy transition. Over $3 billion flowed into renewable ETFs in April alone. South Korea doubled domestic EV sales in a single month. EU leaders are getting “more aggressive” on electrification. The energy shock is forcing every country to rethink oil dependence, and that rethinking could reshape global investment for the next decade. The Iran war may ultimately be remembered as the accelerant that pushed the world off oil faster than any climate policy ever could.

What this means for you:

First, don’t confuse a rising market with a safe market. A narrow, tech-driven rally is fragile. When five stocks do most of the heavy lifting for an entire index, there’s not a lot of cushion if one of them stumbles.

Second, watch the 10-year Treasury yield. If it pushes toward 5%, expect real pressure on rate-sensitive sectors like real estate, utilities, and consumer discretionary.

Third, clean energy exposure belongs in almost every long-term portfolio. The question isn’t whether solar and storage win the energy race. It’s how fast. The $3B+ flowing into renewable ETFs in a single month is the market telling you something.

Fourth, if you’re a worker, the math is brutal right now. With real wages negative and inflation above 3.5%, you’re losing ground every month you stay at your current pay level. Negotiating a raise or switching jobs isn’t optional advice right now. It’s survival.

The story of this market isn’t just about AI stocks hitting record highs. It’s about two worlds pulling in opposite directions. The question isn’t which one wins. The question is how long they can stay apart before they collide.

👉 To get smarter with money follow me on X /Twitter; Instagram Threads; Facebook; or BlueSky (and turn on notifications)

(2) Important Finance News

📬 Today we look at:

1) What Hantavirus Means for Investors

2) How Can Stocks Be at All-Time Highs When Americans Feel Worse Than Ever?

3) Why the Bond Market Is the Most Dangerous Place in the World Right Now

4) The Best Cities for New Graduates in 2026

5) The Energy Revolution Nobody Is Talking About

🤔 But first, what do you think?

1. What Hantavirus Means for Investors

What was supposed to be a dream vacation turned into something far darker for the roughly 150 passengers aboard the MV Hondius, a Dutch cruise ship. The World Health Organization confirmed a deadly hantavirus outbreak on the vessel with three passengers dead and at least eight cases confirmed. Authorities across more than a dozen countries are now tracking down passengers who disembarked before the outbreak was identified.

The strain confirmed on the ship is the Andes variant, the only known type of hantavirus capable of spreading from person to person through close physical contact or shared utensils. Flu-like symptoms can appear anywhere from one to eight weeks after exposure, and there’s currently no approved vaccine or targeted treatment. Health authorities from South America to Europe are evacuating and quarantining passengers on government aircraft, and the Hondius is being diverted to the Canary Islands.

Health experts are moving fast to calm concerns. WHO Director-General Tedros Adhanom Ghebreyesus stated clearly that hantavirus is “not another COVID” and stressed the low overall public health risk, noting that person-to-person transmission remains rare even with the Andes strain.

The financial fallout, however, is already real. Royal Caribbean fell over 2%, Carnival dropped over 2%, Norwegian Cruise Line dipped under 1%, and Viking Holdings fell nearly 2%. The cruise industry is already fighting surging fuel costs and weaker bookings tied to the Iran war, so a deadly disease outbreak during peak summer booking season is about the worst timing possible. Norwegian recently warned that “softer travel demand and geopolitical uncertainty are weighing on bookings,” and that was before this headline hit.

On the flip side, Moderna shot up nearly 12% on day one and another 12% the following day after confirming it has been conducting early-stage hantavirus vaccine research. Analysts at Evercore pushed back, calling the move “sentiment-driven rather than fundamental” and noting that hantavirus represents a “structurally small market” with low incidence rates. Other pharma names like Inovio and Novavax also spiked, despite having no active hantavirus programs.

What this means long-term: This outbreak reveals something important about investor psychology four years after COVID. The “pandemic fear trade” has become a replicable playbook. When an outbreak headline hits, biotech names with any connection to the disease surge, and travel stocks sell off, regardless of whether the fundamental risk is high or low. Knowing this pattern gives you an edge. The next outbreak, whenever it comes, will follow the same script.

The deeper issue for cruise stocks isn’t one virus. It’s that the sector is getting hit from multiple directions simultaneously: high fuel prices, geopolitical uncertainty reducing international travel demand, and now disease headlines during peak booking season. These stocks deserve caution, not blind averaging down.

