💥 Layoffs, War, Stagflation, and What Happens Next

Recession Risk Is Rising Fast. The Worst Job Market in 15 Years. GAS AT $10? (And What to Do Now)

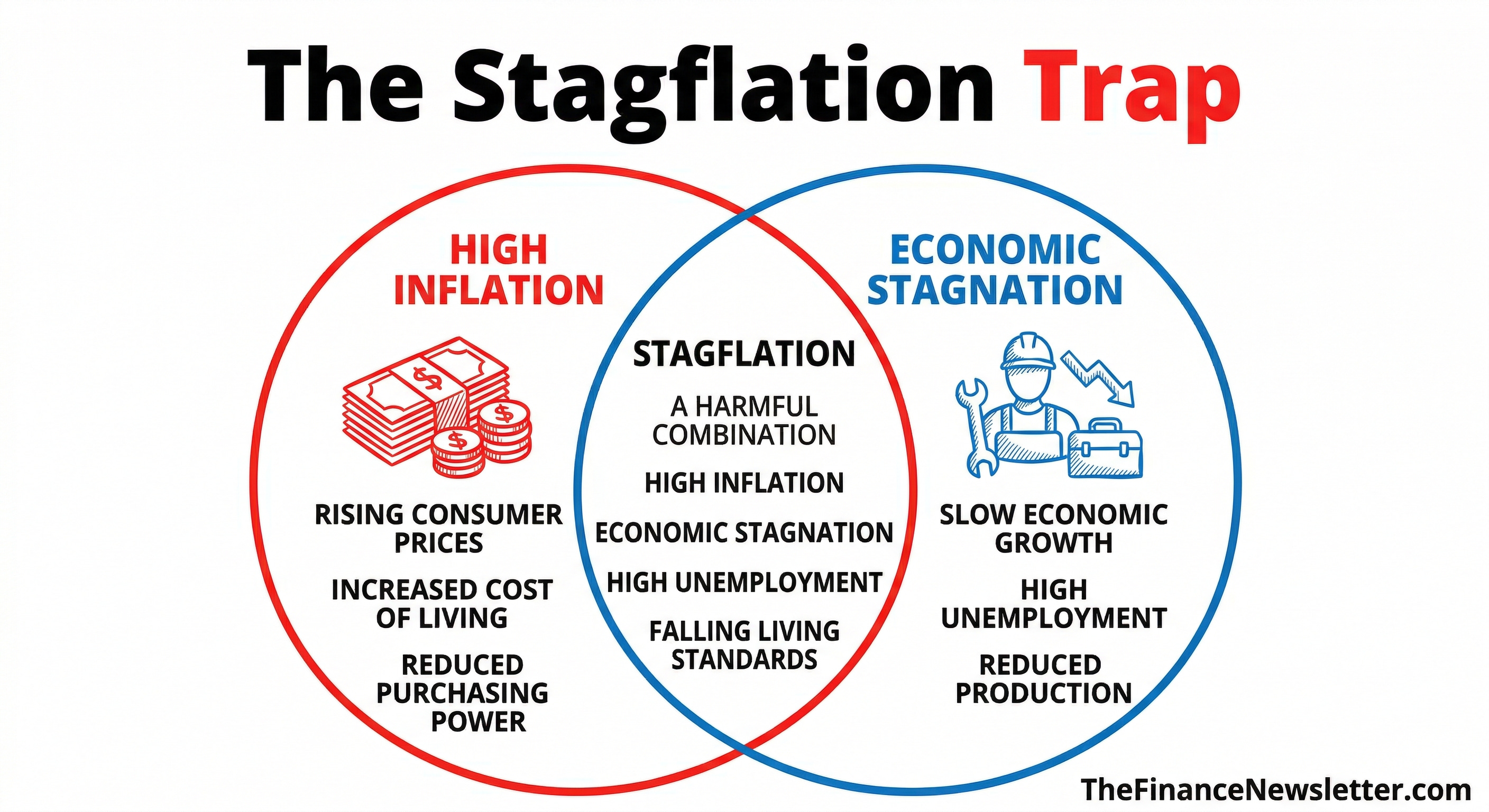

In 1973, OPEC cut oil exports to the United States. Gas lines stretched for blocks. Prices doubled. The stock market dropped 45%. Stagflation — rising prices and stagnant growth — gripped the economy for the better part of a decade.

Most investors alive today have never lived through a real stagflation cycle. They’ve read about it. They’ve studied it. But they’ve never felt it.

They’re about to.

The Iran war started in late February. Oil has jumped 40% since. Gas crossed $4 a gallon. Inflation is headed to 4.2% — the highest in the G7. The hiring rate just hit its lowest point in 15 years. And the Fed — stuck between fighting inflation and protecting growth — may be about to raise rates for the first time in years.

Your grocery bill is about to get worse. So is your gas tank. And your mortgage. And your job security.

I warned you about this three weeks ago.

If you're scared, you're not alone. The data says almost everyone is.

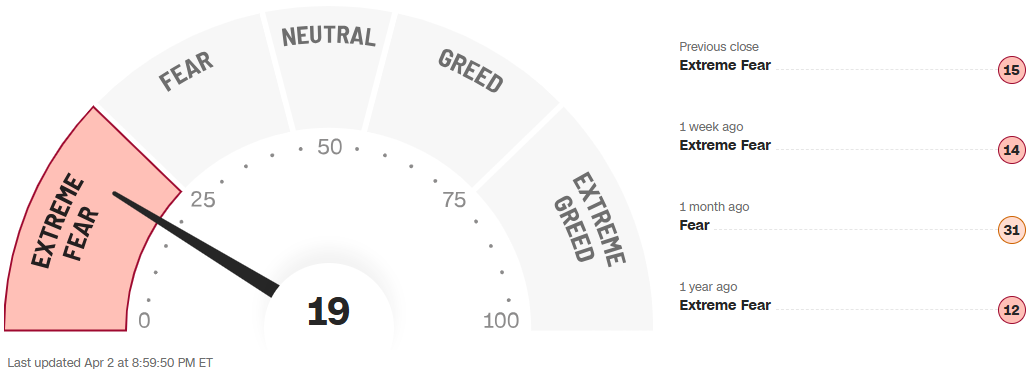

Right now, the Fear and Greed Index sits at 19. Extreme Fear.

The S&P 500 just posted five straight weeks of losses. Oil is above $111. Recession odds are approaching 50%. The Mag 7 — Apple, Microsoft, Nvidia, Meta, Alphabet, Amazon, Tesla — just had their worst quarter in years.

Nothing feels fine right now.

This is the part of the cycle where people make emotional decisions and call them rational.

Do not do that.

This isn’t just a bad quarter. It’s a regime change. It is a repricing of the world around higher energy costs, weaker hiring, tighter money, and rising geopolitical risk. And the investors who understand that early will have an edge that most people will not.

And those who understand what’s happening — and act on it — will be in a very different financial position one year from now than the ones who wait for the news to get better.

This newsletter isn't about fear. It's about clarity. This issue breaks down exactly what's happening, why it matters, and — most importantly — what you should do about it right now.

I cover why the US economy may be entering its first real stagflation cycle in decades, what a 19 Fear and Greed reading means for you, which sectors win and which lose in this environment, and the exact moves that give you the best shot at building wealth.

📬 In today’s issue:

Part I - Markets & Economy:

1. Update, Analysis, and Outlook

2. Important Financial News

3. Chart of the Day [Deep Dive]Part II - Investing Research:

4. Insider Trades

5. Top Stocks Right Now

6. Today’s Trade

7. Fear & Greed Analysis (Market Sentiment)

8. Macro Technical Analysis & PredictionsPart III - My Tips & Advice:

9. Actionable Advice & Recommendations

10. Final Thoughts & Lessons

11. Your Questions Answered

This newsletter takes a week to research & write so please help me and:

Hit the LIKE button❤️ on this post and share this newsletter with friends and family:

🙏Become a paid subscriber and get smarter with your money! (learn about the benefits here) (Get a free 30-day trial with this link):

Part I - Markets & Economy

(1) Update, Analysis, and Outlook

📈 Everything You Need to Know (in 1 minute):

The S&P 500 fell for a fifth straight week — its longest losing streak since 2022 — closing Q1 2026 as the worst quarter since Q2 2022. The Nasdaq fell ~7%, the S&P 500 fell ~5%, and the Dow fell ~4% for the quarter.

The hiring rate fell to 3.1% in February — the lowest since April 2020. Job openings dropped to 6.9 million. US companies announced 60,620 layoffs in March, up 25% from February, with employers mostly blaming AI.

The OECD raised US inflation to 4.2% for 2026 — the highest in the G7. Global growth is projected to slow from 3.3% in 2025 to 2.9% in 2026.

Iran rejected all US ceasefire terms and set five conditions, including international recognition of its authority over the Strait of Hormuz.

Oil surged past $111/barrel on Thursday after Trump’s speech signaled weeks more of Iran conflict, marking an 11%+ single-day jump — oil’s biggest single-day spike since April 2020. Oil is now up ~40% since the war began in late February.

Gas hit $4.08/gallon nationally this week — the first time since August 2022. That’s a ~35% spike in a single month.

The Dow entered correction territory (down ~10% from its February ATH). The Nasdaq is down ~13% from its October peak. The MSCI All Country World Index dropped 9% this month alone.

Mag 7 tech stocks are down ~8% as a group since October. Microsoft had its worst Q1 since the 2008 financial crisis (down 25%). Meta is down 29%. Nvidia is down nearly 20%.

Visa, Mastercard, and Amex each fell ~20% in synchronized selling pressure. Eli Lilly shed 17% on pharma tariff concerns.

Europe is breaking away from Visa, Mastercard, and US financial infrastructure, fast-tracking a Digital Euro and building alternatives to Microsoft Office.

Iran struck two major aluminum producers over the weekend — Emirates Global Aluminium and Aluminium Bahrain — sending aluminum to a 4-year high. Alcoa soared 8% and Century Aluminum jumped 7%.

Helium prices doubled in a month as Qatar’s LNG exports halted through the Strait. Helium cools AI chip-making equipment. South Korea’s Samsung and SK Hynix are running critically low on reserves.

Recession odds are rising fast. Goldman Sachs put them at 30%. EY Parthenon at 40%. Wilmington Trust at 45%. Moody’s Analytics at 48.6%.

Mortgage rates climbed to 6.62%, up from 5.99% in February, pushing homeownership further out of reach.

SpaceX filed confidentially for an IPO targeting a $1.75 trillion valuation — potentially the largest public offering in history, raising up to $80 billion.

💡 Andrew’s Analysis & Advice:

This isn’t just a bad week. This is a regime change.

After 20+ years in finance, I’ve seen corrections, crashes, panics, and recoveries. And I’ll tell you this: the most dangerous market moments aren’t the ones that feel catastrophic. They’re the ones that feel slow. Uncertain. Dragged out. This is one of those moments.

The War Is Rewriting Every Assumption

When the US and Israel launched strikes on Iran in late February, Wall Street analysts told you not to worry. “Geopolitical shocks are short-lived,” they said. That was over a month ago. Today, oil sits above $111/barrel. Gas crossed $4/gallon for the first time since 2022. And Tuesday’s brief market rally on peace talk rumors got crushed the very next day when Trump’s prime-time address Wednesday night made clear there’s no clean exit in sight.

The Strait of Hormuz is the world’s energy chokepoint. About 20% of global oil and LNG flows through it. It’s been closed since the war started. And that single fact is rippling through every corner of the global economy — like a slow shockwave.

Here’s what most people don’t appreciate: the shockwave moves from east to west. JPMorgan’s head of global commodities research compared this to COVID-19, unfolding sequentially. Oil tankers from the Persian Gulf reach Asia in 10-20 days. Europe hits the wall in 20-35 days. The US is last in line, 35-45 days away. Asia is already rationing fuel and canceling flights. Europe hits full impact by mid-April. The US hasn’t felt the full force yet.

Tech’s Slide Is About More Than the War

Let’s be honest, tech was already expensive before a single bomb dropped on Tehran. Near-record valuations. Soaring AI spending. A market questioning whether that spending would ever translate into proportional profits. Then the war started. Oil above $110/barrel means the biggest tech companies, set to spend over $650 billion this year on energy-hungry data centers, suddenly face a major cost problem. Microsoft is down 25% for the quarter (its worst since 2008). Meta is down 29%. Nvidia is down nearly 20% from its October peak.

But here’s what the crowd is getting wrong, this doesn’t mean tech is dead. It means tech was overpriced and is now getting repriced. That’s actually healthy. And as the Chart of the Day shows this week, the Mag 7’s P/E premium versus the rest of the S&P 500 has collapsed from 100%+ at its peak to just 30% — a 10-year low. Great companies getting cheap isn’t a tragedy. It’s an opportunity — for those patient enough to wait for the right moment.

The “Buy the Dip” Reflex Just Got Burned

For three years, investors were trained like Pavlov’s dogs: market dips, you buy, you win. That reflex is getting punished now. This selloff is more drawn out and less dramatic than the quick crashes investors have grown accustomed to. Kevin Gordon at Charles Schwab captured it well this week: “Ironically, that’s keeping people from feeling they can buy the dip.”

And that hesitation is costing money. The investors who wait for certainty always arrive too late.

But the uncomfortable truth is this: more pain could still be ahead. Iran rejected all US ceasefire terms this week. Société Générale’s Michael Haigh warns that if the disruption lasts a few more weeks, global oil inventories could fall to historic lows — and Brent crude could hit $200/barrel. At $200 oil, we’re not talking recession risk. We’re talking recession certainty.

The Hidden Casualties: Aluminum and Helium

Oil isn’t the only commodity in crisis. Iran’s attacks on Emirates Global Aluminium in Abu Dhabi and Aluminium Bahrain over the weekend knocked out two of the Middle East’s largest producers. Aluminum surged to a 4-year high — up 12% in its biggest monthly gain in eight years. Aluminum goes into cars, homes, packaging, and electronics. Higher aluminum costs feed into inflation in places you’d never expect.

Then there’s helium — the story almost nobody is talking about. Qatar supplies roughly a third of the world’s helium. Helium is the critical coolant for AI chip manufacturing. With Qatar’s LNG exports halted, helium prices have doubled in a month. South Korea (home to Samsung and SK Hynix, the world’s two largest memory chipmakers) is running low, with reserves potentially drying up by June. If helium runs out, AI chip production slows, AI hardware gets scarce, and every AI valuation story gets repriced downward. Pull one thread. The whole sweater unravels.

The Consumer Squeeze Is Just Getting Started

Gas at $4.08/gallon isn’t just an inconvenience. JPMorgan calculates that if gas stays near $4 through year-end, it will drain roughly $100 billion from consumer purchasing power. That money comes from somewhere. Either you cut spending elsewhere, or you dip into savings. Both outcomes are bad for the economy.

Diesel is even worse — up 44% since the war began, now at $5.42/gallon. That hits truckers. Truckers hit retailers. Retailers hit you. The inflation you feel at the grocery store in May started with a tanker that couldn’t get through the Strait of Hormuz today.

The OECD raised its US inflation forecast to 4.2% this week. The USDA projects food prices to rise 3.6% this year. Beef, fish, vegetables, and baked goods are all headed higher. Fertilizer, which largely ships through the Strait of Hormuz, is getting scarce, threatening crop costs for months ahead. The squeeze is real, and it’s barely getting started.

The Hiring Reality Check

The job market served up its worst reading in 15 years — and this data was collected before the Iran war had time to fully filter through. The hiring rate dropped to 3.1% in February, the lowest since April 2020. Job openings fell to 6.9 million. Layoffs jumped 25% in March. Powell told Harvard students this week: “There’s no denying that it’s a challenging time to enter the labor market.”

This is stagflation’s defining characteristic: a weak labor market that the Fed can’t rescue with rate cuts because inflation is running too hot. The two standard tools work against each other. That’s what makes this era genuinely difficult.