My advice: If you own cruise stocks, review your position sizing against a backdrop of sustained multiple headwinds. For pharma, never buy a biotech stock purely on outbreak headlines without confirming that the company has an actual product in development at a meaningful clinical stage. Sentiment trades on outbreak news are fast-moving and sharp in both directions.

2. How Can Stocks Be at All-Time Highs When Americans Feel Worse Than Ever?

The University of Michigan’s Consumer Sentiment Index just posted its second consecutive all-time low, hitting 48.2 in May, down from 49.8 in April. This is the worst reading in the survey’s 74-year history, worse than COVID-19, worse than the 2008 financial crisis, worse than any prior moment of economic upheaval captured in the data.

And yet the S&P 500 is at an all-time high.

The preliminary May reading cut across all income levels, age groups, education levels, and political affiliations. About a third of survey respondents pointed to gas prices. About 30% mentioned tariffs. What’s driving the anxiety isn’t hard to identify. Gas is above $4.50 nationally, inflation just hit its fastest pace in three years, job growth is “near zero” per Fed Chair Jerome Powell, and large-scale layoffs from companies like Oracle, Citigroup, and UPS have dominated headlines.

Corporate earnings this week put ground-level detail on those numbers. McDonald’s CEO Chris Kempczinski called the environment “challenging” and said consumer conditions may be “getting a little bit worse,” pointing to high gas prices squeezing lower-income households. Whirlpool reported a greater-than-expected quarterly loss and said the company experienced “recession-level industry decline” in the US as consumer confidence collapsed in late Q1. Maersk, one of the world’s largest shipping companies, said $100 per barrel oil is costing them roughly $500 million per month and that some of those costs are flowing to consumers. From fast food to home appliances to global freight, the message is the same. The American consumer is under serious pressure from multiple directions at once.

And yet stocks are at records.

During my time on Wall Street, I saw this kind of divergence before. Housing data was flashing red for months before the 2008 stock market caught on. The market has a historical habit of ignoring bad news until it absolutely can’t anymore. The gap between how Americans feel and what their portfolios show has never been wider. But gaps like this don’t last forever.

What this means long-term: Consumer spending accounts for roughly 70% of US GDP. When consumers pull back meaningfully, corporate revenue falls. When revenue falls, earnings follow. When earnings fall, stocks follow. The lag between sentiment and stock prices can stretch for months or even longer. But they always reconnect. The question isn’t whether this divergence closes. It’s when and how hard.

My advice: Consumer discretionary stocks, companies that sell things people want but don’t need, are the most exposed sector right now. Companies with exposure to lower-income consumers face the biggest direct headwind. Companies that serve higher-income consumers or sell essential goods and services are far better positioned. Look at your portfolio and honestly ask how much discretionary consumer exposure you’re carrying into what could be a significant spending slowdown.