Europe’s Quiet Breakup With US Financial Infrastructure

One underreported story this week: Europe is accelerating its break from US payment networks and financial systems. What was a deliberate 2030 target for the Digital Euro is now moving faster. As of February, 130 million users across 13 European national payment systems are already linked in a cross-border network charging fees far below Visa and Mastercard. Europe is also building its own alternative to Microsoft Office. This is long-term structural pressure on US payment giants whose international transaction revenue depends on a fragmented, US-centric global financial system.

The SpaceX IPO

Amid all the gloom, one story stands apart. SpaceX filed confidentially for an IPO targeting a $1.75 trillion valuation and up to $80 billion in capital — the largest public offering in history if it hits those numbers. Saudi Aramco’s record 2019 IPO raised $29 billion. Last year, the entire US IPO market raised $44 billion from 202 companies combined. SpaceX wants to beat both.

Up to 30% of IPO shares may be reserved for individual investors — triple the typical allocation. If you’ve ever wanted to own a piece of the space economy before it fully takes off, the June listing window could be your moment.

My advice:

Defense (protect wealth now):

Own energy. The only S&P 500 sector up in 2026 — up 39% this quarter. Oil stocks, LNG players, and natural gas companies are the direct beneficiaries.

Rotate into defensives. Utilities, consumer staples, and healthcare hold up in stagflationary environments. Not exciting — but they protect what you’ve built.

Pay down variable-rate debt now. With a 52% chance of a rate hike by year-end (futures markets this week), every floating-rate obligation gets more expensive. Act before the Fed does.

Offense (position for the recovery):

Build your Mag 7 watchlist. The P/E premium is at a 10-year low. Dollar-cost average in — don’t try to time the exact bottom.

Stay selective, not heroic. Do not buy everything just because prices are down. Buy only what you would be happy to own for years.

Watch the ceasefire signals. Any credible peace move sends oil lower and stocks sharply higher. Have your shopping list ready. Speed will matter.

👉 To get smarter with money follow me on X /Twitter; Instagram Threads; Facebook; or BlueSky (and turn on notifications)

(2) Important Financial News

📬 Today we analyze the impacts of:

1) Trump's $2.2 Trillion Budget

2) The Uncertainty Loop Paralyzing Our Economy

3) The Only Two Catalysts Moving Stocks

4) Winners and Losers From the Iran War

5) America’s Inflation Problem Just Got Worse

6) The Fed Might Raise Rates for the First Time in Years

7) The Job Market Is the Worst It's Been in 15 Years

🤔 But first, the Iran war has been running for over a month now, how long do you think it will last?

1. Trump’s $2.2 Trillion Budget

The White House released its proposed 2027 federal budget this week, and the numbers are historic. The proposal calls for $1.5 trillion in total defense spending — a 42% jump from current levels and the largest single-year increase in military spending since World War II. The full budget totals $2.2 trillion, with $1.1 trillion for the Pentagon and another $350 billion for munitions stockpiling and defense industrial expansion.

To fund the buildup, non-defense discretionary spending gets cut by 10%, roughly $73 billion. The hits are deep and broad. The Small Business Administration loses 67% of its funding. The EPA drops 52%. NASA is cut 23%. Public schools lose $8.5 billion. Affordable housing construction grants ($1.3 billion) get eliminated entirely. Job training for at-risk youth, broadband access programs, community disaster preparedness grants, scientific research funding, rural small business loans — all on the chopping block.

Important context: This is a proposal, not law. Congress controls the budget, and lawmakers have historically rejected Trump’s deepest domestic cuts while approving military increases. Think of it as a window into White House priorities — not a confirmed roadmap.

Why this matters long-term: The US already carries $39 trillion in federal debt. This budget assumes 3.5% GDP growth this year — the Congressional Budget Office projects under 2%. It also assumes 10-year Treasury yields fall to 3.5% by 2027. They sit at 4.35% today. If those assumptions miss, the fiscal math collapses and the debt load grows heavier.

The signal is clear regardless of what Congress passes. Defense spending is going up. We haven’t seen military buildup on this scale since WWII. Companies that supply the military — weapons systems, munitions, ships, missile defense, cybersecurity — are in a multi-year structural tailwind. Cuts to clean energy, education, broadband, and science funding, meanwhile, are long-term headwinds for those sectors.

My advice: Defense contractors like Lockheed Martin $LMT, RTX $RTX, Northrop Grumman $NOC, and General Dynamics $GD build the exact weapons systems, missiles, and ships this budget prioritizes. During the post-9/11 defense buildup, these stocks were among the decade’s top performers. History may be rhyming.

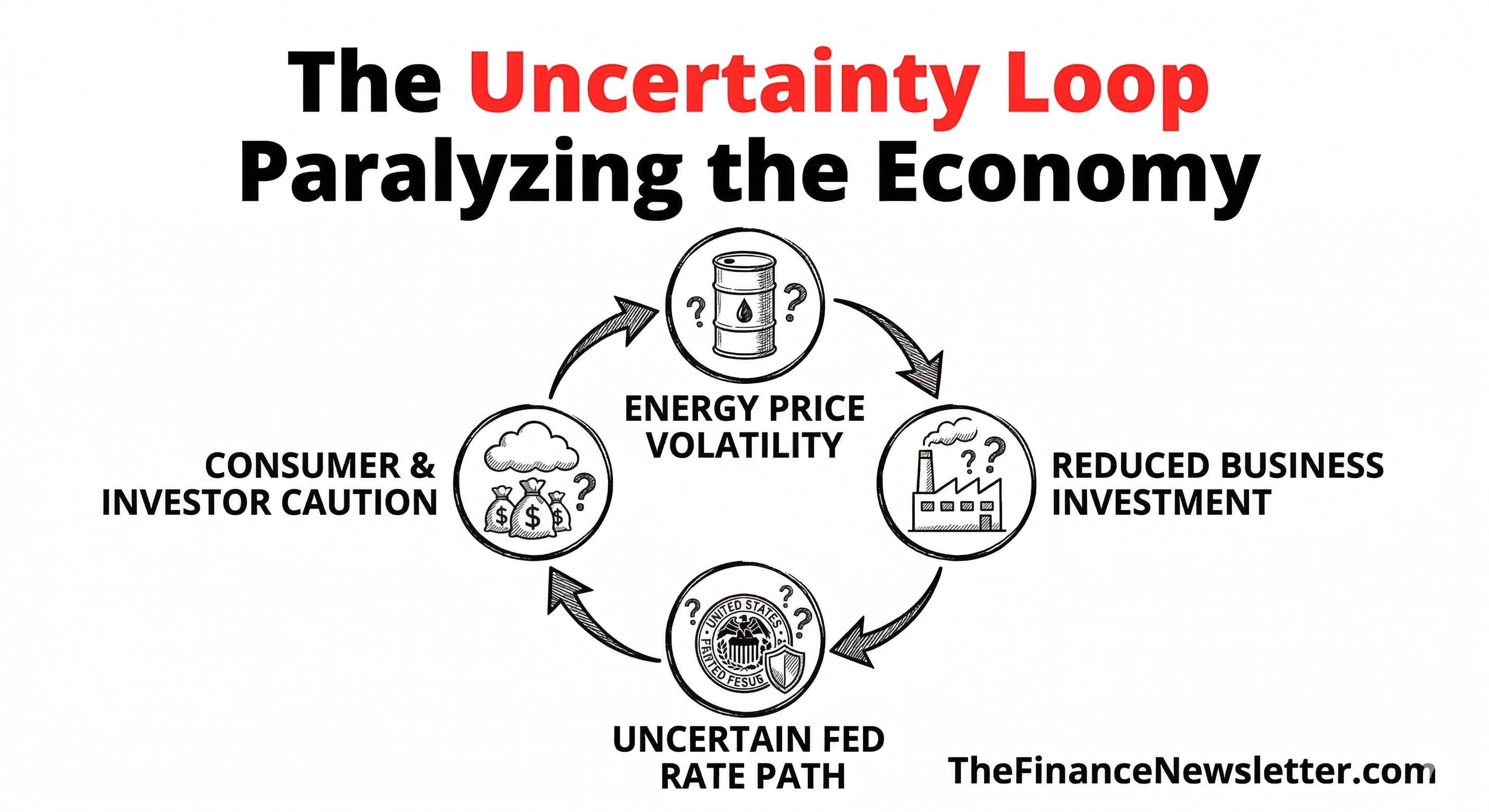

2. The Uncertainty Loop Paralyzing Our Economy

Here’s the core problem facing the US economy right now: nobody can make a decision because nobody knows how this ends. And when nobody decides, nobody invests, nobody hires, and nobody grows. That’s the loop.

The Wall Street Journal reported this week that Société Générale’s Michael Haigh warned that if the Hormuz disruption lasts another couple of weeks, global oil inventories could fall to historic lows. Morgan Stanley noted that “the whole ecosystem is more capital constrained than people think it is,” with energy and shipping constraints making AI data center construction harder and more expensive.

There are thin green shoots. Trump said Tuesday that Iran had reached out for a ceasefire. Iran’s president issued a rare open letter calling the war “costly and futile.” The UAE is reportedly weighing direct involvement to help reopen the Strait with UN backing. Goldman Sachs’ Jan Hatzius suggests that if the Strait reopens by mid-April, the US might see only a 0.4% economic contraction — slow growth, not a full recession.

But the fork in the road is razor-thin. Haigh warns Brent could hit $200 if disruptions spread further. Private credit is under strain. AI investment is showing early cracks. Higher energy costs are just starting to reach consumers. Deloitte’s downside scenario sees AI investment actually falling in 2027-28, unemployment hitting 6.5%, and GDP contracting in back-to-back years.

During my years in banking, we had a saying: uncertainty is the enemy of capital. Capital doesn’t disappear — it hides. It waits for clarity. When clarity arrives, it moves fast. The investors who prepare during uncertainty are the ones who win when resolution comes.

My advice: Think in scenarios, not predictions.

Scenario A (war ends soon): oil falls, stocks rally hard, tech leads the bounce — have your watchlist ready.

Scenario B (war drags on): oil climbs further, inflation accelerates, recession becomes reality — double down on energy, defensives, and cash.

Hedge both with some energy exposure and some defensive positioning. That’s the play right now.

3. The Only Two Catalysts Moving Stocks

Right now, the stock market is essentially controlled by two things: AI anxiety and Trump’s social media posts. Not earnings. Not GDP. Not Fed meetings. A Truth Social update or an Anthropic blog post can move the entire market in minutes.

One boutique hedge fund — Anaconda — told Bloomberg this week it has given up trying to trade around Trump’s announcements. CEO Renaud Saleur said Trump “changes opinion 10 times a day” and the implications are “not manageable.” Jeffrey Sonnenfeld wrote in Fortune that one prominent investor called it “impossible to trade in financial markets without getting into the mind of Trump” — more important than any macroeconomic indicator.

Last week, cybersecurity stocks dropped after a report that Anthropic’s new model poses “unprecedented cybersecurity risks.” Oil futures moved sharply on a Trump post Monday. This is not normal market behavior.

The TACO trade is losing its power. For the past year, every time the market feared escalation, Trump would back down — “Trump Always Chickens Out” — and investors learned to buy the dip on every Trump threat. But Thursday, when Trump extended the Iran ceasefire deadline by 10 days, markets didn’t rally. Oil surged to $110/barrel instead. Israel threatened escalation. Iran rejected talks. The market finally stopped believing the bluff.

My 20 years in finance taught me that the investors who trade on headlines consistently lose to the investors who trade on fundamentals. Headlines create short-term noise. Fundamentals determine long-term direction.

My three rules for navigating this market right now:

Write your investment thesis before the news arrives. Know why you own what you own. When a post contradicts your thesis, you’ll have a framework to evaluate it instead of panic-selling.

Size positions for volatility. If a 10% drop in a position keeps you up at night, you own too much of it.

Keep a shopping list ready. The best buying opportunities come when the news is scariest. The investors who bought during the 2020 COVID crash or the 2022 rate-hike selloff made fortunes. The next opportunity is being built right now.

4. Winners and Losers From the Iran War

Everyone knows the obvious moves — energy up, airlines down, defense up, tech down. The real edge in investing comes from finding the non-obvious winners and losers hiding behind the headlines.

The hidden loser nobody’s talking about: helium. Qatar supplies roughly a third of the world’s helium, and helium cools the machines that make AI chips. With the Strait of Hormuz closed and Qatari energy exports halted, helium prices have doubled in a month. South Korea — home to Samsung and SK Hynix, the world’s two largest memory chipmakers — is running critically low, with reserves potentially drying up by June. If that happens, chip production slows, AI hardware gets scarce, and semiconductor stocks face a supply-driven hit that has nothing to do with earnings or AI sentiment. This is a supply chain crisis hiding inside a geopolitical crisis.

The sneaky inflation driver: plastic. Plastic is made from petroleum. Oil is up 40%+. That means water bottles, packaging, medical supplies, garbage bags, car parts — all getting more expensive. Since plastic packaging touches nearly every consumer product, you’ll feel it at the grocery store before you understand why.

The surprise winners: off-price retailers. This is one of my favorite recession playbook trades, and it’s playing out in real time. Higher shipping costs and supply chain chaos are causing big retailers to receive inventory too late to sell it profitably — so they’re dumping it cheap. TJ Maxx, Ross Stores, and Burlington scoop that inventory at steep discounts and sell it to bargain-conscious consumers pulling back on spending. Burlington jumped 4.1% this week. Ross popped 3.75%. TJX climbed 2.5%.

The aluminum miners. Alcoa $AA and Century Aluminum $CENX surged after Iran struck the Middle East’s two largest aluminum smelters. The supply crunch was already severe from tariffs and the Strait closure. These attacks made it worse. Near-term, aluminum producers have a genuine tailwind. Long-term, watch China — the world’s largest aluminum producer — which could flood the market if prices rise too high.

The timeless lesson: In every economic downturn, consumers trade down. Restaurants to groceries. Groceries to store brands. Department stores to discount chains. That pattern is as reliable as gravity. TJX $TJX, Dollar General $DG, and Costco $COST historically outperform in downturns — and this one is no different. Know which direction the money flows before it happens, not after.

5. America’s Inflation Problem Just Got Worse

The OECD issued its starkest warning yet this week: the US is on track to have the highest inflation in the G7 in 2026, projected at 4.2%. That’s up from 2.6% last year and nearly double the Fed’s 2% target.

For context, the OECD’s projected 2026 inflation rates for other G7 members are: UK at 4%, Germany at 2.9%, Canada at 2.4%, Italy at 2.4%, Japan at 2.4%, and France at 1.8%. The US leads them all — by a meaningful margin.

Two compounding forces are driving this: the Iran war’s energy shock and Trump’s tariff policy. The effective US tariff rate sits at roughly 10.5% — the highest since World War II — meaning imported cars, electronics, and clothing are already more expensive before you factor in energy costs.

The downstream impact is everywhere. The USDA projects food prices to rise 3.6% this year, with groceries up 3.1%. Beef, fish, vegetables, and baked goods are all headed higher. Fertilizer — much of which ships through the Strait — is getting scarce, threatening crop costs further down the road. Gas is already up 35% in one month. And even if the war ends tomorrow, energy infrastructure damaged across the Middle East could keep prices elevated for months.

What 4.2% inflation actually means for your wallet: Your dollar buys 4.2% less every year. Wages need to rise 4%+ just to stay in place. Fixed incomes (bonds, pensions, savings accounts) quietly lose real value every single month. And the Fed is stuck — unable to cut rates to support a slowing economy without risking an inflation spiral.

My inflation survival playbook:

Commodities: Oil, metals, and agricultural commodities rise with inflation. Energy ETFs give you diversified exposure without picking individual stocks.