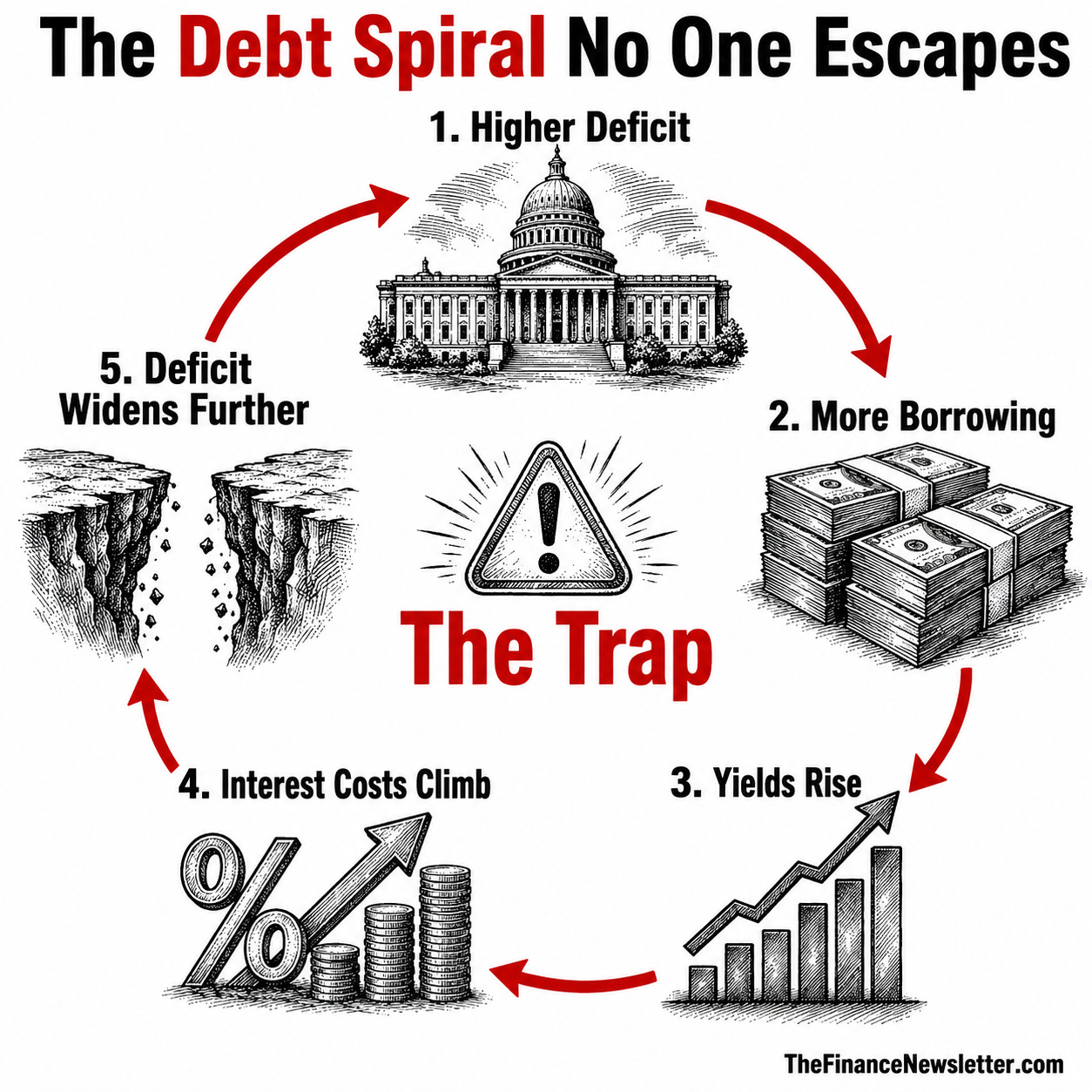

3. Why the Bond Market Is the Most Dangerous Place in the World Right Now

JPMorgan Chase CEO Jamie Dimon, speaking at a Norges Bank Investment Management conference in Oslo, warned that the world is heading for “some kind of bond crisis” unless governments address their surging debt levels. The Wall Street Journal reported that Dimon said he doesn’t understand “how the world running deficits like this isn’t inflationary” and acknowledged the damage may already be done.

The numbers behind the warning are staggering. The US government has spent $1.17T more than it has collected in fiscal 2026 alone, a fiscal year that only started in October. That deficit is running at a pace that would be alarming in a recession. We’re not in a recession. We’re doing this in a period of full employment. And every dollar of deficit spending adds to a debt load that markets are increasingly nervous about financing at current yields.

Here’s why the timing is so critical. The 10-year Treasury yield is now at 4.45% and climbing. Iranian drone strikes on UAE energy infrastructure are pushing yields higher. Markets are now pricing in zero rate cuts until late 2027 and a 42% chance of a rate hike by early 2027. If the 10-year pushes toward 5%, we’re looking at 7%+ mortgage rates and structural damage to the housing market that could last years.

The feedback loop Dimon is warning about is dangerous and well-established in economic history. Higher deficits fuel more government borrowing. More borrowing pushes yields higher. Higher yields increase the government’s interest expense, which widens the deficit further. A wider deficit requires even more borrowing. And on it goes until the market forces a reckoning, usually through a rapid spike in yields or a credit-rating downgrade.

I’ve been saying for months that the bond market is the metric to watch above all others in 2026. If you took that seriously, none of this week’s data surprised you.

What this means long-term: A bond crisis isn’t just a government balance sheet problem. It would hit every American household. It would push up the cost of mortgages, car loans, credit cards, and business borrowing. At its most extreme, a bond crisis can trigger a currency crisis, which historically leads to severe recessions and decades of reduced living standards. The countries that have experienced them, Argentina, Greece, Turkey, never fully recover their prior trajectory.

My advice: Position your portfolio for a “higher for longer” interest rate environment. That means favoring shorter-duration bonds over long-duration bonds, which get hit hardest by rising yields. Reduce exposure to dividend stocks that compete directly with bonds for income-seeking investors. Consider Treasury Inflation-Protected Securities as an inflation hedge. And if you carry variable-rate debt of any kind, lock in fixed rates wherever possible before the next potential hike. The time to prepare for a bond crisis is before it arrives, not after.