Real assets: Hard assets hold value during inflationary periods better than financial assets. Industrial and residential REITs are worth watching.

TIPS (Treasury Inflation-Protected Securities): Bonds that adjust with inflation, so your return keeps pace with rising prices.

Avoid long-duration bonds: Fixed coupon payments lose real value as inflation rises. Short-term Treasuries and money market funds offer far better protection right now.

6. The Fed Might Raise Rates for the First Time in Years

A month ago, the futures market priced in a 96% chance of one or more Fed rate cuts by September. This week, CNBC reported that flipped: traders now see a 52% chance of a rate hike by year-end — the first time that probability has crossed 50%.

Chicago Fed President Austan Goolsbee said this week: “I could see circumstances where we would need to raise rates.” That’s significant coming from a historically dovish official. Governor Christopher Waller — one of the strongest advocates for cuts just months ago — said the Iran war’s inflation risks swayed him to hold steady in March. San Francisco Fed President Mary Daly warned that even the March dot plot (showing one more cut expected this year) might be misleading, saying it “risks conveying a false sense of certainty.”

The core dilemma is brutal. The Fed has already cut rates by nearly 2 percentage points since September 2024, bringing the target range to 3.5%-3.75%. A growing number of officials now believe they’ve hit “neutral” — the rate that neither stimulates nor restricts the economy. Cutting further from neutral while inflation runs above 4% would be like pouring gas on a fire.

Three paths and none of them are clean. Raise rates: fight inflation but risk tipping a weakening economy into recession. Hold rates: hope inflation cools on its own while the labor market deteriorates. Cut rates: support growth but risk an inflation spiral back to 2022 levels. That’s stagflation’s defining cruelty — every option has a cost.

What this means for you:

Variable-rate debt is now a liability. Pay down credit cards, HELOCs, and adjustable mortgages before the Fed moves. Every month you wait could cost you more.

Short-duration Treasuries and money market funds are paying real yields. Lock in competitive returns without taking duration risk.

Banks benefit from higher rates. Net interest margins widen when rates rise — regional bank stocks tend to outperform in rate-hike cycles.

7. The Job Market Is the Worst It’s Been in 15 Years

The Labor Department reported this week that the hiring rate dropped to 3.1% in February — the lowest since April 2020. Excluding the pandemic’s worst months, it’s the weakest reading in more than 15 years. Job openings fell to 6.9 million. And employers announced 60,620 layoffs in March — up 25% from February — with most companies citing AI as the driver.

Fed Chair Jerome Powell told Harvard students this week: “There’s no denying that it’s a challenging time to enter the labor market.” That might be the understatement of the year.

Gallup found that just 19% of college graduates believe it’s a good time to land a quality job — down from over 70% in 2022. University of Michigan surveys show grads are more pessimistic today than at any point in the past four years. Over 40% of recent grads now view socialism positively — roughly double the rate from the 2010s. That’s not just politics. That’s the sound of an economic promise breaking.

Here’s the long-term reality most people aren’t ready to hear: white-collar hiring is set to stay weak through 2026, and AI is accelerating the erosion of entry-level roles. Data entry, basic research, customer service, administrative work — these were the stepping-stone jobs for new graduates. AI is eating them first, and eating them fast.

My advice:

If you’re employed: Build skills AI can’t easily replicate — leadership, creative strategy, complex judgment, relationship management. People who work with AI tools will outlast people who compete against them.

If you’re job-hunting: Niche down. A specialist in a specific domain always outlasts a generalist in a tough market.

If you’re investing: A weakening labor market is a leading indicator that consumer spending is next to drop. Rotate away from discretionary spending stocks (restaurants, retail, entertainment) toward consumer staples and essential services.

💡 Andrew’s Analysis & Advice:

All 7 stories point to the same core truth. The U.S. economy is entering a period where war risk, inflation risk, policy risk, and labor market weakness are feeding each other.

We are entering an era of stagflation. High prices and low growth. Energy shocks feed inflation. Inflation forces the Fed to hike rates. High rates kill job growth. This is a classic economic trap. Do not panic. Wealth is built during recessions. Build cash reserves. Avoid bad debt. Buy high quality assets when others sell in fear.

This is not just a bad-news cycle. It is a regime shift. A world that was priced for falling inflation, friendly Fed moves, and AI-fueled growth is being repriced for scarcity, conflict, caution, and tighter money.

👉 For daily insights, follow me on X/ Twitter; Instagram Threads; or BlueSky (and turn on notifications)

(3) Chart of the Day [Deep Dive]

The Greatest Valuation Reset In A Decade

💡 Andrew’s Analysis & Advice:

This week’s chart is one of the most important visuals you’ll see this year.

It tracks the Magnificent 7’s price-to-earnings (P/E) premium relative to the remaining 493 companies in the S&P 500. In plain English: how much more expensive the biggest tech stocks are compared to everything else in the market.

Here’s what the chart tells you at a glance.

At the peak in 2021, the Mag 7 traded at a roughly 100% P/E premium to the rest of the market. Investors were willing to pay double. The AI boom, pandemic-era hypergrowth, and near-zero interest rates created a combination that pushed valuations to near-record territory. The market was essentially saying: “These companies are so much better than everything else that they deserve to cost twice as much.”

Today, that premium has collapsed to just 30% — the lowest point on this chart’s 10-year history.

And that’s a number worth stopping on.

Why this happened is important context. The Mag 7 weren’t just caught in the Iran war crossfire. They were genuinely overvalued entering 2026. The war added two structural headwinds that are specifically tech-negative: rising energy costs (data centers are enormous energy consumers, and oil above $110/barrel makes running them significantly more expensive) and a broad risk-off rotation that pushed capital toward defensives. Microsoft had its worst quarter since 2008. Meta dropped 29%. Nvidia fell 20% from its October peak.

The valuation compression was inevitable. The war just accelerated the timeline.

Here’s what most investors are getting wrong about this chart. They’re either panicking out of tech (and selling at the worst time) or assuming 30% is the floor (and buying too early). The chart doesn’t tell you where the bottom is. What it does tell you is that the margin of safety in big tech has improved dramatically. A 30% premium is far more defensible than a 100% premium.

In 20+ years of investing, I’ve watched this pattern repeat: great companies fall out of favor, valuations compress, and eventually the fundamentals reassert themselves. The investors who bought Apple in 2013, Amazon in 2016, or Nvidia in 2019 bought when the crowd had given up on the story. That’s always when the best entries appear.

The long-term AI thesis remains intact. AI is still going to reshape every industry. The Mag 7 companies are still going to be at the center of it. The debate isn’t if — it’s when the market recaptures that.

My advice:

Think in time horizons.

6-month horizon: Be cautious. The short-term technical picture is still negative (more on that in Section 8). More pain is possible if oil climbs further or the war escalates.

3-5 year horizon: These valuations are starting to look genuinely compelling. The entry point you have today would have been unimaginable 18 months ago.

The strategy for this environment is dollar-cost averaging — investing a fixed amount at regular intervals rather than trying to call the exact bottom. You don’t need to catch the lowest price. You just need to be buying near it, consistently, while the crowd is still scared.

The bottom line: the Mag 7 are at their cheapest relative valuation in over a decade. That’s not a “buy everything today” signal. It’s a “start watching, start planning, and start building a position gradually” signal. When the tide turns, it turns fast. You want to already be in the water.

This newsletter takes many hours to research and write so please help me and:

Hit the LIKE button on this post and share this newsletter with friends & family:

Become a paid subscriber and get smarter with your money! (learn about the benefits here) (Get a free 30-day trial with this link):

(Your job can pay for this newsletter with its employee development budget — Send this email template to your manager)

Part II - Investing Research

4. Insider Trades

5. Top Stocks Right Now

6. Today’s Trade

7. Fear & Greed Analysis (Market Sentiment)

8. Macro Technical Analysis & Predictions

(4) Insider Trades (from Billionaires, Politicians, and CEOs):

When people with deep knowledge, such as politicians who set policy, executives who run the company, or legendary investors, put their own money on the line, pay attention.

1) Palo Alto Networks $PANW

CEO Nikesh Arora bought $9,999,977 of stock on 03/27/2026.

Palo Alto Networks $PANW provides AI-powered threat detection, cloud security, and network protection to enterprises worldwide. Arora knows the company’s pipeline, win rates, upcoming contract renewals, and competitive position better than any analyst on Wall Street. He’s not doing this for a tax benefit. He’s betting nearly $10 million of his own money because he believes the stock is undervalued right now.

The macro backdrop also supports this trade. The Iran war has dramatically increased cyber-threat activity across critical infrastructure globally. Anthropic’s new AI model generated fresh cybersecurity concerns just this week. As AI becomes more capable and more embedded in enterprise systems, the attack surface expands — and the demand for Palo Alto’s platforms grows with it.

Arora is also executing a “platformization” strategy — consolidating multiple security tools into one subscription model — which drives high switching costs and recurring revenue. Once a company is fully on the Palo Alto platform, leaving is enormously disruptive. That’s a durable competitive moat.

Long-term outlook for $PANW: The global cybersecurity market is projected to exceed $500 billion by decade-end. The AI agent economy creates entirely new categories of cyber risk and entirely new demand for enterprise security. CEO buying $10 million of his own stock during a market downturn is a conviction signal that’s historically among the most reliable in investing. Arora’s $10 million bet says the dip is a gift. Hard to argue with.

2) Iperionx Ltd $IPX

CEO Anastasios Arima bought $1,793,110 of stock on 03/30/2026.

Iperionx $IPX is a critical minerals company focused on domestic titanium production — a strategic metal that goes into military aircraft, missiles, submarines, medical devices, and advanced manufacturing. CEO Anastasios Arima bought $1,793,110 worth of shares on March 27, 2026, increasing his ownership by 4% to nearly 13 million shares.

The timing is extraordinary. Trump’s proposed budget calls for the largest US military buildup since World War II. Every fighter jet, missile system, and naval vessel depends heavily on titanium. The US has historically imported most of its titanium supply — a vulnerability that the Iran war has made glaring. Domestic production of critical metals is now a matter of national security, not just economics.

Arima buying $1.8 million of Iperionx shares while the Pentagon requests a $1.5 trillion budget is a calculated bet: defense spending will flow to companies that can supply critical domestic materials. That’s a powerful thesis with a long tailwind behind it.

Long-term outlook for $IPX: The domestic critical minerals story is one of the most compelling multi-decade investment themes of this era. Geopolitical fragmentation — accelerated by the Iran war — is forcing every major economy to onshore supply chains for materials that matter militarily. Companies that can produce titanium, lithium, and rare earth elements domestically have years of demand growth ahead. High risk given the company’s size, but the macro tailwind is powerful and the CEO’s conviction is evident.

3) Zenas Biopharma, Inc. $ZBIO

CEO Leon O Moulder Jr bought $1,021,140 of stock on 03/31/2026.

Zenas Biopharma $ZBIO is a clinical-stage biotech company focused on immunology and inflammation — conditions with massive unmet medical need and proven commercial potential. CEO Leon O. Moulder Jr. filed a purchase of $1,021,140 worth of shares on March 31, 2026, a 3% increase, bringing his total to over 2.1 million shares.

In clinical-stage biotech, a CEO buying over $1 million of his own stock is one of the strongest signals available. Moulder knows the pipeline, the upcoming data readouts, and the regulatory landscape better than any outside analyst. He’s not making a routine purchase. He’s making a conviction call with his personal capital.

The immunology and inflammation space has produced some of the most commercially successful drugs in pharma history. Humira generated over $200 billion in lifetime sales. Dupixent is still growing at $14+ billion annually. A successful drug in this category could be transformative for a company Zenas Biopharma’s size.

Long-term outlook for $ZBIO: Clinical-stage biotech is high-risk by nature — most drugs fail before reaching market. But when CEOs buy $1M+ at these price levels, it often precedes positive clinical data or regulatory milestones. Watch upcoming pipeline readouts closely. The immunology TAM is massive and the CEO’s money is on the table.

👉 For daily insights, follow me on X /Twitter; Instagram Threads; Facebook; or BlueSky (and turn on notifications)

(5) Top Stocks Right Now

1) Kodiak Sciences $KOD up +74.8% on Thu 3/26

Kodiak Sciences $KOD surged +74.8% last Thursday after revealing strong clinical trial data for its treatment of diabetic retinopathy — a leading cause of blindness in adults with diabetes. The results confirmed the company’s approach can produce meaningful improvements in patient outcomes, a major milestone for a biotech working in one of the most underserved areas of ophthalmology.

Diabetic retinopathy affects tens of millions of people worldwide. Current treatments require frequent, painful injections directly into the eye — a compliance challenge that leaves many patients undertreated. Kodiak’s pipeline is targeting extended dosing intervals without sacrificing effectiveness. Strong trial data in this space can move a small biotech dramatically, and that’s exactly what happened here.

Long-term outlook for $KOD: The global diabetic eye disease treatment market is projected to exceed $15 billion by the early 2030s. An aging global population and rising diabetes rates ensure a growing patient base. If Kodiak’s results hold through later-stage trials and reach regulatory approval, the upside from today’s price could still be significant. High risk given the clinical stage, but the data is a genuine catalyst worth monitoring.

2) Navan $NVAN up +43.3% on Thu 3/26

Navan $NVAN, the AI-powered business travel and expense management platform (formerly TripActions), jumped +43.3% last Thursday after reporting strong earnings and upbeat 2027 revenue guidance. The company beat Q4 expectations and gave investors a confident forward outlook — a rare bright spot in an otherwise difficult environment for technology stocks.

Navan helps companies manage employee travel and spending through an intelligent platform that automates booking, expense reporting, and policy compliance. With businesses looking to cut costs without eliminating travel entirely, an AI-driven platform that finds savings automatically while reducing admin work is exactly what CFOs want right now.

Long-term outlook for $NVAN: Corporate travel and expense management is a large and growing market, estimated at $50+ billion globally. As companies increasingly demand proof of ROI on every dollar spent, tools that provide real-time visibility into travel and expense data become non-negotiable. Navan’s strong guidance signals confidence in winning more enterprise contracts. Worth watching as a long-term AI-plus-SaaS growth story.

3) Argan $AGX up +37.9% on Fri 3/27

Construction company Argan $AGX surged +37.9% last Friday on a fourth-quarter earnings and revenue beat, with guidance topping expectations by a wide margin. Argan builds power generation facilities — natural gas plants, renewable energy projects, and industrial infrastructure.

In a world where AI data centers are consuming unprecedented amounts of electricity, and where the Iran war has made domestic energy infrastructure a national priority, a company that builds power generation capacity is exactly what the market is rewarding. Argan’s backlog of projects reflects real demand, not speculation.

Long-term outlook for $AGX: The energy infrastructure buildout is one of the decade’s biggest investment themes. AI data centers require massive, reliable power — and the US grid simply isn’t built for the demand that’s coming. Companies that build power generation facilities quickly and at scale have years of contracted backlog ahead. Argan’s guidance beat signals the pipeline is healthy and growing. Power generation construction is set to be one of the most in-demand services in the US economy for the next 5-10 years.

4) Penguin Solutions $PENG up +13.4% on Thu 4/2

AI infrastructure company Penguin Solutions $PENG rose +13.4% yesterday after beating Q1 expectations and raising its full-year outlook — impressive performance in a market where tech is broadly under pressure. Penguin Solutions provides high-performance computing infrastructure, including the complex systems that power AI training and inference workloads.

The company’s raised guidance is the key signal. It means demand for AI compute isn’t slowing — it’s accelerating. Even as investors question the ROI of AI spending broadly, the companies building the infrastructure layer continue to win contracts and grow revenue.

Long-term outlook for $PENG: AI infrastructure is one of the most durable multi-year investment themes in tech. Every large language model trained, every AI agent deployed, every enterprise adopting AI tools runs on infrastructure like what Penguin Solutions provides. As AI moves from experimental to embedded, the infrastructure layer becomes critical and recurring. The company’s raised guidance says the demand environment is real, not speculative.

5) United Therapeutics $UTHR up +12.5% on Mon 3/30

United Therapeutics $UTHR rose +12.5% last Monday after a nebulized (inhaled) version of its blockbuster drug Tyvaso delivered improved results in a second Phase 3 clinical trial. Tyvaso treats pulmonary arterial hypertension (PAH) — a serious and often fatal condition affecting blood flow through the lungs.

United Therapeutics has built one of the most durable franchises in rare disease. Tyvaso is already a multi-billion dollar drug. A new delivery format (nebulized vs. inhaled powder) that shows better clinical outcomes expands the addressable market and extends the drug’s commercial life — both powerful long-term value drivers.

Long-term outlook for $UTHR: Rare disease is one of the most attractive niches in biotech — pricing power is high, competition is limited, and patients are loyal to treatments that genuinely work. United Therapeutics also carries a long-term moonshot: xenotransplantation (genetically engineered pig organs for human transplant), which could eventually open an entirely new multi-billion dollar market if regulatory and clinical hurdles are cleared. The Tyvaso trial data this week is near-term validation of a company executing well across multiple fronts.

6) Symbotic $SYM up +12.2% on Tue 3/31

Symbotic $SYM surged +12.2% last Tuesday on a new warehouse automation partnership with Associated Wholesale Grocers — one of the largest wholesale grocery cooperatives in the US, supplying thousands of independent grocery stores across the country.

Symbotic builds AI-powered robotic systems for warehouse automation. Its systems move and sort inventory at speeds no human workforce can match, at a fraction of long-term operating cost. As inflation raises labor expenses and supply chain disruptions create a premium on operational efficiency, warehouse automation moves from competitive advantage to business necessity.

Long-term outlook for $SYM: Warehouse automation is a massive, secular growth market projected to exceed $80 billion globally by 2030. The grocery sector — high volume, razor-thin margins, constant pressure to reduce costs — is exactly where automation ROI is most compelling. Symbotic’s Associated Wholesale Grocers partnership deepens its footprint in a category where adoption can cascade quickly once competitors see the efficiency gains. The long-term pipeline for $SYM is one of the most compelling in the robotics space.

7) CoreWeave $CRWV up +12.0% on Tue 3/31

CoreWeave $CRWV climbed +12.0% last Tuesday after securing an $8.5 billion investment-grade term loan backed by its compute hardware — an industry first. CoreWeave provides GPU cloud computing infrastructure specifically designed for AI training and large-scale model inference.

Getting an $8.5 billion investment-grade term loan backed by hardware as collateral is a landmark moment for the AI infrastructure sector. It signals that capital markets are now comfortable treating AI compute infrastructure as a real, financeable asset class — not just a speculative technology bet. For CoreWeave, it means access to growth capital at better terms than most AI-adjacent companies can achieve.

Long-term outlook for $CRWV: CoreWeave is positioned as a GPU-focused alternative to Amazon, Google, and Microsoft cloud for AI compute workloads. Its specialization gives it a performance and cost advantage for AI training specifically. As AI demand grows and hyperscalers struggle to keep pace, specialized GPU clouds fill the gap. The $8.5 billion loan extends its competitive runway significantly. Long-term, the question is whether it can scale fast enough to defend against trillion-dollar cloud providers. Near-term, the demand environment is strongly in its favor.

💡 Andrew’s Advice:

AI infrastructure keeps winning regardless of market sentiment. CoreWeave and Penguin Solutions both rose on earnings beats and raised guidance — proving that demand for AI compute is real and growing even as the broader tech sector struggles. These are the "picks and shovels" plays: while investors debate which AI company ultimately wins, the companies building the infrastructure they all need are compounding their businesses.

Efficiency and automation are the playbook for a high-cost, inflationary environment. Symbotic's warehouse automation win is a direct response to rising labor costs. Companies that help other companies do more with less are structurally advantaged when margins are under pressure everywhere.

The war creates second-order winners that most investors miss. Argan's construction surge — driven by energy infrastructure demand — both trace back to the same macro backdrop. In every major geopolitical shift, the best trades are often two steps removed from the headline. Train yourself to look there first.

Healthcare and biotech are becoming the new safe haven. Kodiak Sciences, United Therapeutics, and ongoing acquisition activity across the sector all reflect a rotation toward recession-resistant, non-correlated growth. When the macro gets ugly, healthcare keeps delivering — because people don't stop needing treatment because the stock market is down.

👉 For daily insights, follow me on X /Twitter; Instagram Threads; Facebook; or BlueSky, and turn on notifications!

(6) Today’s Trade

The options market is where the smartest traders place their biggest bets. I monitor options flow activity daily.

Virgin Galactic Holdings $SPCE

Virgin Galactic Holdings $SPCE is a commercial space company working toward bringing paying passengers to the edge of space on suborbital flights. After years of development delays, funding challenges, and intense competition from Blue Origin, the company is trading just above its 52-week low of $2.13.

This week, something interesting caught my attention in the options market. Call volume in $SPCE hit 33,654 contracts — 7x the average daily volume and, more strikingly, 40x put volume. Traders are focused on two expiration months: May 15, 2026 (targeting the 3.50 strike call) and July 17, 2026 (targeting the 2.50 strike call, with most July activity appearing to be buys, while some traders close short call positions at the 2.50 strike based on open interest analysis). Both Jefferies and Susquehanna downgraded the stock on consecutive days this week — making the scale of bullish call activity even more unusual.

Call-to-put ratio: 40 to 1. This is an extreme skew toward upside bets. At this ratio, someone sees a catalyst that the stock’s beaten-down price doesn’t reflect. Whether that’s a partnership announcement, a funding development, or simply speculative positioning ahead of news — the options market is sending a signal worth noting.

My take: I’m cautiously bullish on this options play — not because $SPCE’s fundamentals are strong (they’re not), but because 52-week low prices plus a 40-to-1 call-to-put ratio plus unusually high volume equals a setup where a small positive catalyst could create outsized short-term upside. This is a speculative, high-risk, short-duration trade. Size it as a small, defined-risk position. Don’t let the call volume size convince you to overcommit.

Long-term outlook for $SPCE: Commercial space tourism is a real market, but Virgin Galactic faces intense competition from Blue Origin and operates in an environment where SpaceX — about to launch the world’s largest IPO at a $1.75 trillion valuation — is the dominant force. Long-term, $SPCE needs a meaningful improvement in its financial position and a clear path to recurring revenue before it becomes a compelling long-term investment.

👉 For daily insights, follow me on X /Twitter; Instagram Threads; Facebook; or BlueSky (and turn on notifications)

(7) Fear & Greed Analysis (Market Sentiment)

How do you cut through the noise and understand what’s really happening? The secret is to look at the feelings people, the actions of investors, and the facts about the economy.

Current Reading: 19 — Extreme Fear.

This is a negative/bearish short-term signal, but also a historically important contrarian indicator for long-term investors.

A reading of 19 means almost every major sentiment indicator is flashing red at the same time. The S&P 500 is trading below its 125-day moving average (negative momentum). The NYSE is generating far more 52-week lows than highs (negative price strength). Market breadth is weak — far more volume flowing into falling stocks than rising ones (extreme fear). The put/call ratio is elevated — investors are buying protection at a high rate (extreme fear). Safe haven demand is high — money is flowing into bonds over stocks (fear). Junk bond spreads are widening — investors are fleeing risk (extreme fear).

The macro backdrop explains every single indicator. The Iran war, oil above $110/barrel, inflation heading to 4.2%, rising recession odds, and a weakening labor market have all hit the market simultaneously. That’s an unusually high concentration of fear catalysts in a short period.

But here’s the insight that separates smart investors from the crowd: Extreme Fear is historically one of the best times to start building positions. Warren Buffett famously said: “Be fearful when others are greedy, and greedy when others are fearful.” The principle is right, but the timing matters.

In my 20+ years in banking and investing, I watched this pattern repeat: the moments of maximum fear — September 2022, March 2020, December 2018, February 2016 — were the best entry points of each cycle. Not because the bad news suddenly disappeared. Because the bad news was already priced in. Nearly everyone who was going to sell had already sold. That’s called exhausted selling. And exhausted selling tends to precede recoveries.

A reading of 19 is not a “buy everything today” signal. It’s a “start planning and building your shopping list” signal. The war could escalate. Oil could push to $150. Or a ceasefire could come this weekend. You don’t know. But what history tells you clearly is that markets at Extreme Fear levels are statistically closer to bottoms than tops.

One year ago, the index was at 12 — even deeper fear than today. Investors who bought there significantly outperformed. The same opportunity may be building now.

My advice:

Fear & Greed below 15: Consider that a “maximum fear” zone where deploying cash methodically is historically rewarded.

Fear & Greed recovering toward 25: An early signal that the worst selling pressure has passed.

Fear & Greed recovering toward 50 (Neutral): Recovery is underway. You should already be invested, not trying to buy the exact bottom.

Current events and macro align perfectly with this reading. The Iran war, rate hike fears, and layoff news are all contributors. When — not if — those fears begin to ease, this index will recover. And it tends to move faster than most investors expect. The time to prepare is now, not when the news gets better.

👉 For daily insights, follow me on X /Twitter; Instagram Threads; Facebook; or BlueSky (and turn on notifications)

(8) Macro Technical Analysis

Technical levels matter because they’re where millions of traders have programmed their buy and sell orders. When key levels break, algorithms kick in and magnify moves.

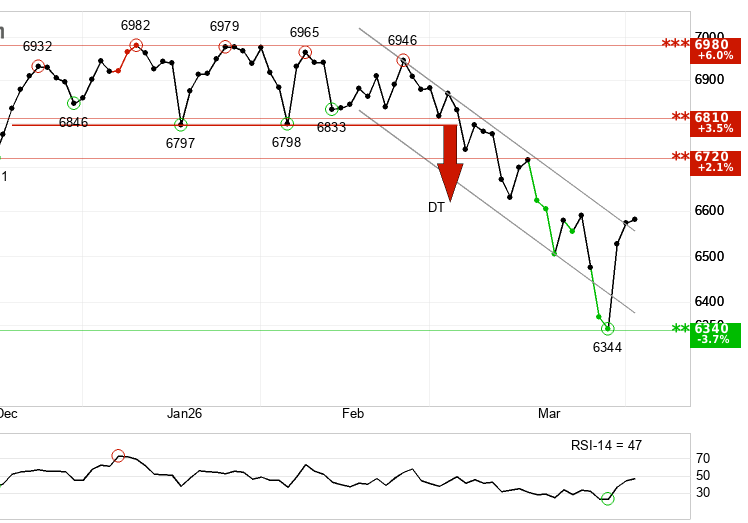

1) S&P 500 SPY 0.00%↑

Short-term trend: Negative.

The S&P 500 is showing a negative technical picture in the near term, though there are early signs that the pace of decline is beginning to slow.

The index has broken upward through the ceiling of its short-term falling trend channel — which counterintuitively means the rate of decline is slowing, not that the index is surging. However, the recent double top formation at around 6,797 broke cleanly through support, and the downside target of 6,620 has now been met. The formation signals further potential downside before any meaningful recovery.

Support sits at approximately 6,340. Resistance sits at approximately 6,720. The index is currently caught between these two levels, neither breaking out convincingly nor collapsing further. Medium-term is Positive. Long-term is Positive.

In plain English: the worst of the selling pressure may be starting to exhaust itself in the short term, but the chart hasn’t turned bullish yet.

2) Tech Stocks QQQ 0.00%↑

Short-term trend: Negative.

The Nasdaq-100 is in the clearest and most bearish technical position of the three assets analyzed this week. The index is in a confirmed falling trend channel — meaning investors have been selling at progressively lower prices over time, a textbook negative signal.

The Nasdaq broke down from a head and shoulders formation at around 24,736 — one of the most reliable bearish formations in technical analysis — triggering a sell signal. The downside target of 24,126 has been met, but the formation signals further downside potential. Support sits at 23,000. Resistance sits at 24,700.

Medium-term is Hold. Long-term is Positive.

Don’t try to catch this falling knife yet. The head and shoulders breakdown in the Nasdaq is a serious signal. Respect it. The medium-term “hold” rating suggests the worst of the decline may pass before getting dramatically worse — but near-term, the path of least resistance is still lower.

3) Bitcoin $BTC

Short-term trend: Neutral.

Bitcoin is at a critical technical decision point. It has broken through the floor of its short-term rising trend channel and marginally breached support at 67,300. An established break below that level would signal further downside. However, volume was high at prior price tops and low at prior price bottoms — a pattern that slightly weakens the bearish signal and suggests the breakdown may not be confirmed.

The overall near-term assessment: neutral/hold.

The key number to watch is $67,300. If Bitcoin holds above that level, it may stabilize near current prices. A clean break below $67,000 opens the technical door toward $64,000 and potentially lower. Given the macro backdrop — risk-off sentiment, Extreme Fear reading of 19, and stock market weakness — Bitcoin faces correlation risk with equities in the near term.

4) Macro Analysis (what this means for you)

The near-term picture is negative across the board. The mid-term picture is improving.

All three assets this week tell a consistent story. The Nasdaq is in the worst shape — confirmed falling trend, head and shoulders breakdown, no near-term reversal signal. The S&P 500 is marginally better — still negative, with some early deceleration of selling pressure. Bitcoin is in neutral territory — not confirming a recovery, but not collapsing further either.

These technical readings align directly with the Fear & Greed Index sitting at 19 (Extreme Fear). Markets that have been sold aggressively for five consecutive weeks tend to show exactly these patterns: falling trend channels, oversold momentum indicators, and broken support levels. The question is always the same: is this the exhaustion phase, or is there another leg lower?

The macro overlay is the missing variable no chart can capture. The Iran war and its impact on oil prices, inflation expectations, and risk appetite is the single driver behind all of these technical moves. No head and shoulders pattern can tell you when the Strait of Hormuz reopens. But charts do tell you where prices are relative to key levels — and right now, we’re in oversold, extreme-fear territory where the risk/reward for patient, long-term investors is starting to improve.

The interconnected signal: The Fear & Greed Index at 19 plus the Nasdaq’s head and shoulders breakdown plus the S&P’s decelerating trend channel plus Bitcoin holding (so far) at 67,300 all point to the same conclusion. We’re likely closer to a short-term floor than a continued freefall — but confirmation hasn’t arrived yet.

My plan: Stay patient, stay informed, stay positioned defensively in the near term — and keep your shopping list updated. When the technicals turn and the sentiment shifts, the move will be fast. You want to be ready before it happens, not scrambling after it starts.

This newsletter takes a week to research & write so please help me and:

Hit the LIKE button on this post & share this newsletter with friends and family:

Become a paid subscriber and get smarter with money! (learn about the benefits here) (Get a free 30-day trial with this link):

Part III - My Tips & Advice

9. Advice & Recommendations

10. Final Thoughts & Lessons

11. Your Questions Answered

(9) My Advice & Recommendations:

Uncertainty is the real enemy. When no one knows how the war ends, capital hides. When you can't predict the outcome, focus on positioning. Build cash reserves. Avoid bad debt. Own assets that thrive in multiple scenarios.

Energy is the only S&P 500 sector in positive territory in 2026 — up 39% this quarter. Oil stocks, LNG players, and natural gas companies are the direct beneficiaries of the Iran war's supply shock. If you have zero energy exposure right now, that's a gap to close.

Own the second-order winners, not just oil. The crowd buys energy stocks. Smart money buys helium and aluminum. Helium prices have doubled. Aluminum hit a 4-year high after Iran’s attacks. Buy ETFs like $HEL (helium) or stocks like $AA (Alcoa) and $CENX (Century Aluminum). These are the hidden supply chain bottlenecks that will keep inflating for months.